Event Overview: Tom Lee Reinforces 7,700 Target

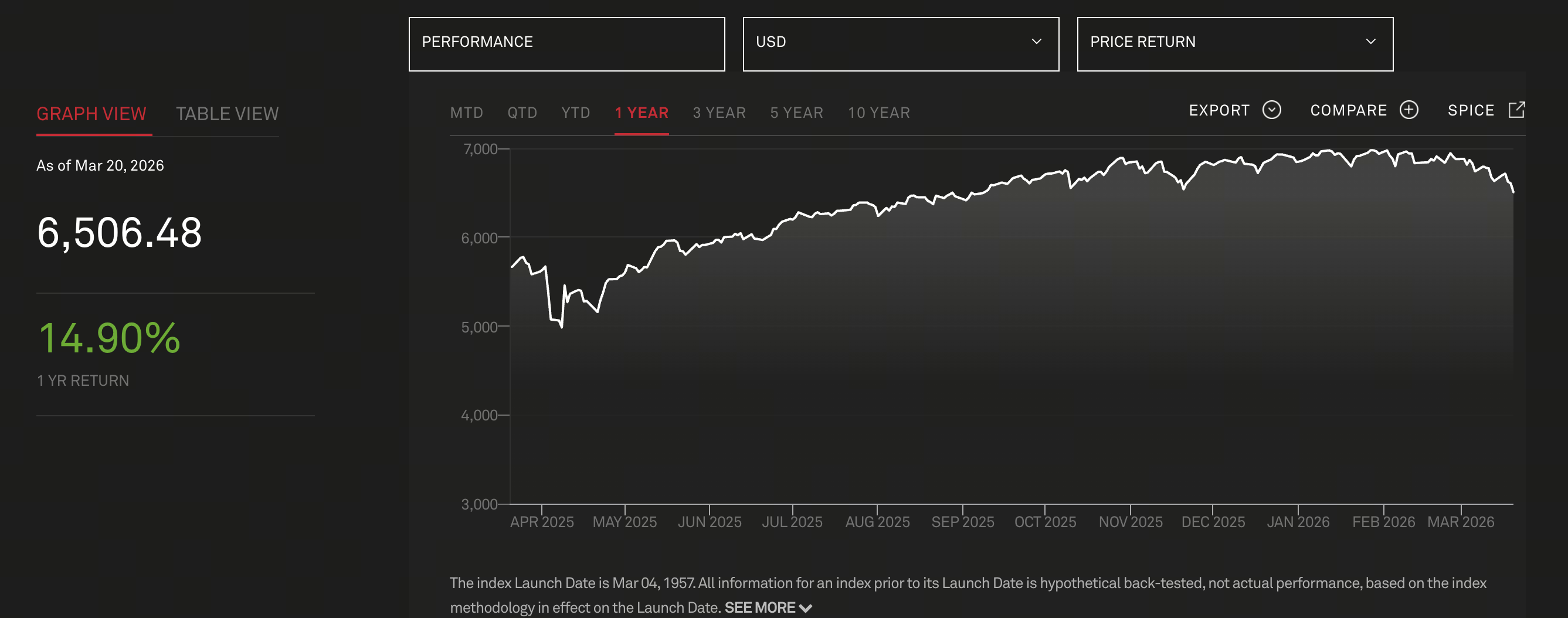

Image source: S&P 500 Index

Image source: S&P 500 Index

In March 2026, Tom Lee, co-founder of Fundstrat, reaffirmed in a media interview that he is holding firm on his year-end S&P 500 target of 7,700 points. This projection is part of his long-term market framework—not a temporary adjustment.

He emphasized that the target itself is a “conservative estimate,” grounded only in moderate price-to-earnings ratio expansion and excluding scenarios of extreme liquidity easing or explosive earnings growth.

At the same time, he put forward a view that sparked widespread market discussion: Historically, war has often been a buying opportunity.

Core Analysis: Why War Becomes a “Buy Point”

Tom Lee’s logic is not simply driven by sentiment; it rests on three key mechanisms:

-

Markets Price in Risk Ahead of Time: Wars typically unfold gradually rather than erupting suddenly. The market begins adjusting asset prices before conflicts officially break out.

-

Risk Premium Declines After Uncertainty Is Released: Once a conflict materializes and the worst-case scenario is confirmed, the market enters a phase of “restored certainty.”

-

Policy and Liquidity Tend to Shift Toward Easing: In wartime, fiscal and monetary policies generally aim to stimulate the economy, providing support for asset prices.

He pointed out that, in the past eight major wars, markets typically started forming a bottom early in the conflict, rather than rebounding only after the war concluded.

Historical Review: The Cyclical Relationship Between War and the Stock Market

Historical data shows that war’s impact on the stock market unfolds in distinct stages:

-

Early Stage (Escalation): Market volatility intensifies, risk assets decline

-

Mid Stage (Outbreak): Panic peaks, markets gradually stabilize

-

Late Stage (Policy Stimulus): Economic reconstruction and fiscal expansion drive gains

For instance, during World War II and the Gulf War, the stock market established a bottom in the early phase of conflict.

This phenomenon reflects that the market is more focused on “changes in expectations” than on the event itself.

Current Market Structure: Has Risk Already Been Priced In?

Tom Lee underscored that the current market is not in a phase of “unpriced risk”; instead, it has already undergone structural adjustment:

-

Energy sector: Three-year bear market

-

Financial sector: Persistent weakness

-

Tech giants (MAG-7): Entering an adjustment cycle

These sectors together account for roughly 70% of the S&P 500, indicating that the market as a whole has already undergone significant risk reduction.

Furthermore, gold’s parabolic surge ahead of the conflict signals that capital has already moved into safe-haven assets. The market isn’t ignoring risk—it has already absorbed it.

Macro Variables: Liquidity, Interest Rates, and Earnings Expectations

The foundation for the 7,700 target is not just sentiment or historical precedent, but three major macro variables:

-

Liquidity Cycle: If the Federal Reserve ends tightening or shifts to easing, it will provide critical support for the stock market.

-

Corporate Earnings Growth: Advances in AI and automation are boosting productivity, creating structural growth opportunities for corporate profits.

-

Valuation Expansion: As interest rates decline, the market is willing to assign higher valuation multiples.

Sectors and Capital Flows: Who Will Drive the Next Rally?

From a capital structure perspective, future upward momentum may come from three directions:

-

Technology and AI sectors: Remain the core narrative

-

Traditional industries that have undergone substantial adjustment: Possess potential for valuation recovery

-

Institutional capital returning: After prior risk reduction, positions remain relatively low

It’s important to note that a market rally does not necessarily require a “broad bull market.” It may manifest as structural rotation and pockets of strong performance.

Risks and Uncertainties: The Market Is Not Unilaterally Optimistic

While Tom Lee remains optimistic, his logic does not imply the market is risk-free:

-

Geopolitical conflicts may further escalate

-

A rebound in inflation could limit monetary policy flexibility

-

Excessive AI valuations may trigger corrections

-

If corporate earnings fall short, the foundation for gains will weaken

Therefore, the view that “war is a buy point” is best applied to phased, incremental allocation—not blind bottom-fishing.

Forward Projection: The S&P 500’s Path to 7,700

Based on current information, the S&P 500’s path to 7,700 may involve:

-

Short-term volatility (driven by geopolitical risk)

-

Mid-term stabilization (risk pricing completed)

-

Long-term rally (driven by liquidity and earnings)

Throughout this process, market narratives will gradually shift from “risk” to “opportunity.” “Ultimately, the market’s focus is not on the crisis itself, but on the growth potential that follows.”

Conclusion

Tom Lee’s 7,700-point forecast for the S&P 500 is not simply an optimistic outlook, but a comprehensive assessment based on historical patterns, market structure, and macro variables.

The idea that “war is a buy point” reveals a deeper logic: market rallies often emerge from uncertainty, not certainty.

For investors, the key is not to judge the war itself, but to identify:

Only when these three factors converge will a genuine market rally take shape.