TL;DR

-

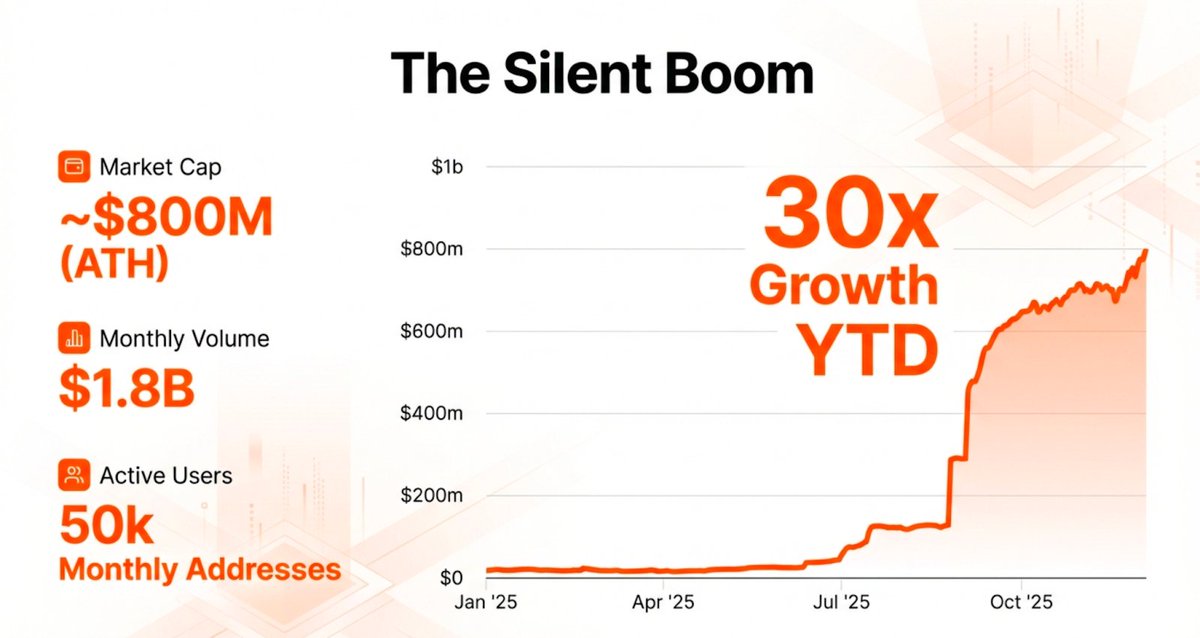

Tokenized stocks are the breakout sector of the current RWA cycle — the market has hit an $800M all-time high with 30x year-to-date growth and $1.8B in monthly trading volume

-

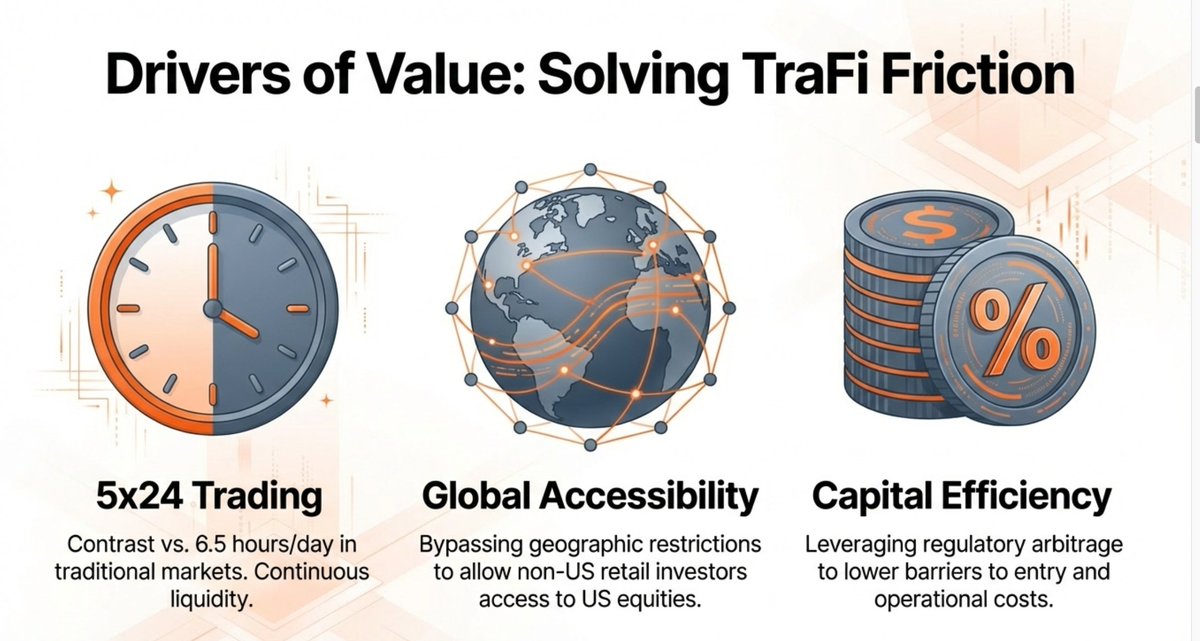

The core value proposition: 24/7 global access to US equities with near-instant settlement, bypassing the geographic restrictions and settlement delays of traditional brokerages

-

Tokenized stocks are the breakout sector of the current RWA cycle — the market has hit an $800M all-time high with 30x year-to-date growth and $1.8B in monthly trading volume

-

The core value proposition: 24/7 global access to US equities with near-instant settlement, bypassing the geographic restrictions and settlement delays of traditional brokerages

-

Three architectures are competing for dominance:

-

Instant Execution (@OndoFinance , CyberAlpha) — winning on capital efficiency

-

Inventory Model (@xStocksFi ,@BackedFi ) — leading on DeFi composability via debt structuring under Swiss law

-

Direct Ownership (@Securitize ) — strongest legal rights, but constrained by transfer restrictions and limited on-chain composabilityThe market is effectively a duopoly: Ondo at 53% share via liquidity engineering; Backed/xStocks at 23% via regulatory arbitrage

-

Technology is no longer the moat — regulation is. Assembling a cross-border license stack across the US, EU, and offshore jurisdictions is the hardest barrier to replicate

-

Platforms face a fundamental Trilemma: they can only optimize for two of three — liquidity/speed, regulatory safety/shareholder rights, or DeFi composability

-

The industry is splitting into two paths: Evolutionary (DTCC integration, incremental efficiency) vs. Revolutionary (direct on-chain issuance, full disintermediation)

-

Bottom line: the convergence of the $150 trillion global equity market with blockchain infrastructure is no longer a thesis — it's underway

1. The State of the Market: Analyzing the "Silent Boom"

The Real-World Asset (RWA) landscape is undergoing a structural transformation, with tokenized stocks emerging as the breakout sector of this cycle. While the broader RWA ecosystem has eclipsed an $800 million market capitalization—representing a staggering 30x Year-To-Date (YTD) growth in Dec 2025 —the integration of traditional equities into blockchain infrastructure marks a fundamental pivot in capital market design. This "Silent Boom" is not merely a migration of assets; it is the modernization of global liquidity, replacing fragmented legacy systems with a unified, programmable financial layer.

The sector’s momentum is quantified by Tier-1 metrics that signal a shift from experimental to institutional:

-

Market Cap Achievement: The sector recently reached an All-Time High (ATH) of approximately $800 million as of Dec 2025.

-

Liquidity Velocity: Monthly trading volumes have surged to $1.8 billion, demonstrating high secondary market activity.

-

Adoption Density: The network currently supports 50,000 monthly active addresses and 130,000 total holding addresses.

This trajectory is underpinned by the blockchain’s capacity to eliminate the settlement and accessibility frictions that have historically plagued traditional finance (TradFi).

2. Strategic Value Drivers: Solving Traditional Finance (TradFi) Friction

Traditional equity markets are shackled by legacy constraints: restricted trading hours, geographic silos, and high operational overhead. Tokenization serves as the strategic solution, providing a global, 24/7 liquidity layer that bypasses these bottlenecks. By re-engineering equities as digital tokens, issuers can tap into global capital pools while offering a trade execution experience superior to the T+1 legacy model.

The core value proposition is defined by the Efficiency Triple-Threat:

-

5x24 Trading: While traditional markets are limited to a 6.5-hour daily window, tokenized stocks enable continuous on-chain liquidity. This allows for real-time reactions to global events, eliminating the "opening bell" gap risk.

-

Global Accessibility: Tokenization effectively bypasses geographic restrictions, granting non-US retail investors seamless access to high-demand US equities that were previously cordoned off by brokerage barriers.

-

Capital Efficiency: By leveraging regulatory arbitrage and digital-first infrastructure, platforms lower operational costs and entry barriers, creating a more lean alternative to the traditional brokerage stack.

While the value drivers are clear, the technical implementation—particularly the bridging of liquidity—varies significantly across the three primary architectural frameworks.

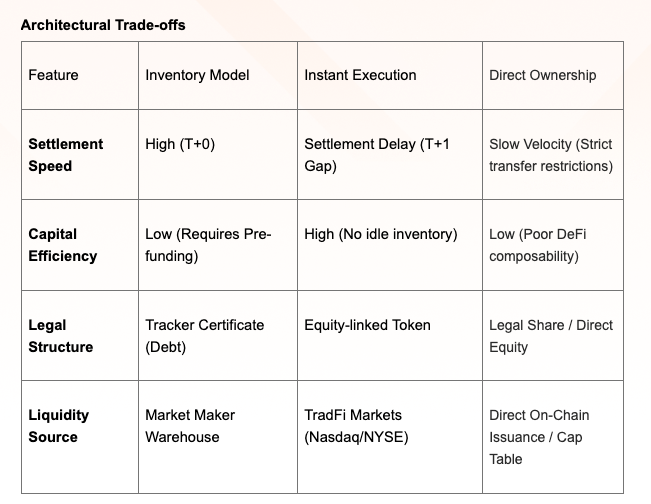

3. Comparative Analysis of Tokenization Architectures

The choice of product architecture is the single most important strategic decision for a platform, as it dictates scalability, DeFi composability, and the systemic risk profile.

The Three-Model Framework

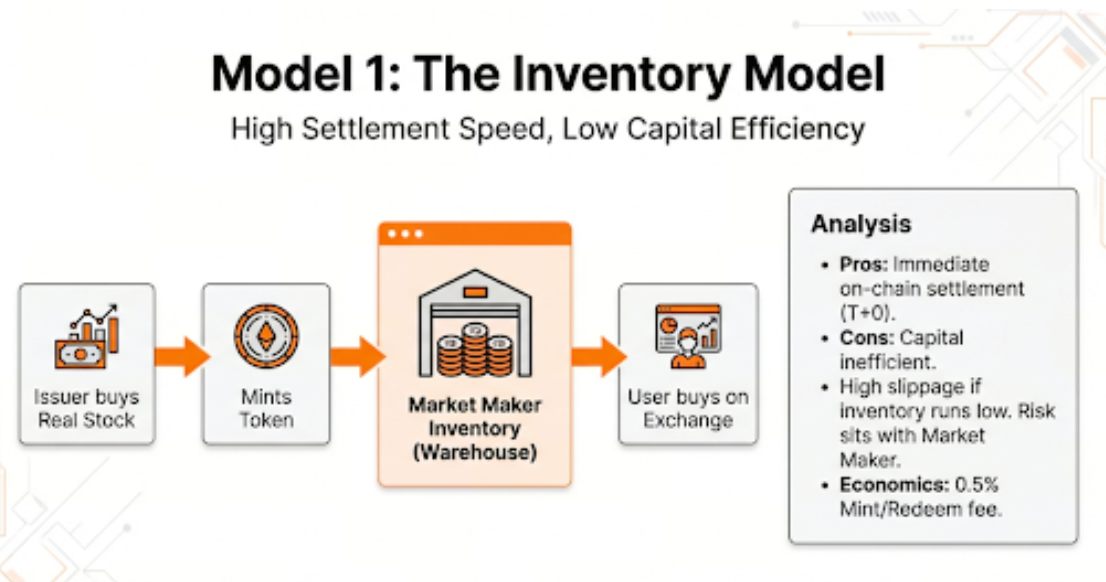

Inventory Model (e.g., xStocks, Backed): A "Pre-funded Liquidity" approach. The issuer or market maker purchases stock in advance and mints tokens held in a warehouse, ready for immediate sale.

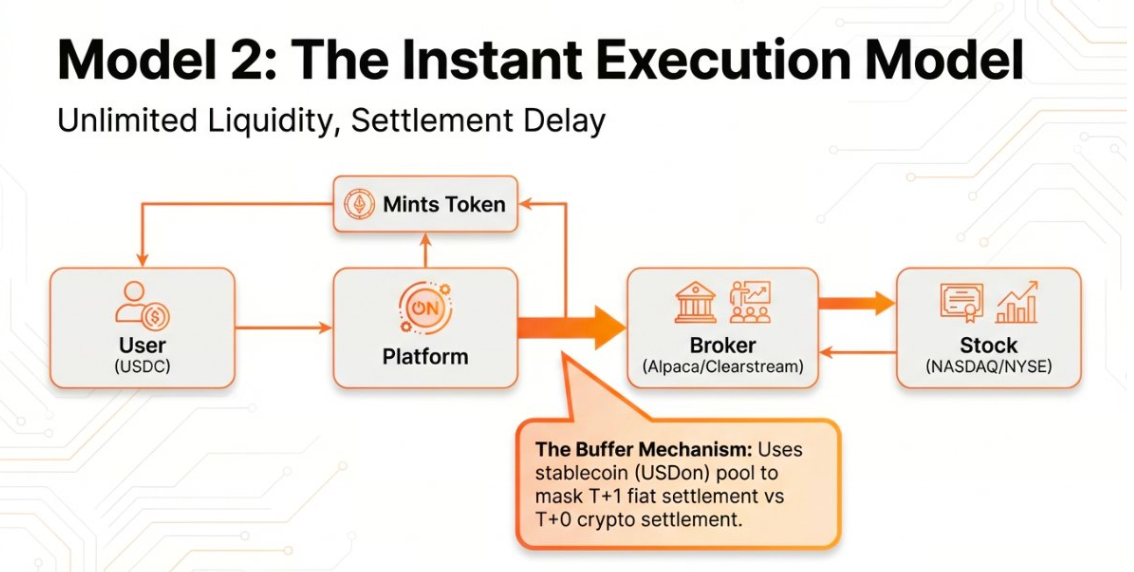

Instant Execution Model (e.g., Ondo, CyberAlpha): A "Just-in-Time Liquidity" approach. A stock purchase and token minting event are triggered only when a user places a confirmed order.

Direct Ownership Model (e.g., Securitize, Galaxy Digital): A "Purist" approach where the token is the legal share. Ownership is recorded directly on the company's capitalization table by a Transfer Agent. This provides investors with full shareholder rights, including voting and dividends, but involves strict transfer restrictions

As we move toward higher transaction volumes, the technical challenge shifts toward effectively bridging the gap between traditional and digital settlement cycles.

4. Competitive Landscape: Market Leaders and Challengers

Market dominance is currently a duopoly defined by liquidity moats and regulatory savvy.

Ondo Finance (53% Market Share): Ondo’s dominance is driven by its USDon Buffer. By converting USDC to USDon to mint stock tokens, Ondo controls redemption flow and mitigates "run on the bank" risks during T+1 gaps.

- Revenue Engine: Ondo generates an estimated 30M-40M in annualized revenue, derived from a ~0.1% trading spread and a 0.15% management fee on its RWA treasury products.

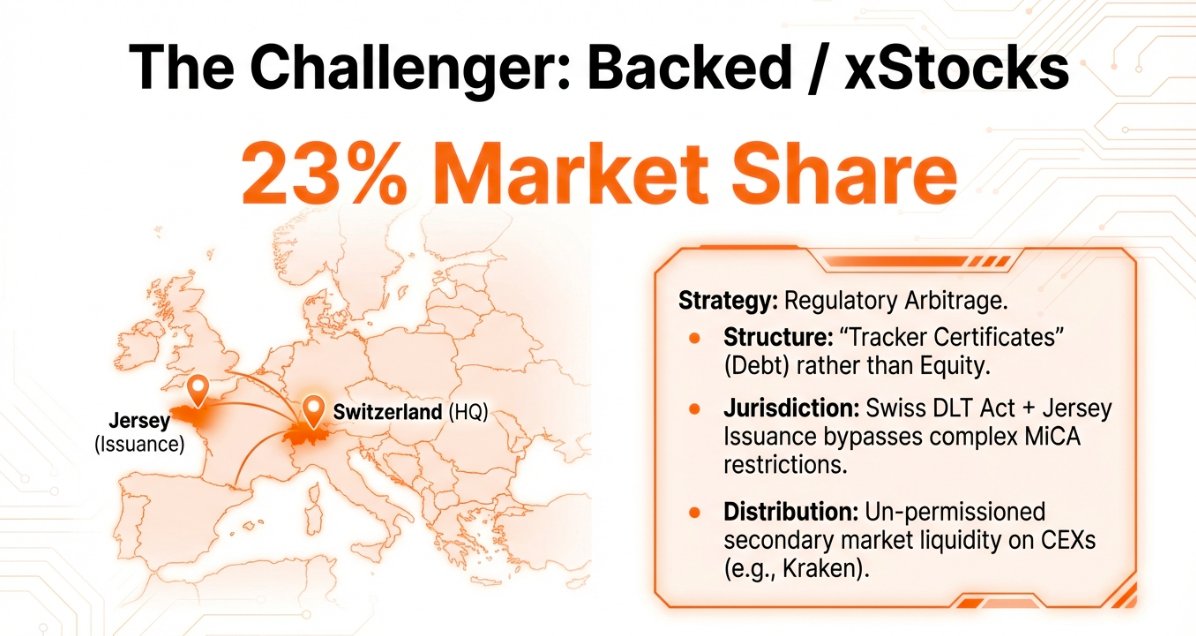

Backed / xStocks (23% Market Share): Their "Legal Alpha" is Regulatory Arbitrage. By structuring products as Tracker Certificates (Debt) under the Swiss DLT Act and Jersey-based issuance, they bypass MiCA restrictions and offer superior DeFi composability. Debt instruments avoid the transfer restrictions inherent in direct equity.

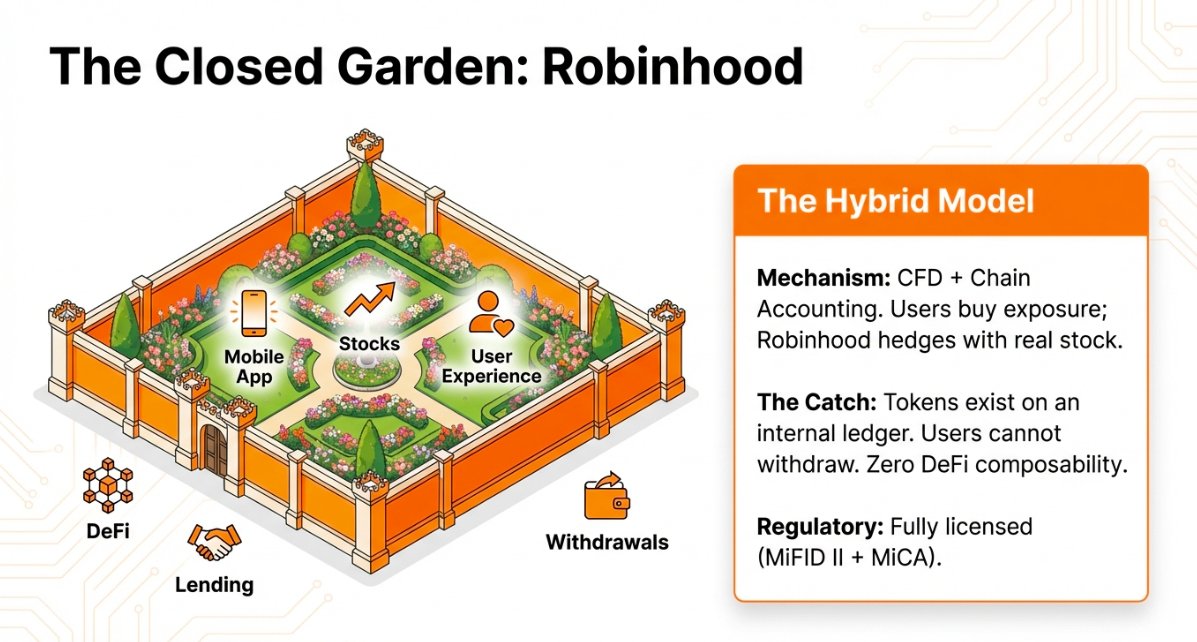

Robinhood (The Closed Garden): Currently operating on Arbitrum but signaling a move to a proprietary Robinhood chain. While fully licensed (MiFID II + MiCA), it lacks DeFi composability; tokens cannot be withdrawn, creating a high-trust but isolated ecosystem.

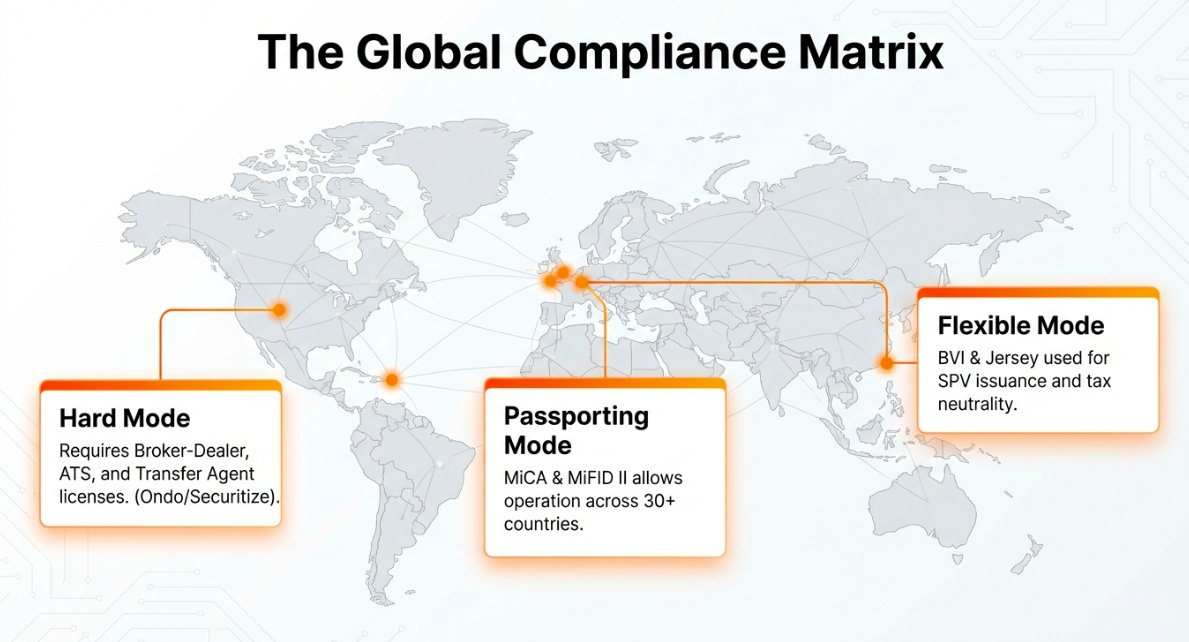

6. The Global Compliance Matrix and Regulatory Moats

In the RWA sector, "License Assembly"—the strategic collection of global permits—is a more formidable moat than the underlying technology.

-

Hard Mode (United States): Requires a trifecta of licenses: Broker-Dealer, Alternative Trading System (ATS), and Transfer Agent. Ondo secured this moat by partnering with/acquiring entities like Oasis Pro.

-

Passporting Mode (European Union): Under MiCA and MiFID II, firms can "passport" a single member-state license across 30+ countries.

-

Flexible Mode (Offshore): BVI and Jersey are utilized for SPV issuance to maintain tax neutrality and offshore flexibility.

The Ondo Regulatory Bridge: Ondo’s legal structure is a masterclass in fintech engineering: a BVI Issuer for offshore issuance, Oasis Pro as the US Broker-Dealer/ATS for asset access, and BX Digital (Swiss-based) acting as the validator for compliant passporting.

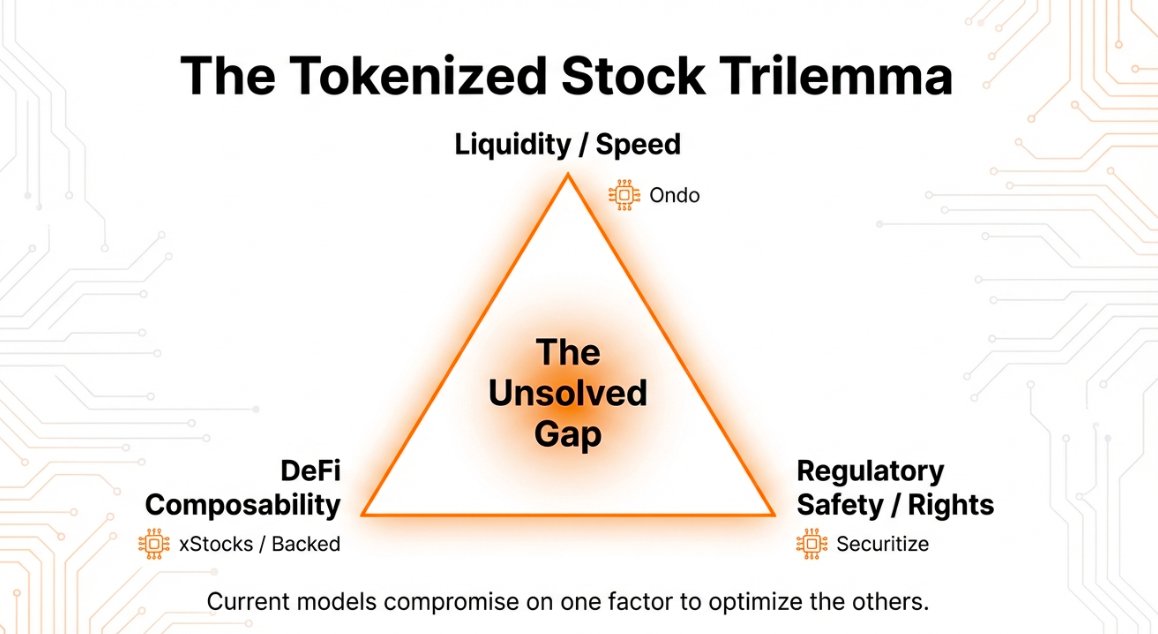

7. Strategic Outlook: The Tokenized Stock Trilemma

As the industry moves toward mass adoption, it must resolve the Tokenized Stock Trilemma, where platforms generally optimize for only two of the following:

-

Liquidity/Speed: (Ondo) Optimized via buffers and secondary market partners like 1inch.

-

Regulatory Safety/Rights: (Securitize) Optimized via direct ownership and SEC-compliant cap table integration.

-

DeFi Composability: (xStocks/Backed) Optimized by using Tracker Certificates (debt structure), which bypass the transfer restrictions of equity to allow for un-permissioned secondary trading.

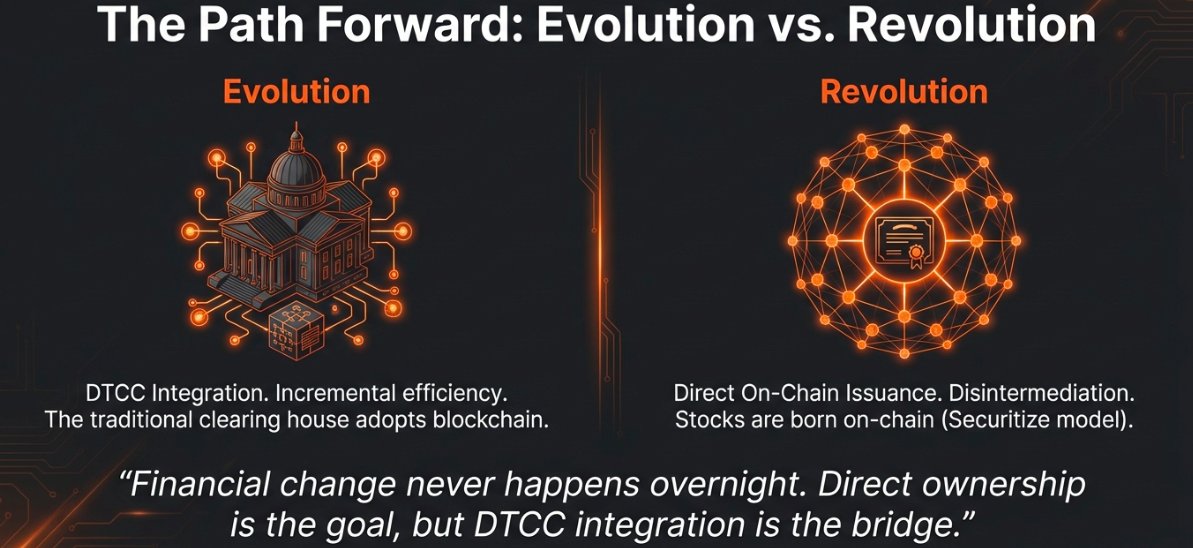

The market is diverging into two paths: the Evolutionary Path (DTCC integration/incremental efficiency for legacy players) and the Revolutionary Path (Direct on-chain issuance/total disintermediation).

"Financial change never happens overnight. Direct ownership is the goal, but DTCC integration is the bridge."

8. Summary and Critical Takeaways

The tokenized stock sector has graduated from proof-of-concept to aggressive market validation. The convergence of the $150 trillion global equity market with blockchain infrastructure is now an inevitability.

Critical Takeaways:

-

Institutional Maturity: The $800M market cap and 30x 2025 yearly growth signal that the sector is ready for institutional scale.

-

Model Supremacy: The "Instant Execution" model (Ondo/CyberAlpha) is currently the winning architecture due to its superior capital efficiency and lack of inventory bottlenecks.

-

The Regulatory Moat: Success is no longer about the "swapper" contract; it is about the License Assembly. The ability to bridge US asset access with EU and offshore distribution is the definitive barrier to entry.

About Foresight Ventures

Foresight Ventures

is a top-tier crypto venture firm and one of the

five most active investors

globally in 2024. With our team in US and Asia, we are the first and only crypto VC truly bridging East and West. Our approach is research-driven and founder-focused: we back the infrastructure powering next-gen global payments — from stablecoins and on/off-ramps to real-world assets, while amplifying our portfolio through a strong media network. Our 150+ investments include

Story, TON, Aptos, Morph, 0G Labs, Sentient AI, The Block, Foresight News, and many more.For more information, please visit: Website | Twitter | LinkedIn

For media requests, please contact media@foresightventures.com.

Disclaimer:

1. This article is reprinted from [ForesightVen]. All copyrights belong to the original author [ForesightVen]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

2. Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

3. Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.