Introduction

In 2025, bitcoin continued to integrate into the global financial system. The launch and growth of spot bitcoin ETFs in 2024 and 2025, the inclusion of digital asset public companies in major equity indices, and ongoing regulatory clarity are shifting bitcoin from the “crypto” fringe toward a new asset class that we believe is worthy of institutional asset allocation.

In our view, the unifying theme for the current cycle is bitcoin’s transition from an “optional” new monetary technology to a strategic allocation for a growing set of investors. In our view, four trends are increasing bitcoin’s value proposition:

- The macro and policy backdrop shaping demand for scarce digital assets.

- Structural ownership trends across ETFs, corporates, and sovereigns.

- Bitcoin’s relationship to gold and the broader store-of-value continuum.

- Evidence that bitcoin’s drawdowns and volatility are diminishing when compared to prior cycles.

In this article, we outline these trends.

The 2026 Macro Backdrop

Monetary Conditions And Liquidity

After an extended period of monetary policy tightening, the macro landscape is shifting: quantitative tightening (QT) ended in the US last December, the U.S. Federal Reserve’s (Fed’s) rate-cutting cycle still is in early innings, and more than $10 trillion in lower-yielding money-market and fixed-income ETFs could be poised to rotate into risk assets.1

Policy And Regulatory Normalization

Regulatory clarity remains a constraint—and potential catalyst—for institutional adoption. In the US and abroad, policymakers have been advancing frameworks to clarify digital asset oversight, to standardize custody, trading, and disclosure, and to provide more guidance for institutional allocators.

Proposals like the U.S. CLARITY Act (Digital Asset Market Clarity Act)—under which the Commodity Futures Trading Commission (CFTC) would regulate digital commodities and the Securities and Exchange Commission (SEC), digital securities—could reduce compliance uncertainty for companies focused on and institutions evaluating allocations to digital assets. The US CLARITY Act provides a compliance roadmap for the lifecycle of a digital asset, with a standardized “maturity test” allowing tokens to transition from SEC to CFTC oversight as they decentralize. With a dual-registration regime for broker-dealers, the Act reduces the legal “limbo” that historically has driven digital asset firms offshore.

The US government also has addressed bitcoin-specific issues in the following ways:

- Discussions between lawmakers and industry leaders about adding bitcoin to government reserves.

- Treatment and management of seized bitcoin holdings, now mostly under federal control.

- Bitcoin adoption at the state level, with Texas leading the way, buying and adding bitcoin to its reserves.

Structural Demand: ETFs And DATs

ETFs As A New Structural Buyer

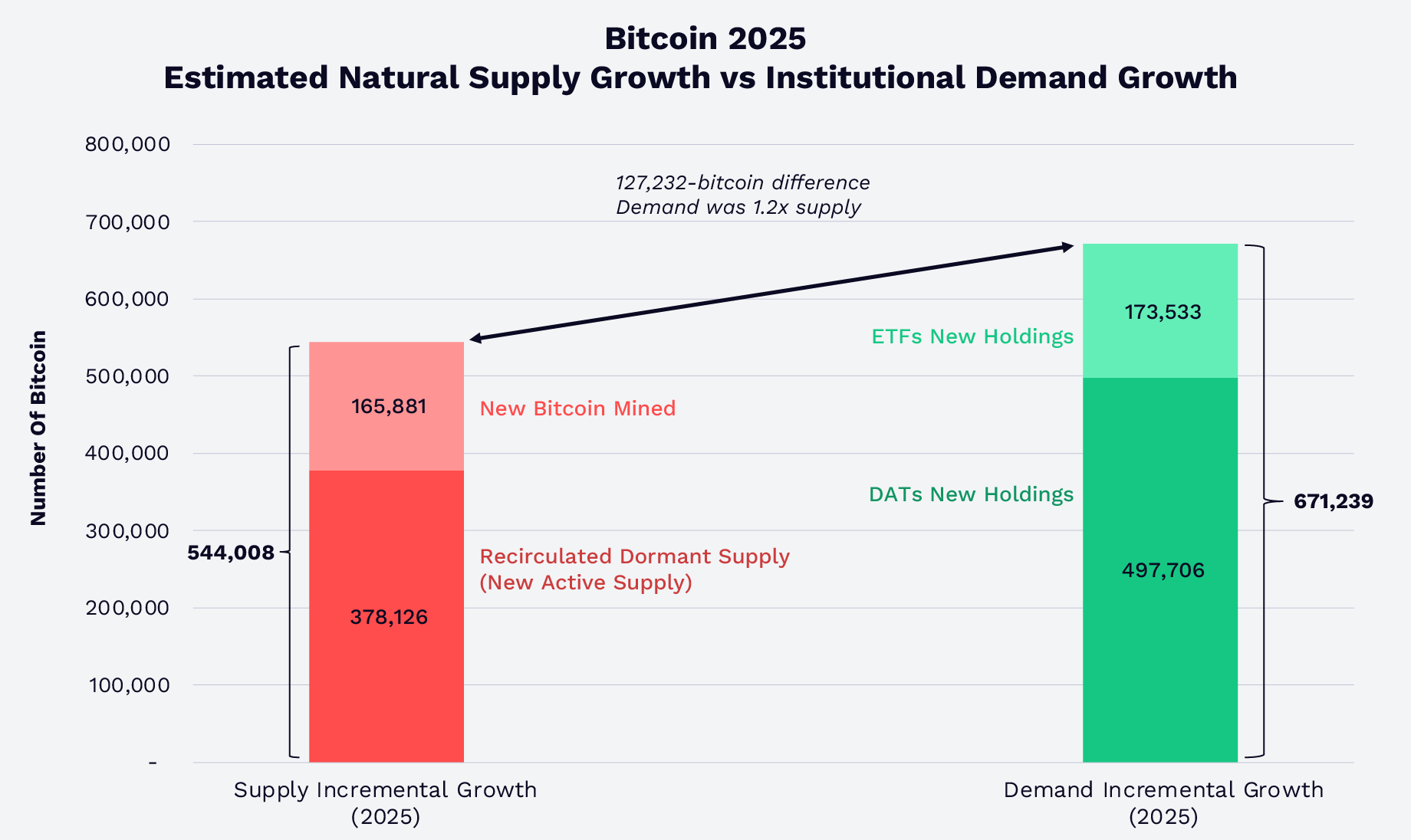

The scaling of spot bitcoin ETFs has reshaped the market’s supply-demand profile. In 2025, US spot bitcoin ETFs and digital asset treasuries (DATs) absorbed 1.2 times the combination of newly mined bitcoin supply and the number of dormant bitcoins recirculated (active supply growth), as shown below. By year-end 2025, ETFs and DATs held more than 12% of the total bitcoin outstanding. Although the growth in its demand surpassed the growth in its supply, bitcoin’s price declined, seemingly in response to exogenous factors—the large liquidation event caused by a software glitch on October 10, fears of the bitcoin four-year cycle turning, and negative sentiment around quantum computing threatening bitcoin’s cryptography.

Source: ARK Investment Management LLC and 21Shares, 2026, based on data from Glassnode as of December 31, 2025. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency.

During the fourth quarter, Morgan Stanley and Vanguard added bitcoin to their investment platforms.2 Morgan Stanley expanded client access to regulated bitcoin products, including spot ETFs. Surprisingly, after years of excluding crypto and all commodities from its ecosystem, Vanguard added third-party bitcoin ETFs to its platform. As ETFs mature, they should function increasingly as a structural bridge between the bitcoin market and traditional capital pools.

Bitcoin-Exposed Companies In Indexes, Corporate Adoption, And Bitcoin Treasuries

Corporate adoption of bitcoin has broadened beyond a handful of early adopters. The S&P 500 and Nasdaq 100 Indexes have included the stocks of companies like Coinbase and Block, incorporating bitcoin-adjacent exposure into mainstream portfolios. Formerly MicroStrategy, Strategy, a digital asset treasury (DAT), has built a sizable bitcoin treasury position amounting to 3.5% of total supply.3 Moreover, Bitcoin DAT companies now hold more than 1.1 million BTC, representing 5.7% of supply valued at ~$89.9 billion as of end of January 2026.4 For the most part, these treasuries include a cohort of long-term as opposed to short-term holders.

Sovereigns And Strategic Holdings

In 2025, on the heels of nation-state of El Salvador, the Trump Administration established the U.S. Strategic Bitcoin Reserve (SBR)—with seized bitcoin. Today, the SBR holds ~325,437 BTC, 1.6% of total bitcoin supply, valued at $25.6 billion.5

Bitcoin And Gold As Stores-Of-Value

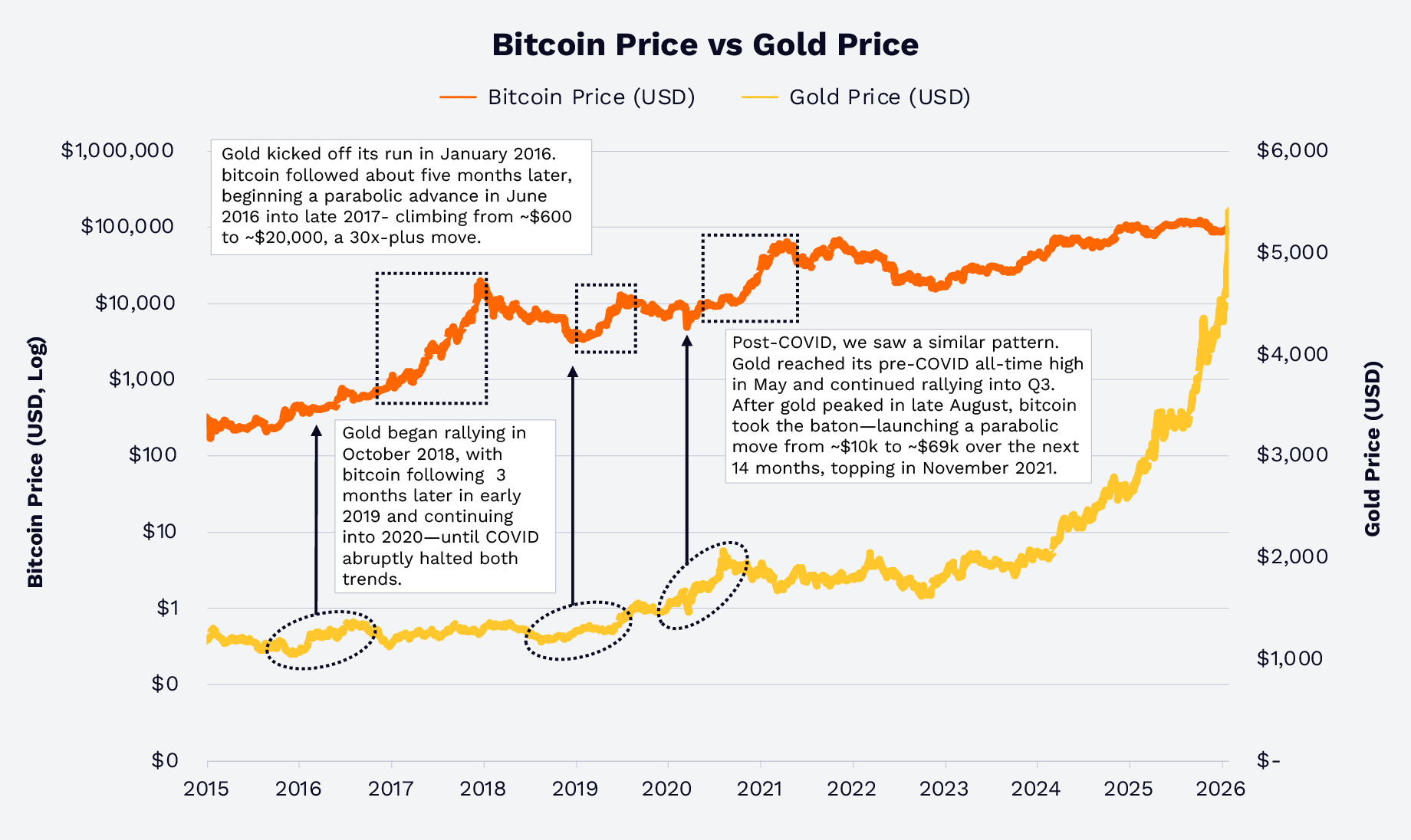

Gold Leads, Bitcoin Follows?

In recent years, gold and bitcoin have responded differently to macro narratives around currency debasement, negative real yields, and geopolitical risk. In 2025, the gold price surged 64.7% on concerns about inflation, fiat debasement, and geopolitical risk. Somewhat surprising, the price of bitcoin dropped 6.2%, a divergence, however, with historical precedence.

In 2016 and 2019, an advance in the gold price led that in the bitcoin price. In early 2020, during the COVID shock, a rally in the gold price foreshadowed an increase in the bitcoin price after an explosion in fiscal and monetary liquidity. This gold-bitcoin pattern became pronounced in 2017 and 2018, as shown below. Does history rhyme? Based on historical relationships, bitcoin is a high-beta,6 digitally native extension of the same macro trade that historically has supported gold.

Source: ARK Investment Management LLC and 21Shares, 2026, based on data from Glassnode and TradingView as of January 31, 2026. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency. Past performance is not indicative of future results.

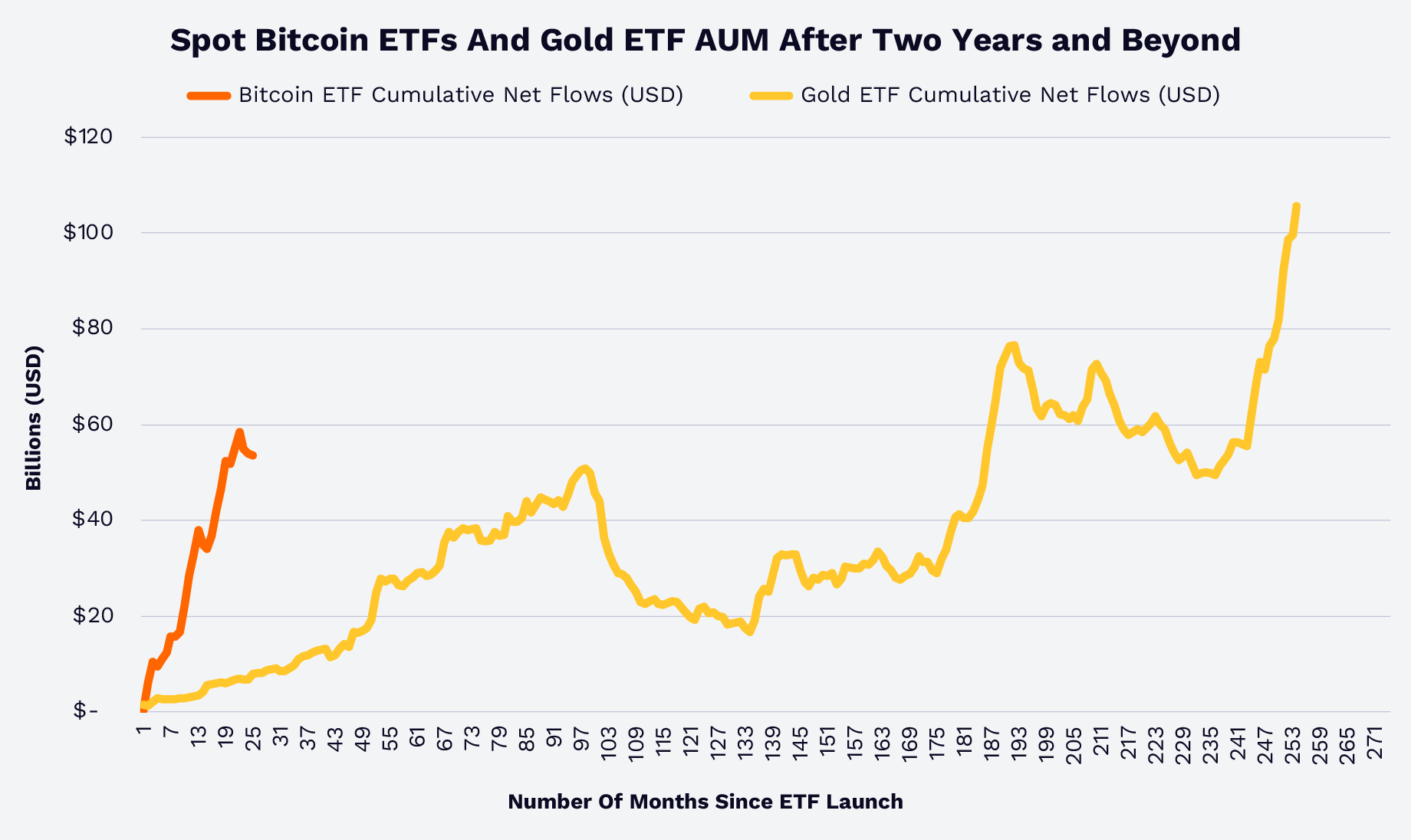

ETF AUM: Bitcoin Gaining Share

Cumulative ETF net flows offer another comparison of bitcoin to gold. According to Glassnode and World Gold Council data, spot bitcoin ETFs accomplished in less than two years what took gold ETFs more than 15 years, as shown in the chart below. In other words, financial advisors, institutions, and retail investors seem to be more comfortable with bitcoin’s role as a store-of-value, a diversifier, and a new asset class.7

Source: ARK Investment Management LLC and 21Shares, 2025, based on data from Glassnode and World Gold Council as of December 31, 2025. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency. Past performance is not indicative of future results.

Interestingly, the correlation between bitcoin and gold returns over the last market cycle since 2020 has been very low, as shown below. That said, gold could be a leading indicator.

Note: The correlation matrix above uses weekly returns from 1/1/2020 through 1/6/2026. The assets are as follows: Bitcoin = Bitcoin Currency, Gold = Gold Currency, Commodities = Bloomberg Commodity Index, S&P 500 = S&P 500 Index, Bonds = Bloomberg US Aggregate Bond Index, REITS = FTSE Nareit Equity REITS Index. Source: ARK Investment Management LLC, 2026, based on data from Bloomberg as of January 12, 2026. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency. Past performance is not indicative of future results.

Market Structure And Investor Behavior

Drawdowns, Volatility, And A Maturing Market

Bitcoin is a volatile asset, but its drawdowns have diminished over time. In prior cycles, peak-to-trough declines regularly exceeded 70–80%. In the current cycle since 2022, as of February 8, 2026, no downswing from record all-time highs has exceeded ~50%, as shown below, suggesting incremental participation and deeper liquidity—even in the face of major corrections, such as the one that occurred during the first week of February 2026.

Source: ARK Investment Management LLC and 21Shares, 2025, based on data from Glassnode as of January 31, 2026. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency. Past performance is not indicative of future results.

These observations suggest that bitcoin is transitioning from a speculative asset to a globally traded macro instrument with increasingly diverse holders, supported by a robust trading, liquidity, and custodial infrastructure.

Time In The Market vs Timing The Market

Based on data from Glassnode, from 2020 to 2025, a hypothetical “worst” bitcoin investor—one who invested $1,000 at the highest price every year—turned ~$6,000 into ~$9,660 by December 31, 2025, and ~$8,680 by January 31, 2026—a ~61% and ~45% return, respectively, as shown below. Even with the recent correction in the first week of February, this investment would be $7,760 by February 8—a ~29% return.

Source: ARK Investment Management LLC and 21Shares, 2026, based on data from Glassnode as of January 31, 2026.[KG1] The data presented are a hypothetical illustration and do not represent the investments or returns of an actual investor. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency. Past performance is not indicative of future results.

The lesson here is that, since 2020, holding periods and position sizing have been more important than timing: they generally have rewarded investors focused on bitcoin’s value proposition—not its volatility.

Bitcoin’s Strategic Question Today

In 2026, bitcoin’s story is less about whether it will “survive” and more about its role in diversified portfolios. Bitcoin is:

- A scarce, non-sovereign asset in a controversial environment of evolving global monetary policies, government deficits, and trade deficits.

- A high-beta extension of traditional store-of-value assets like gold.

- A global liquid macro instrument available in regulated vehicles.

Long-term holders—including ETFs, corporate treasuries, and sovereign entities—have absorbed a significant share of new bitcoin supply, as regulatory and infrastructure progress has broadened access. Historical data also suggest that, thanks to the low correlation of bitcoin returns to those of other assets, including gold, allocations to bitcoin potentially could have improved the risk-adjusted returns of portfolios, even more so now that its volatility and drawdowns have decreased over a full market cycle. As investors evaluate this new asset class in 2026, the question we believe they face is not “whether” but “how much” to allocate to bitcoin, “through which vehicle.”

Disclaimer:

- This article is reprinted from [ARK-INVESTt]. All copyrights belong to the original author [David Puell, Matthew Mena]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.