I. Introduction: Why “NFTs Are Dead” and “NFTs Will Be Reborn” Are Both Oversimplifications

Over the past few years, NFTs have followed the classic trajectory of new technology: a burst of innovation, capital inflows, overblown valuations, a sentiment drawdown, and then rational rebuilding.

As a result, two common conclusions miss the mark:

-

“NFTs are dead” overlooks the foundational technology that has taken root. Even as total trading volume has fallen sharply from its peak, NFTs as an on-chain standard for ownership verification and transfer have not disappeared; instead, they’ve matured in areas like toolchains, Wallet integration, cross-chain indexing, and data interfaces.

-

“NFTs will make a full comeback” is also too optimistic. Demand will not automatically return to past highs, and projects lacking genuine use cases and cash flow support will continue to be eliminated in low liquidity environments.

A more accurate perspective is that NFTs are shifting from an “asset class narrative” to serving as “digital equity infrastructure.” Rather than representing just a category of image Assets, NFTs are becoming a universal layer for expressing “who owns what rights, when those rights are available, how they’re transferred, and how they’re settled.”

II. Market Structure Reassessment: From Aggregate Decline to Layered Growth

In the post-bubble era, evaluating the NFT market requires looking beyond total trading volume to the underlying structure:

-

There’s a clear divergence between leading and tail-end Assets, with trading depth concentrated in a handful of collections.

-

Different blockchain ecosystems are specializing, and both users and Assets are migrating across platforms more frequently.

-

Primary issuance (mint) enthusiasm is waning, but “high-quality, high-certainty equity” Assets in secondary markets are holding up relatively well.

-

Trading behavior is shifting from “broad speculation” to “event-driven and liquidity-driven” activity.

This means the industry must update its metrics. In the past, “floor price increases” explained everything; today, more relevant indicators include: unique active Wallets, Maker depth, transaction persistence, Royalties enforcement rates, platform migration costs, and true retention and repurchase rates.

When these metrics improve, the industry achieves sustainable growth—not just a short-term rebound.

Whether it’s OpenSea, Magic Eden, or native marketplaces on various chains, a clear trend has emerged:

The profit margin from “simple trade matching” is shrinking, forcing platforms to expand both upstream and downstream.

-

Upstream involves issuance and tools: Launchpad, contract templates, identity and whitelists, Creator analytics dashboards.

-

Downstream covers settlement and distribution: cross-chain aggregation, payment channels, Recommended systems, API services, Risk Control, and anti-fraud.

This underscores a shift in platform value from “how much Trading Fee is collected” to “how much end-to-end friction can be reduced.” In a low fee rate environment, user retention hinges not on slogans, but on lower trading costs, higher execution efficiency, greater fund security, and superior discovery mechanisms.

Leading platforms of the future will function more like “on-chain infrastructure providers for content and Assets” than traditional “trading websites.”

IV. Value Anchors Shift: From Scarcity Narratives to Equity Cash Flow

NFTs’ first phase was built on “scarcity + community consensus.” The second phase must answer: “Where does the equity come from, and how is value realized?”

Sustainable value typically derives from three anchors:

-

Usage rights: For example, in-game items, event tickets, or digital passes—holding confers consumable utility.

-

Return rights: Such as Royalties sharing, revenue rebates, or membership discounts—holding is linked to cash flow or cost savings.

-

Governance/participation rights: Such as community voting, collaborative content creation, or priority access—holding grants organizational participation.

When NFTs put “rights objects, exercise conditions, and transferability rules” on-chain, their valuation becomes less sentiment-driven and more aligned with “equity asset pricing.”

This also explains why, after the speculative frenzy fades, high-quality projects persist: they have clear, explainable rights structures—not just a single narrative.

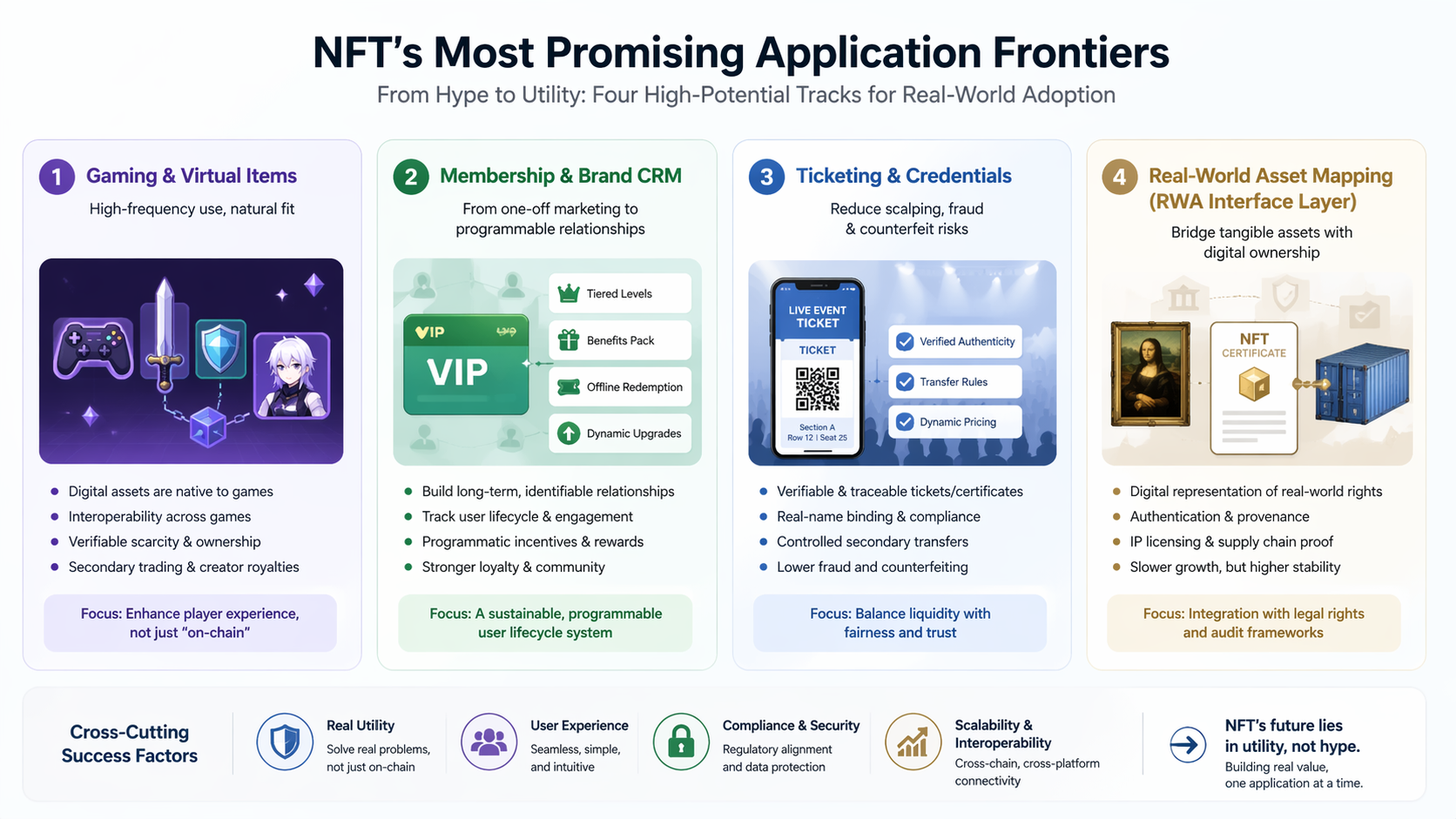

V. Four Most Likely Application Tracks

Gaming and Virtual Items: High-Frequency, Usage-Driven Adoption

Gaming offers the most practical application for NFTs. The logic is straightforward: Assets are already digital, users are used to trading, and both identity and items require verifiable records.

The real question isn’t “should it be on-chain,” but “does it enhance the player experience?” Key drivers include cross-game interoperability, verifiable scarcity, secondary market equity, and Creator revenue sharing.

Brands and content creators are increasingly prioritizing “sustainable user relationships” over one-off airdrops. If NFT memberships can integrate tiering, bundled benefits, offline redemption, and dynamic upgrades, they could become long-term CRM solutions.

The goal isn’t just to issue a badge, but to build a “recognizable, traceable, and incentivized” user lifecycle system.

Ticketing and Credentials: Reducing Scalping and Counterfeiting

NFTs’ verifiable and traceable features are valuable for event ticketing, training certificates, and competition access.

When combined with real-name verification, secondary transfer rules, and dynamic pricing, NFTs can maintain liquidity while deterring scalping and forgery.

Real-World Asset Digital Mapping (RWA Interface Layer)

Over the long term, NFTs can serve as digital proof for real-world equity—such as collectibles authentication, supply chain verification, or IP licensing records.

Growth in these areas is gradual, but once integrated with legal frameworks and audit processes, they tend to be more stable than sentiment-driven Assets.

VI. Technology Stack Evolution: The Key to Mainstream NFT Adoption

The bottleneck isn’t technology—it’s user experience. Over the next 3–5 years, the industry’s ceiling will be shaped by:

-

Account abstraction and seamless Signature, lowering Wallet barriers for new users.

-

Multi-chain and cross-chain messaging standards, reducing liquidity fragmentation.

-

Programmable Royalties and profit-sharing modules, making Creator incentives more predictable.

-

Data indexability and Real Time APIs, enabling application layers to iterate as rapidly as Web2.

-

Security and audit automation, reducing contract and phishing risks.

Whoever can hide “complexity” in the backend will be best positioned to bring NFTs from crypto-native to mainstream users.

VII. Regulation and Compliance: Core Variables for Industry Growth and Valuation

The long-term value of the NFT sector hinges on two uncertainties: regulatory interpretation and enforcement scope. Projects involving return promises, buyback mechanisms, or dividend distribution may trigger stricter compliance requirements.

Leading players will therefore invest in:

-

KYC/AML and source of funds verification.

-

Detection of market manipulation and wash trading.

-

Intellectual property and copyright traceability.

-

Consumer protection and standardized information disclosure.

For institutional capital, compliance isn’t a “nice-to-have”—it’s the price of entry. Reducing legal uncertainty means a lower capital discount rate and access to longer-term funding.

Early NFT models faced a fundamental conflict: users wanted low fees, Creators wanted ongoing Royalties, and platforms needed revenue. The future points to “multi-layered fees and configurable value distribution,” for example:

-

Lower Trading Fees, but increased charges for data services, issuance tools, and marketing.

-

Creator Royalties moving from “mandatory and uniform” to “conditional and community-negotiated.”

-

Users earning fee rebates or equity boosts through staking, tasks, or contributions.

-

Platforms charging B2B clients for APIs, settlement, custody, and Risk Control—reducing reliance on Trading Fees alone.

This marks a shift in NFT monetization from “buy-sell spreads” to “service value.”

IX. Three Possible Future Scenarios (2026–2030)

Scenario A: Moderate Growth (Most Likely)

The industry grows at a steady pace, with hotspots dispersed and ongoing platform and project consolidation.

Value is driven mainly by gaming, memberships, ticketing, and top IPs; volatility remains, but extreme bubbles are less frequent.

Scenario B: Infrastructure Breakthroughs Drive Expansion (Moderate Probability)

If Wallet usability, payment gateways, and compliance frameworks all improve, NFTs could experience another growth cycle—this time driven by “in-app assetization” rather than pure trading mania.

Growth would resemble a blend of SaaS and consumer internet models, not just capital speculation.

Scenario C: Regulatory Tightening and Liquidity Contraction (A Real Risk)

If major markets impose strict oversight on equity-related NFTs and macro liquidity remains tight, the industry could stagnate, with only a few high-certainty use cases surviving.

Still, as a technical standard, NFTs would continue to find use in enterprise and vertical applications.

X. Conclusion: NFTs Are No Longer a Single Track, But a Foundational Layer

The future of NFTs won’t be determined by whether they repeat past price surges, but by whether they become the “standard for digital rights expression.” As the industry shifts from storytelling to product delivery, and from chasing valuations to delivering equity, NFTs can finally mature.

-

For investors, the key question is: “Does this equity offer sustained demand and exit liquidity?”

-

For project teams: “Can you build verifiable, realizable, and sustainable user value?”

-

For platforms: “Can you connect issuance, circulation, settlement, and compliance with lower friction?”

The most accurate conclusion is this: NFTs aren’t disappearing, they’re being demystified; they’re not reverting to the past, but moving to the next stage.