As global demand for cross-border remittances rises, traditional payment systems are increasingly hampered by high fees and slow processing times. In emerging markets, where banking access is limited but mobile networks are ubiquitous, the telecom finance model is emerging as a compelling alternative.

Leveraging the growth of blockchain and digital assets, Telcoin enables more cost-effective and efficient cross-border remittances by integrating mobile operators, blockchain infrastructure, and mobile wallets into a unified payment network. This approach has led to the development of foundational platforms like the Telcoin Application Network (TAN), opening new technological pathways for global mobile financial services.

The Telcoin cross-border payment network is built on mobile communications, using mobile wallets provided by operators as the primary user gateway to enable rapid, international fund transfers. This telecom finance network integrates mobile communications infrastructure with blockchain-powered payments at its core.

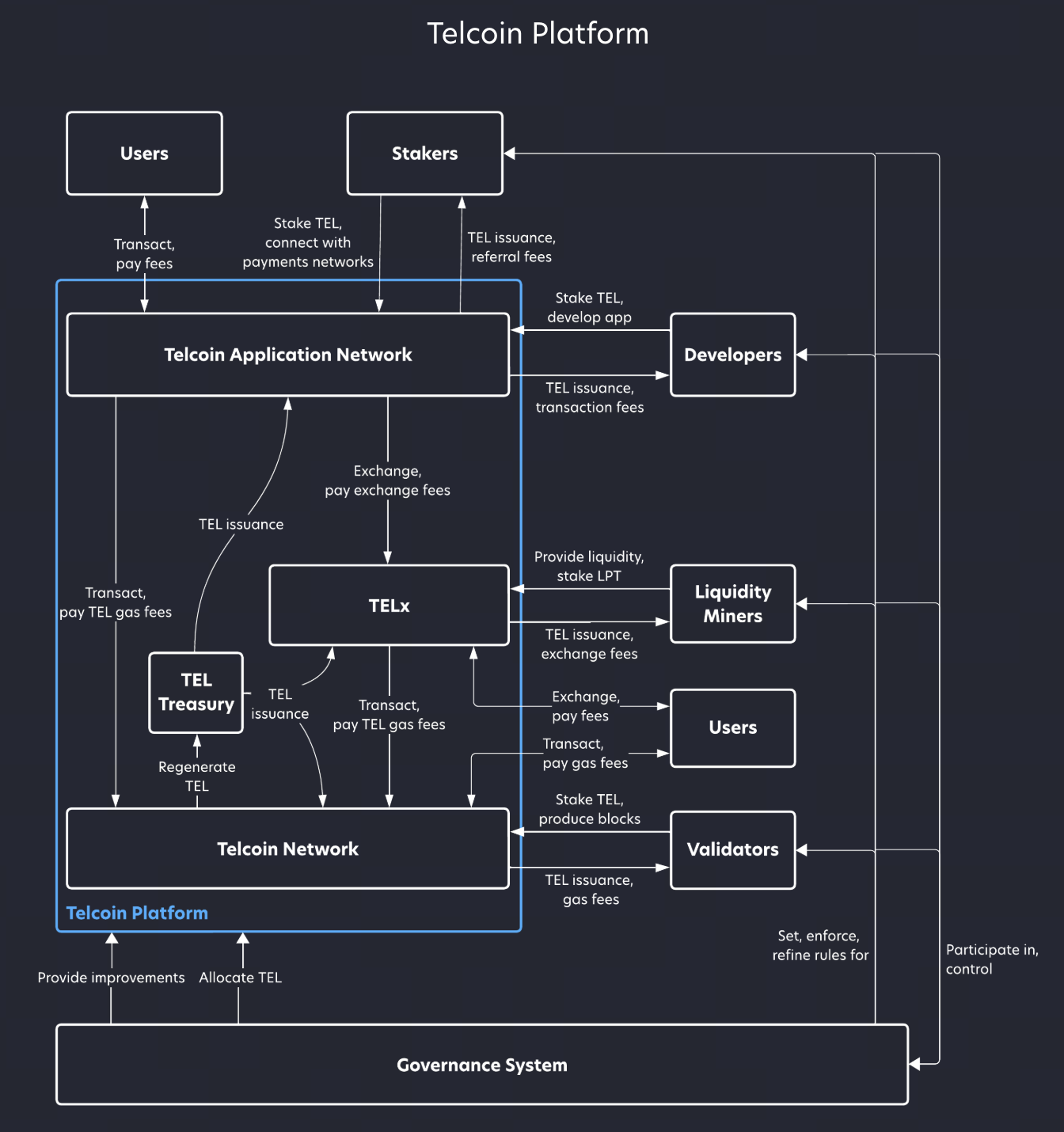

Telcoin’s architecture features a multi-layered structure: the Telcoin Network manages fund transfers and settlements, TELx handles asset exchange, and the Telcoin Application Network (TAN) serves as the user access layer, delivering mobile apps and wallet services. This layered design allows Telcoin to support asset exchange, fund movement, and app integration simultaneously.

The Telcoin Application Network (TAN) is the main user entry point. TAN comprises various mobile apps, typically built by operators or partner developers, offering non-custodial wallets, cross-border payments, and digital asset management. This structure lets users participate in cross-border payments without needing a bank account.

As TAN expands, more apps, developers, and users join, creating network effects that drive Telcoin’s cross-border payment scale. This expansion at the application layer is central to understanding both Telcoin’s architecture and its ecosystem growth trajectory.

Source: telcoin.org

Key Participants in Telcoin Cross-Border Payments

The Telcoin cross-border payment network relies on several participant roles that collectively enable seamless international fund flows. Understanding these roles is critical to grasping how the Telcoin network operates.

The first group is Mobile Network Operators (MNOs), who provide mobile wallet services and serve as the primary gateway for users entering the Telcoin network. With large user bases in many countries, MNOs allow Telcoin to rapidly expand its coverage.

| Participant |

Main Roles & Responsibilities |

Core Contribution to Telcoin Network |

Relationship with Telcoin |

Significance |

| Mobile Operator (MNO) |

Provides mobile wallet services and is the main entry point for users |

Leverages a large user base for rapid network expansion |

Connects to the Telcoin payment network via mobile wallet |

Solves user access and coverage challenges, enabling rapid scaling |

| App Developer |

Builds mobile apps on TAN, offering payments and asset management |

Expands the app ecosystem and drives real-world payment use |

Develops and integrates Telcoin-powered apps |

Enhances user experience and supports diverse ecosystem growth |

| Validator Nodes & Stakers |

Stake TEL tokens to participate in network consensus and validation |

Secure the network and ensure decentralized operation |

Stake TEL tokens for governance and validation |

Provide incentives for long-term network security and stability |

| End User |

Uses mobile wallets for remittance, storage, payments, and trades |

Drives transaction demand, liquidity, and network scale |

Uses mobile wallets and Telcoin apps |

Core value driver, determines network adoption |

App developers form the next group, building mobile apps on TAN to deliver payments, asset management, and financial services. These apps are vital to expanding the Telcoin ecosystem and driving real-world usage.

Validator nodes and stakers are also essential. By staking TEL tokens, they help operate the network and secure cross-border payment systems. This mechanism is closely tied to Telcoin’s tokenomics and underpins the network’s incentive structure.

End users complete the ecosystem, using mobile wallets for cross-border remittance, asset storage, and trading. As user participation grows, so do Telcoin’s transaction volume and liquidity.

How Telcoin Differs from Traditional Cross-Border Payment Systems

Traditional cross-border payments rely on banks and international networks like SWIFT, involving multiple intermediaries—sending, clearing, and receiving banks—which makes the process complex.

Telcoin’s model leverages blockchain and mobile wallets for peer-to-peer transfers, allowing funds to move directly between wallets in different countries and minimizing intermediaries.

Traditional remittance fees are often high, especially in emerging markets. Telcoin’s blockchain settlement significantly reduces costs and enhances transparency.

Settlement times with banks can span days, while Telcoin’s network typically completes transactions much faster—making it ideal for high-frequency, low-value cross-border payments.

These distinctions often draw comparisons between Telcoin, stablecoin payments, and crypto-based remittance networks. Understanding these differences clarifies Telcoin’s unique positioning in the cross-border sector.

Telcoin and Mobile Network Operator (MNO) Collaboration

Mobile operators are integral to the Telcoin network. Through partnerships, Telcoin enables operators to offer cross-border financial services via mobile wallets.

In many emerging markets, operators already provide mobile payments and airtime top-ups. Telcoin builds on this foundation, enabling international remittances directly from mobile devices.

Such partnerships typically involve technical integration and financial service collaboration, with operators embedding Telcoin into their apps to deliver seamless payment experiences.

This collaboration fuels Telcoin’s network growth: as more operators join, user numbers and cross-border reach expand.

Telcoin Cross-Border Remittance Process Explained

A typical Telcoin remittance starts with a mobile wallet. Users select the destination and amount in the app, then submit a transaction request.

The request routes through TAN to the Telcoin Network for processing, with TELx facilitating asset exchange and liquidity management as needed.

Settlement occurs on the blockchain, transferring funds to the recipient’s mobile wallet in the target country. The recipient accesses funds through their app.

This process is faster and involves fewer intermediaries than traditional remittance, reflecting Telcoin’s technical and payment architecture.

Advantages and Potential Challenges of the Telcoin Payment Network

Telcoin’s main advantages include broad mobile network coverage—critical in countries with limited banking infrastructure—and a large potential user base.

Transaction costs are lower, thanks to blockchain and mobile wallets, which streamline processes and cut fees.

The network is highly scalable: as more operators and apps join, Telcoin’s reach and utility grow.

Challenges remain, such as regulatory compliance, cross-border payment rules, and the pace of operator partnerships, all of which could impact network expansion.

Summary

Telcoin merges mobile operator reach with blockchain technology to create a telecom finance cross-border payment network. By using mobile wallets, it streamlines fund transfers and reduces reliance on traditional intermediaries.

The Telcoin Application Network (TAN) acts as the user gateway and accelerates cross-border payment adoption. With growing operator and user participation, Telcoin’s network continues to scale—offering a novel solution for cross-border payments and establishing a unique position in mobile finance.

FAQ

What are the core advantages of Telcoin cross-border payments?

Telcoin delivers low-cost remittances, mobile wallet access, and the efficiency of blockchain settlement.

Does Telcoin require a bank account?

No. In many regions, users can send and receive cross-border payments via mobile wallets without a bank account.

What is the Telcoin Application Network (TAN)?

TAN is Telcoin’s application layer, comprising multiple mobile apps that provide access to cross-border payments and financial services.

Does Telcoin collaborate with mobile operators?

Yes. Telcoin partners with mobile operators, enabling users to make cross-border payments directly from their phones.

How does Telcoin differ from traditional cross-border remittance?

Telcoin uses blockchain and mobile wallets for payments, while traditional remittance depends on banks and intermediaries.