Summary

-

Driven by macro factors, both the allocation and trading demand for gold have risen simultaneously. In January 2026, global physical gold ETFs recorded a historic monthly net inflow of $19 billion, pushing the global gold ETF AUM to $669 billion.

-

Tokenized gold is dominated by the two leading solutions, Tether - XAUT and Paxos - PAXG, which together account for as much as 97% of the total market capitalization. Their combined perpetual open interest exceeds $1 billion, and their cumulative on-chain trading volumes have both surpassed $4 billion.

-

Competition in gold trading among platforms is essentially a competition for index governance power. Whether XAUT/PAXG are included, how weights switch during market closures, and the composition and risk control constraints of external data sources/oracle feeds determine the product’s price quality during market closures and extreme volatility.

-

Gate has built a full-stack gold market covering tokenized gold spots, leveraged ETFs, TradFi CFDs, metal perpetuals, and on-chain Perp DEX to meet different user needs.

I. Macroeconomic Background

Gold is being repriced amid macroeconomic uncertainty, while both traditional ETF investment channels and on-chain tokenized gold channels are expanding simultaneously. Market focus is shifting from whether to allocate to gold toward what form of gold to allocate and how to hold and trade gold more efficiently across different financial systems. In this context, digital gold is increasingly referring to the on-chain tokenization of physical gold and its freely tradable nature.

1.1 Gold at Historical Highs

Since the beginning of 2026, gold has repeatedly reached new cyclical highs at elevated levels. In early March, the spot gold price remained fluctuating in a high range around $5,200 per ounce. Behind this are multiple resonating factors, including the U.S. dollar and real interest rates, geopolitical tensions and trade frictions, as well as rising central bank gold purchases and investment demand.

1.1.1 The U.S. Dollar and Real Interest Rates

Gold is essentially a non-yielding asset. When the market expects real interest rates to decline or become more volatile, the opportunity cost of holding gold decreases and allocation demand rises. The decline in U.S. Treasury real yields since late February has also supported gold prices.

1.1.2 Geopolitical Tensions and Trade Frictions

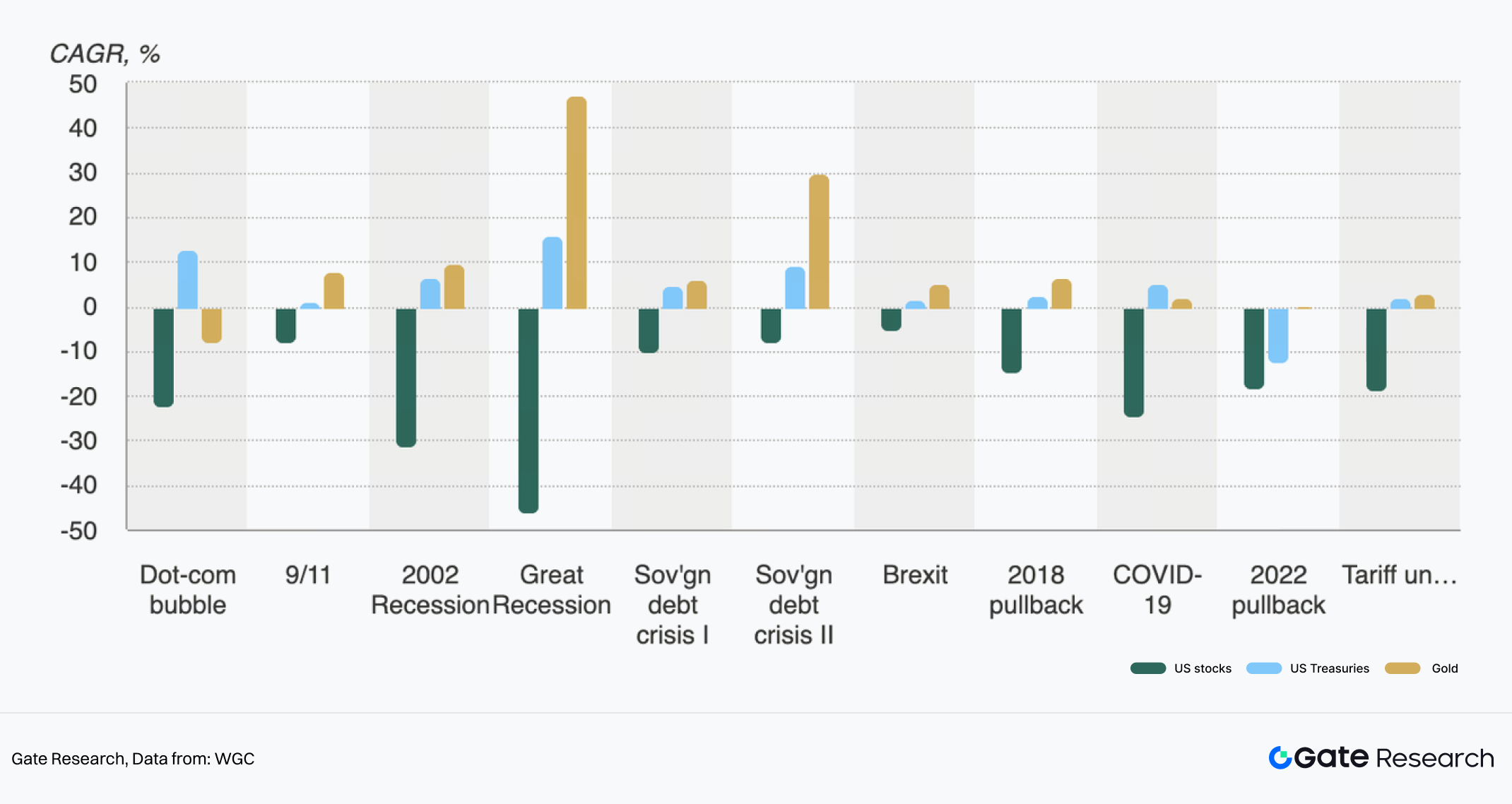

Figure 1: Stocks, bonds and gold performance during various crises

Conflict risks, trade frictions, sanctions, and uncertainties in the energy supply chain directly raise the safe-haven premium, and gold often becomes the preferred defensive allocation for capital. At the same time, tariffs and policy uncertainties also strengthen market demand for gold as a safe-haven asset.

1.1.3 Increase in Central Bank Gold Purchases and Investment Demand

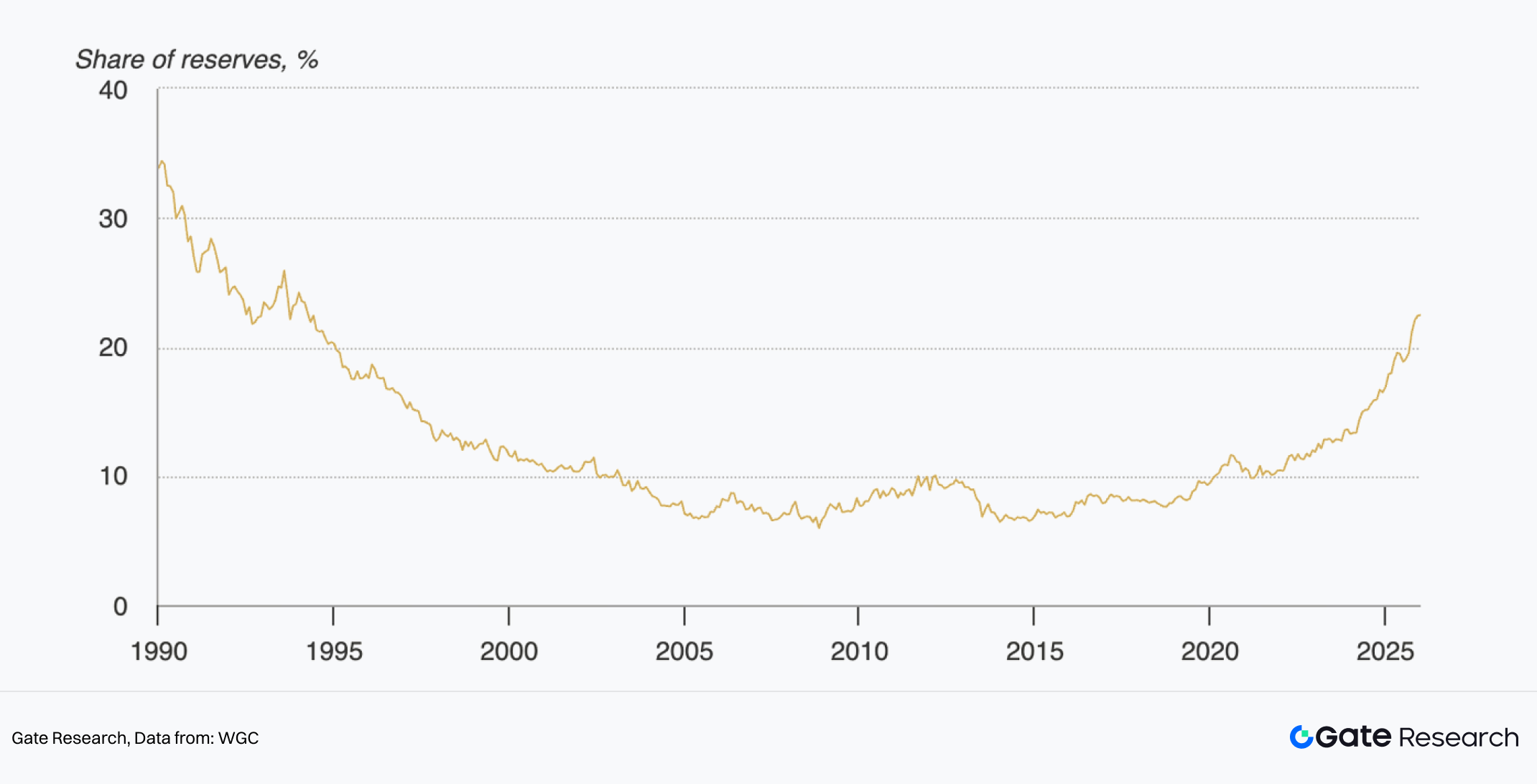

Figure 2: Gold claims as a share of official foreign exchange reserves

According to data from the World Gold Council, total gold demand in 2025, including over-the-counter transactions, exceeded 5,000 tons for the first time, reaching a value of $555 billion. Both demand and gold prices set new records. Among them, investment demand was one of the core drivers. Global gold ETF holdings increased by 801 tons throughout the year, marking the second-highest level in history. Central banks purchased 863 tons of gold during the year, remaining at historically high levels. Based on market value, gold’s share of official foreign exchange reserves has doubled over the past five years to exceed 20%, forming an important underlying support for prices.

1.2 Dual-Channel Growth of ETF Holdings and On-Chain Tokenized Gold

Traditional capital has rapidly flowed into gold ETFs. In January 2026, a record high monthly net inflow was recorded, attracting $19 billion in purchases, pushing ETF holdings to 4,145 tons and AUM to $669 billion, both reaching new historical highs. In an environment of rising gold prices and increased volatility, the allocation and trading attributes of ETFs have both strengthened.

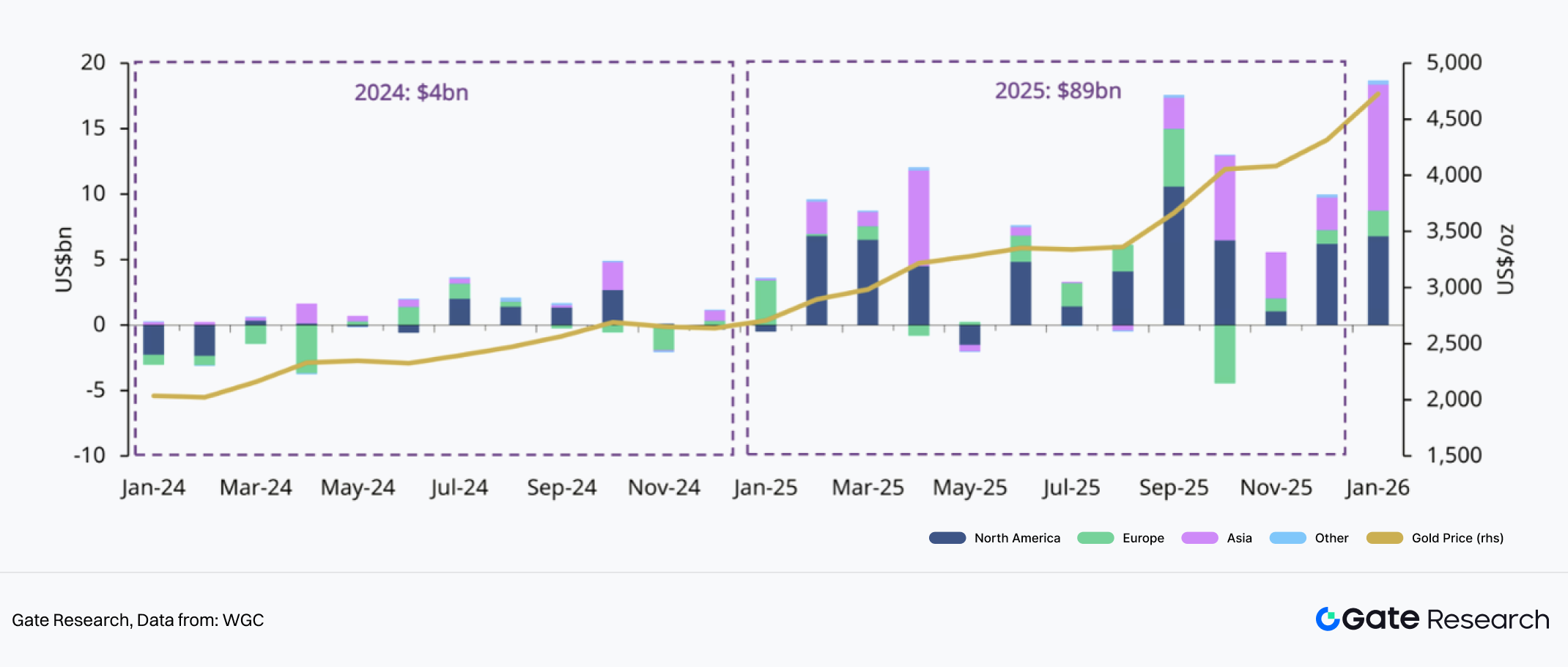

Figure 3: Regional gold ETF flows

It is worth noting that all regions recorded net inflows in January, with North America and Asia significantly driving global demand. At the same time, due to escalating geopolitical and trade tensions, all regions continued to maintain positive momentum.

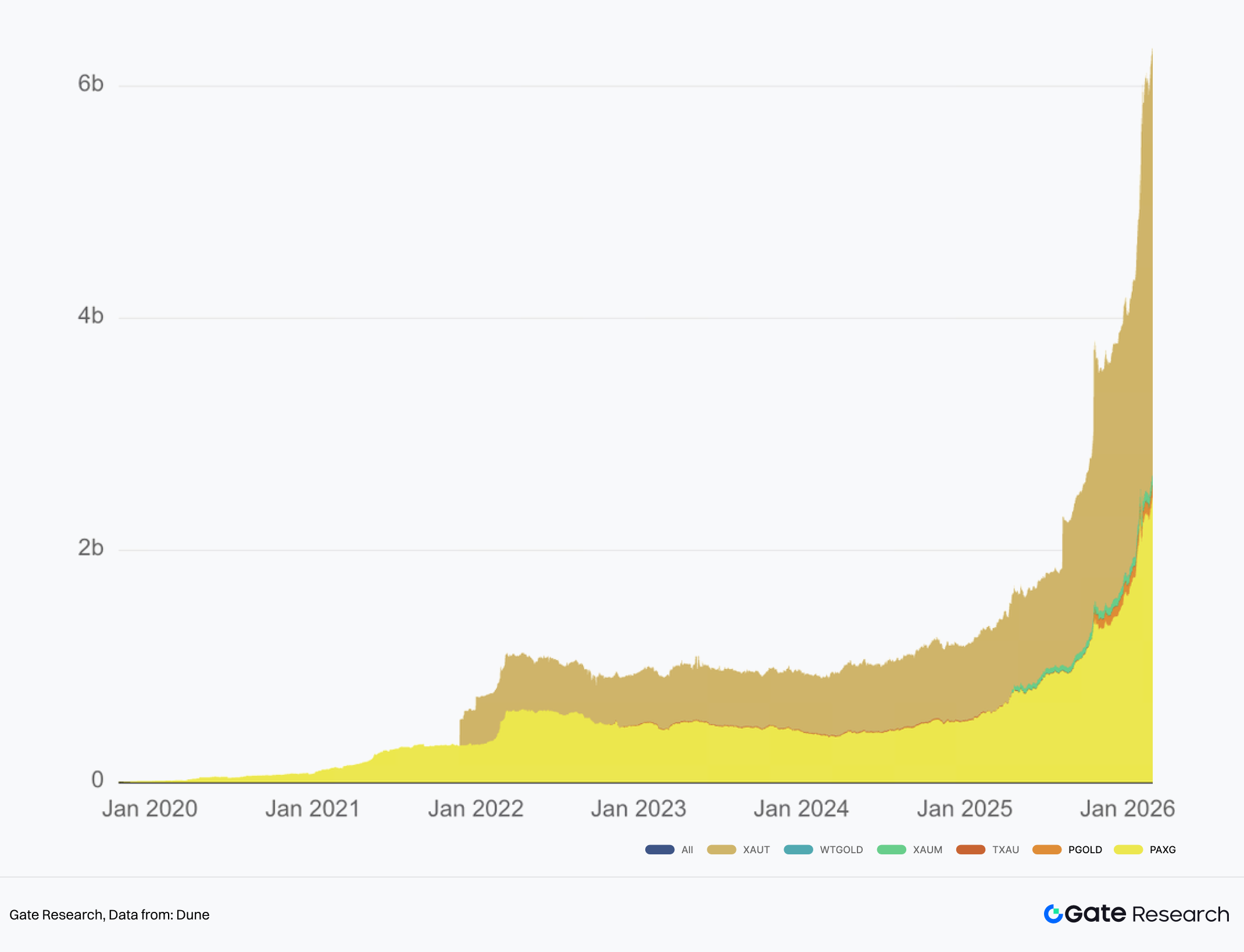

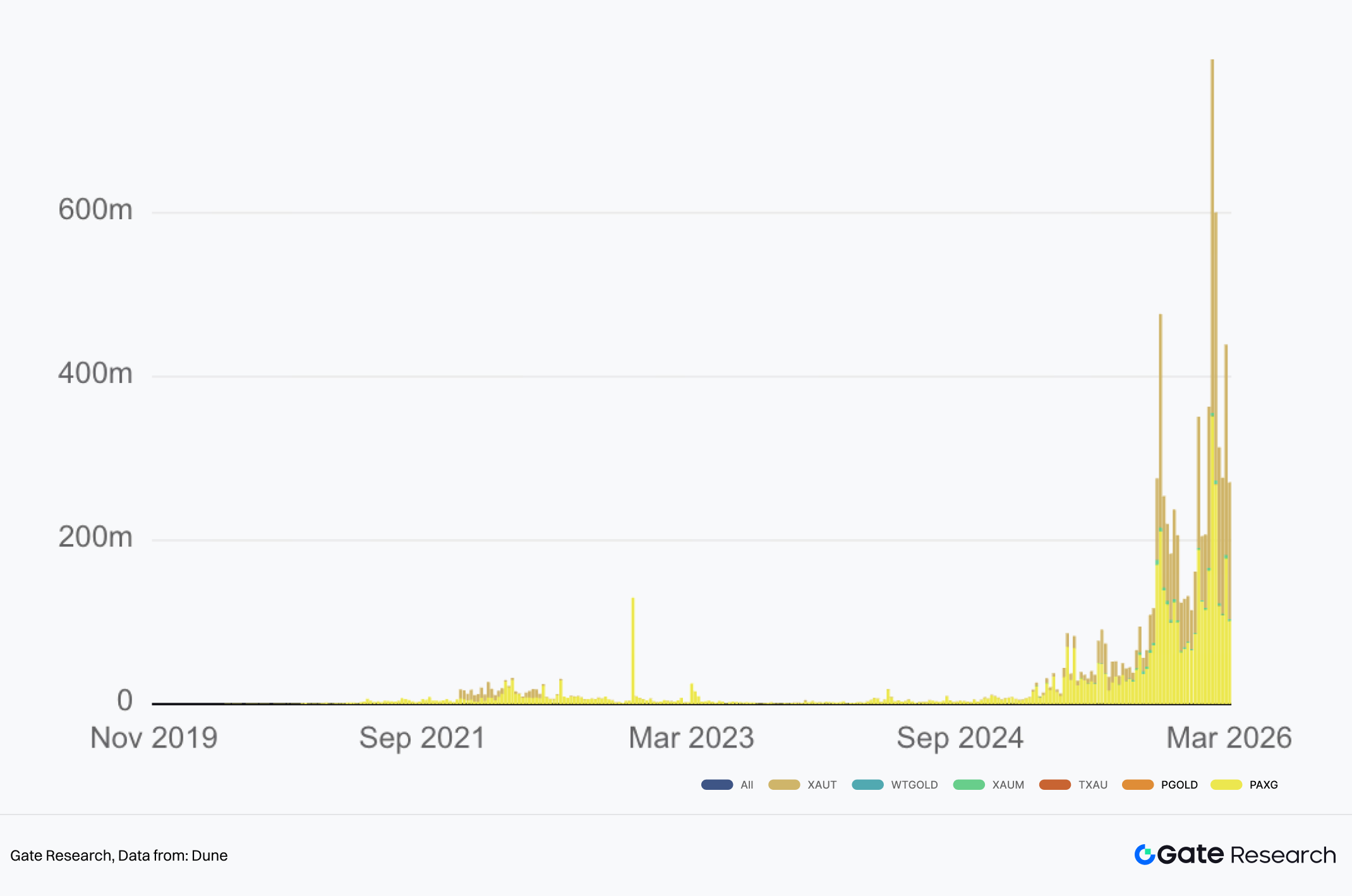

Figure 4: Tokenized Gold AUM

In addition to safe haven sentiment, structural demand for improved financialization efficiency of gold assets has also driven the rapid growth of tokenized gold. Portability, divisibility, 24 by 7 circulation, cross platform trading, and the ability to be embedded into on chain finance including collateralization, lending, and market making are the advantages of tokenized gold. Over the past year, the scale of tokenized gold has grown from slightly above 1 billion dollars to more than 6 billion dollars, representing over 1.2 million ounces of gold locked. It has become an asset category in on chain finance and RWA that cannot be ignored.

It is worth noting that the narrative of “digital gold” seems to no longer belong exclusively to BTC’s store of value imagination, but is extending to on chain physical gold. In a volatile environment, crypto capital is shifting portfolio allocations from a single BTC exposure toward a balanced “BTC + gold” configuration. Tokenized gold provides a pathway that allows investors to remain within the crypto account ecosystem while switching to the risk profile of gold. Tokenized gold relies on infrastructure such as custody, auditing, redemption rights, and compliance. This also foreshadows the selection among different provider solutions and the deployment paths of CEXs in TradFi.

II. Current State of the Tokenized Gold Market

2.1 Market Landscape

Tokenized gold has been one of the fastest growing sub sectors within RWA over the past year, with total market capitalization surpassing 6 billion dollars. However, the market capitalization of tokenized gold is highly concentrated in leading assets. Among them, Tether XAUT has a market capitalization of 3.7 billion dollars, while Paxos PAXG stands at 2.6 billion dollars. Together they account for about 97 percent of the market share. Even within the broader category of tokenized commodities, XAUT and PAXG together account for more than 70 percent.

In addition, trading volume and liquidity are also heavily concentrated in these two leading assets, XAUT and PAXG. On centralized exchanges, XAUT’s global perpetual futures open interest is nearly 600 million dollars, while PAXG’s is close to 450 million dollars, ranking 9th and 12th respectively among perpetual contract assets. On chain DEXs, XAUT and PAXG each contribute hundreds of millions of dollars in weekly trading volume, and their cumulative on chain trading volumes have both exceeded 4 billion dollars, far surpassing other tokenized gold assets.

Figure 5: Weekly DEX Volume on Tokenized Gold

2.2 Comparison with Traditional Gold ETFs

There are systemic differences between tokenized gold and traditional gold ETFs in terms of liquidity, custody, and redemption mechanisms.

At the liquidity level, although both represent trading exposure to gold, their liquidity sources are completely different. The liquidity of gold ETFs essentially comes from two layers. The first is secondary market trading liquidity, including exchange matching, market maker quotations, and intraday trading. The second is the primary market creation and redemption mechanism, which uses “physical gold or cash ↔ ETF shares” for arbitrage to ensure that ETF prices stay close to net asset value. This means the price alignment of ETFs largely depends on whether the market making and arbitrage system operates smoothly and whether trading hours are continuous. The liquidity of tokenized gold is not very different from typical crypto asset liquidity. It includes on chain liquidity and CEX or broker liquidity. The former depends on the size of DEX liquidity pools, while the latter is influenced by exchange order book depth, OTC quotations, and cross platform arbitrage. The core advantages are 24 by 7 trading continuity and easier cross domain transfer and divisibility. However, price alignment relies more on oracles or quotation sources, as well as risk management during periods when the traditional gold market is closed.

At the custody level, ETFs rely on the securities custody system, while tokenized gold relies on physical custody and tokenized rights mapping. Gold ETF holders own fund shares, while the underlying gold is held by designated custodians. Investors usually do not directly access the specific serial numbers of the gold bars. The custody model of tokenized gold emphasizes that users hold on chain certificates that correspond to off chain physical gold. The key issues include whether the gold is held in segregated custody, whether audits are verifiable, and how legal rights are defined. For example, what type of claim rights the token holder actually possesses.

At the redemption level, ETF redemption usually operates through basket level creation and redemption by Authorized Participants. Institutions maintain price alignment through large scale creation and redemption, while ordinary investors typically exit through selling in the secondary market rather than redeeming physical gold. The redemption design of tokenized gold is conceptually closer to physical redemption for end users. However, in practice there are often several constraints, such as minimum redemption thresholds determined by gold bar specifications and transportation or insurance costs, geographic and compliance restrictions including delivery locations, KYC or AML requirements, and fees, as well as differences in redemption paths such as physical delivery or cash settlement. In general, tokenized gold providers commit to full physical redemption, but they do not expect all users to withdraw physical gold. Instead, tokenized gold is intended to function as a transferable certificate that can be moved across platforms and used as an underlying asset in different financial environments.

2.3 Differences in Solutions Among Tokenized Gold Providers

Although tokenized gold generally appears as on chain tokens pegged to physical gold, different issuers have significant differences in compliance pathways, custody structures, redemption mechanisms, and liquidity access. These differences not only determine the credibility and transparency of the product itself but also directly affect its usability within exchanges, DeFi, and institutional trading systems. At present, the market is mainly dominated by two leading solutions, Tether XAUT and Paxos PAXG, while other products form a long tail of supplementary options.

2.3.1 Compliance and Issuance Structure

The most fundamental difference in tokenized gold lies in the issuing entity and regulatory framework. PAXG is issued by Paxos Trust Company. Its issuance structure is closer to a trust based digital asset and is subject to the US regulatory system, strengthening asset transparency through regular audits and disclosures. It emphasizes compliance and institutional trust, making it easier to be accepted by traditional financial institutions and some DeFi protocols. Tether’s XAUT adopts a more offshore oriented issuance structure. Its gold reserves are mainly stored in Swiss vaults and reserve information is disclosed through periodic reports. Regulatory requirements are relatively more flexible, making it more suitable for serving global exchanges and crypto native users.

Overall, trust based issuance emphasizes regulatory compliance and institutional acceptance, while offshore issuance emphasizes global liquidity and trading convenience. These two approaches represent two major development paths for tokenized gold.

2.3.2 Custody and Auditing

The gold reserves of PAXG are stored in vaults recognized by the London LBMA system, and proof of reserves is published monthly. The auditing institutions are usually third party audit firms. Disclosures include the circulating amount of PAXG, the corresponding gold reserves, and custody arrangements, while also providing on chain query tools. The gold reserves of XAUT are mainly stored in Swiss vaults and reserve reports disclose the total reserve amount and token issuance amount. However, the reporting frequency and level of disclosure detail are slightly lower compared with PAXG.

2.3.3 Redemption

Differences in redemption mechanisms among projects are mainly reflected in minimum redemption size, redemption methods, and fee structures.

Since physical gold is usually delivered in LBMA Good Delivery bars as the standard unit, redemption typically involves a minimum quantity threshold. The token unit of PAXG is 1 token representing 1 ounce of gold. After meeting a certain threshold of 430 PAXG plus fees, users can redeem the corresponding LBMA gold bar. The practical minimum redemption size is usually close to one standard gold bar, approximately 400 ounces with a weight range of 350 to 430 ounces. The specific process must be completed through the issuer. In addition, Paxos allows users to convert PAXG into smaller gold products such as gold coins or small gold bars, or redeem PAXG for US dollars based on the prevailing gold price. A key feature of PAXG is the relatively diversified redemption pathways and the provision of a gold bar serial number lookup system, allowing holders to verify the corresponding gold reserves.

XAUT also uses 1 token representing 1 ounce of gold as the base unit and allows fractional division down to about 0.000001 ounce. Physical redemption usually takes place at designated Swiss vaults and must meet the required minimum quantity threshold, typically equivalent to the size of a standard gold bar. Redemption requires completion of KYC and AML procedures and users must bear transportation, insurance, and vault delivery costs. Compared with PAXG, XAUT redemption is more oriented toward institutions or large investors, with fewer retail level redemption options.

Although tokenized gold provides a pathway for physical redemption, in practice most users enter and exit positions by trading tokenized gold on exchanges or secondary markets rather than withdrawing physical gold bars. Therefore, the primary role of the redemption mechanism in practice is not frequent usage but rather providing price anchoring and asset credibility. As long as the market believes the tokens can be redeemed for the corresponding gold reserves, their price can maintain a long term peg with spot gold.

III. The Gold Index Competition Between CEX and Perp DEX

In this round, trading platforms collectively launching gold indices or gold perpetual contracts is essentially a competition for gold price discovery power and the account entry point for gold risk exposure. What users want is the ability to switch risk from high volatility assets to safe haven assets at any time within the crypto margin system. What platforms want is to keep the trading demand for traditional assets within their own margin and liquidation systems.

As a result, platforms naturally prefer “synthetic gold” such as index perpetuals or CFD like price exposure structures. These products rely only on reliable indices and risk control models, and do not need to bear the legal and operational complexity brought by physical custody and redemption. In contrast, tokenized gold such as XAUT and PAXG spot is closer to an asset layer RWA. It requires custody, auditing, redemption rights, and compliance boundaries. Its growth is slower but its asset properties are stronger.

Therefore, the real market evolution shows a dual track structure. On one hand, CEX platforms provide spot and derivatives trading for XAUT and PAXG. On the other hand, they expand gold index perpetuals such as XAUUSDT in order to cover a wider range of hedging and trading demand.

3.1 CEX: Index Composition and “Market Closure Switching” Determine Product Credibility

The biggest contradiction of synthetic gold is that perpetual contracts trade 24 by 7, while the underlying traditional gold spot market and its main trading sessions are not 24 by 7. To address this mismatch, CEX platforms generally make engineering trade offs between continuous trading experience and alignment with traditional gold price benchmarks. As a result, two mainstream approaches have emerged. One approach directly incorporates on chain physical gold tokens such as XAUT and PAXG into the index, sometimes allowing them to dominate pricing when traditional markets are closed. The other approach relies more on traditional data providers and oracle networks to construct an external gold price index, using tokenized gold only as a low weight reference for validation.

On a certain O** exchange, on chain gold is directly included in the components and weightings of the XAU USDT index. The XAU USDT index is used to calculate funding rates, price limits, and mark prices. After a later adjustment, the index was divided into two sets of weightings for normal trading hours and periods when the gold spot market is closed. During normal trading hours, the XAU USD price from a certain exchange accounts for 20 percent, while the remaining 80 percent comes from XAUT USDT and PAXG USDT markets across multiple exchanges. During market closure periods, the weight of that exchange is reduced to 0 percent, and the index is entirely composed of order book sources from tokenized gold markets, each accounting for 25 percent. It is worth noting that on this exchange the component price itself is derived from a weighted average of several major commodity price providers, and the platform retains discretion to adjust the weights.

This type of market closure switching design, where TradFi sources fall to 0 percent and tokenized gold rises to 100 percent, effectively turns the synthetic gold index into a composite price index of XAUT and PAXG during weekends or traditional market closure periods. The continuous 24 by 7 trading of tokenized gold fills the pricing gap caused by the discontinuity of traditional markets. The advantage is stronger continuity and tradability. The trade off is that the index inevitably introduces factors unrelated to the fundamentals of gold, such as crypto market exchange risk premiums, liquidity discounts or premiums, and cross platform arbitrage efficiency.

Another exchange, B**, adopts a different route for its XAUUSDT index, relying primarily on external gold price indices with tokenized gold as a secondary reference. The Price Index of XAUUSDT is composed of three data sources, including Dxfeed XAU USD AFX, Massive C.XAU USD, and Pyth XAU, each accounting for 33 percent. Meanwhile, the exchange’s own PAXGUSDT market accounts for only 1 percent. According to the exchange’s public documentation, PAXG is included in the index but with a very small weight of 1 percent. It functions more as a mechanism to enhance 24 by 7 availability or serve as a verification reference rather than as the main pricing driver. At the same time, the exchange further disclosed key aspects of its risk engineering for TradFi perpetual products. During periods outside traditional trading hours, the mark price uses EWMA smoothing to reduce unnecessary liquidations caused by sudden volatility, and constraints are set on the deviation between the mark price and the index price. For XAUUSDT, the example deviation limit is ±3 percent in order to control systemic risk.

3.2 Perp DEX: Weighting Is “Folded” into the Oracle Network, and Competition Shifts to Feed Quality

On the Perp DEX side, price sources are usually not publicly displayed in the form of order book weightings from specific exchanges as they are on CEX platforms. Instead, they are folded into the oracle layer. Perp DEX platforms directly reference the aggregated result of a gold price feed as the anchor for mark prices, funding rates, or liquidation mechanisms. Taking the Pyth XAU/USD feed as an example, its Insights page shows that this feed involves participation from 27 publishers.

This means that the “weighting” in Perp DEX systems is often not determined by a fixed weighting table defined by the trading platform itself. Instead, it is determined by the aggregation mechanism of the oracle network. The key factors include the composition of feed publishers, update frequency, outlier handling, confidence intervals, and how the platform manages deviations between oracle prices and executed market prices during extreme market conditions.

Overall, the so called competition between CEX and DEX in the gold market is essentially a competition for index governance power. The specific structure of the index determines the outcome. This includes the weight assigned to tokenized gold such as XAUT or PAXG in the index components, whether market closure weight switching exists, which data providers or quotation sources supply the TradFi price feeds, and the publisher composition and aggregation mechanism of oracle feeds. These structural choices determine whether the product behaves more like a standard gold price index or more like a composite price of on chain gold during weekends, market closures, and extreme volatility.

This will also directly shape the trading strategy space for users, including how the basis between the index and XAUT or PAXG spot evolves, how funding rates reprice market closure risk, and how index differences across platforms create arbitrage opportunities and risk management requirements.

IV. Gate’s Practical Approach: Building a “Full Stack Gold Market”

It becomes clearer if gold demand is separated into two layers. The asset layer emphasizes physical anchoring and transferable certificates, leaning more toward long term holding and asset allocation. The trading layer emphasizes synthetic exposure, 24 by 7 risk management, and leveraged tools, leaning more toward hedging, trading, and cross market strategies. Gate’s approach is to integrate both layers into the same product matrix and margin system, forming a gold trading stack that expands step by step from spot, leveraged ETF products, and CFDs to macro perpetual contracts and Perp DEX.

4.1 Spot: Bringing Physical Anchoring into the Trading Account

At the asset layer, Gate already provides spot trading access for tokenized gold. This includes direct trading of XAUT/USDT spot, while the platform also features PAXG related pages and trading campaigns. Within the Gate crypto account system, users are already able to hold certificates of physical gold that can be transferred on chain. This creates a directly tradable underlying asset anchor for future risk switching, cross asset allocation, or hedging combinations with derivatives.

Beyond derivatives contracts, Gate also extends directional gold trading into a lighter leveraged product format. The platform has launched leveraged tokens such as XAU3L and XAU3S, as well as XAG3L and XAG3S. Compared with perpetual contracts, these products package leverage and rebalancing mechanisms into a token format that can be traded in the spot market. This structure is suitable for traders who want amplified exposure while reducing the operational complexity associated with margin and liquidation. From the platform perspective, it further completes product depth by covering the same underlying asset across multiple product forms.

4.3 TradFi CFD: Integrating Traditional Trading Habits and Asset Expansion into a Single Entry

On the channel closer to traditional finance, Gate launched Gate TradFi, bringing CFDs for gold, foreign exchange, stock indices, commodities, and equities into its product line. These products are accessible through both the Gate App and MT5. The account unit USDx is pegged 1 to 1 with USDT, using USDT as the underlying funding asset to trade TradFi price-based products. The system also adopts mechanisms closer to traditional CFD markets, including fixed trading sessions and market closures, overnight fees, cross margin, and liquidation based on margin ratio.

4.4 Perpetual Contracts: Using XAU Perpetuals to Solve the 24 by 7 Trading and Traditional Session Gap

Gate launched a metals futures section earlier this year, offering USDT margined perpetual contracts for assets such as gold XAU/USDT and silver XAG/USDT. The platform highlights leverage of up to 50 times and continuous 24 by 7 trading, integrating traditional metal assets into the crypto derivatives framework. Gate’s metal perpetual contracts use price indices derived from multiple comprehensive metal markets to enhance stability and verifiability, while maintaining a reasonable linkage between contract prices and spot prices.

4.5 Perp DEX: Extending the Full Stack into On Chain Infrastructure

Within the Gate ecosystem there is also a narrative with greater potential compared with other CEX platforms. Gate DEX includes Gate Perp DEX, a self developed decentralized perpetual trading platform built on Gate Layer, which already supports hundreds of trading pairs. Gate Perp DEX currently covers metal assets including gold XAU perpetuals and silver XAG perpetuals, continuing to expand Gate’s capacity to support gold and macro assets while extending its presence into the on chain ecosystem.

V. Conclusion

Against the backdrop of rising macro uncertainty and expanding demand for gold allocation, the gold market is experiencing three parallel structural changes:

-

Capital Side: The Re Financialization and Strengthening Trading Attributes of ETFs In January 2026, global physical gold ETFs recorded a record inflow. This indicates that gold is not only a safe haven allocation but is also once again becoming a financial instrument that can be traded, rebalanced, and moved across regions.

-

Tokenized Gold: Assetization and Derivatives Development Under a Duopoly Structure Tokenized gold is not an on chain version of ETFs. Instead, it upgrades gold exposure from a position held within centralized brokerage accounts into an asset certificate that can be transferred, divided, and embedded into financial contracts. XAUT and PAXG, as the most important tokenized gold assets, form the main foundation of market scale and liquidity. In derivatives markets, they are also seeing considerable open interest and trading demand. The market is increasingly focused on how to express gold risk exposure within the crypto account ecosystem.

-

Platform Side: The Core Competition Between CEX and DEX Is Index Governance The key to synthetic gold index perpetual products is not only multi-source data but also the composition and weighting of data sources, market closure switching rules, mark price risk control constraints, and the quality of oracle feeds. These structural details determine the pricing behavior of products during market closures and extreme volatility, which in turn determines the basis, funding rates, and arbitrage opportunities.

Returning to the Gate approach, Gate has already structured its gold trading ecosystem around multiple product forms. These include tokenized gold spot, leveraged ETF products, TradFi CFDs, metal perpetual contracts, and on chain Perp infrastructure. The objective is to keep gold holding, trading, leverage, and hedging within the same product matrix and account system, forming a more complete gold trading stack.

References:

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.