Author: OKX

Introduction

Currently, the crypto market’s exploration of RWA mainly focuses on asset tokenization—mapping ownership of real-world assets like government bonds, stocks, or real estate onto the blockchain to achieve more efficient settlement and custody. However, this solution, centered on efficient holding and settlement, cannot fully meet the needs of the more active and larger trading volume in financial markets: namely, leveraged trading and risk management related to asset price volatility.

In fact, the true engine of liquidity in global financial markets is not static asset holders but traders seeking leveraged directional exposure. From the US monthly-end nominal value options market of about $50 trillion to the non-US CFD (Contract for Difference) markets with approximately $30 trillion in monthly trading volume, retail investors’ demand for high leverage and short-term risk exposure has never waned. Despite the enormous trading scale, existing traditional financial tools still struggle to fully support this demand: 0DTE options (zero days to expiration) force traders into nonlinear risks involving Theta (time decay) and Vega (volatility), while CFD markets are often criticized for their opaque black-box mechanisms and centralized counterparty risks.

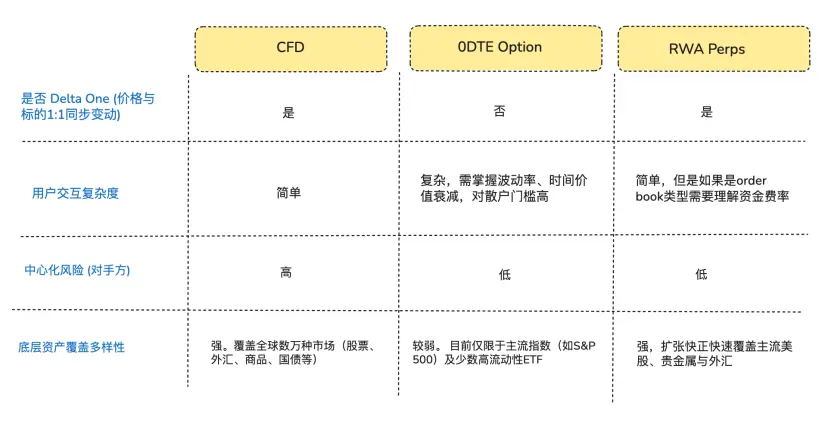

From the perspective of traders purely seeking directional exposure, what many truly desire is not “options” or “tokenized stocks,” but a pure Delta One (linear/symmetric payoff) exposure—that is, asset price movements that can be simply and directly converted into profit or loss in proportion, without any loss or deviation (Arthur Hayes wrote a comprehensive review titled “Adapt or Die” late last year about their development of perpetual contracts—interested readers can check it out).**

It is within this structural mismatch that DeFi protocols have keenly identified a market opportunity. Some DeFi entrepreneurs are attempting to introduce perpetual contracts, which have been validated and matured in the crypto market for nearly a decade, into traditional asset domains. These products use synthetic derivatives architectures, anchored by oracle price feeds and funding rate mechanisms, to provide around-the-clock leverage trading on stocks, commodities, and forex without the need for actual custody or delivery of the underlying assets.

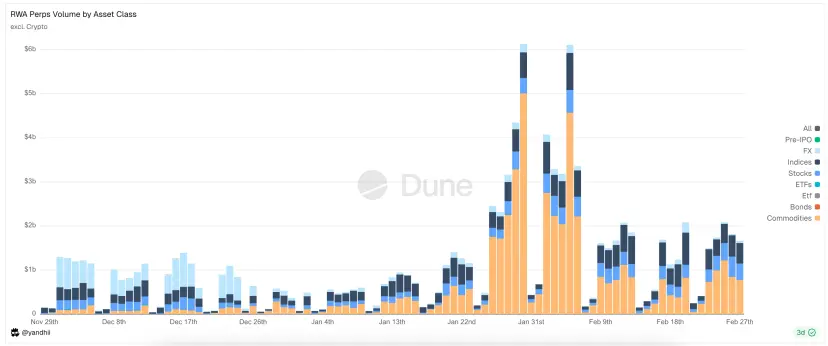

Figure: Main asset types traded on RWA Perps Dex currently

1. Market Background (Opportunities for Entering the RWA Perps Market)

1.1 Entry Point 1: US 0DTE Options Market

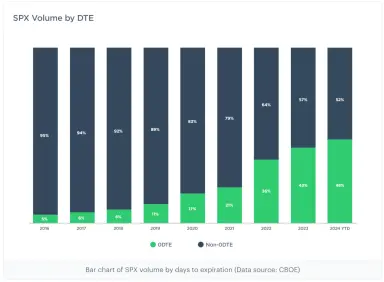

Over the past decade, the US options market has undergone profound structural changes. According to data from Cboe Global Markets, the proportion of end-of-day options (0DTE) trading volume in the S&P 500 index options has surged from less than 5% in 2016 to over 60% today, with a monthly nominal trading volume of $48 trillion (about 40 times the monthly trading volume of perpetual contracts on centralized exchanges). This data reflects not only increased trading frequency but also reveals a large capital force seeking extremely high intraday leverage exposure.

Note: 0DTE stands for “Zero Days to Expiration,” referring to options that expire on the same day. These options expire at market close and are used for ultra-short-term speculation to achieve quick returns and avoid overnight risk.

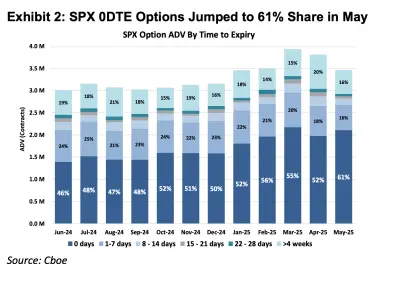

Figure: The above two charts show the proportion of S&P 500 index options with different expiration times from 2016 to 2025. It’s clear that 0DTE options accounted for less than 5% in 2016, but by 2025, their market share has skyrocketed to 61%, indicating nearly half of S&P 500 options trading is now focused on same-day directional bets for ultra-short-term gains.

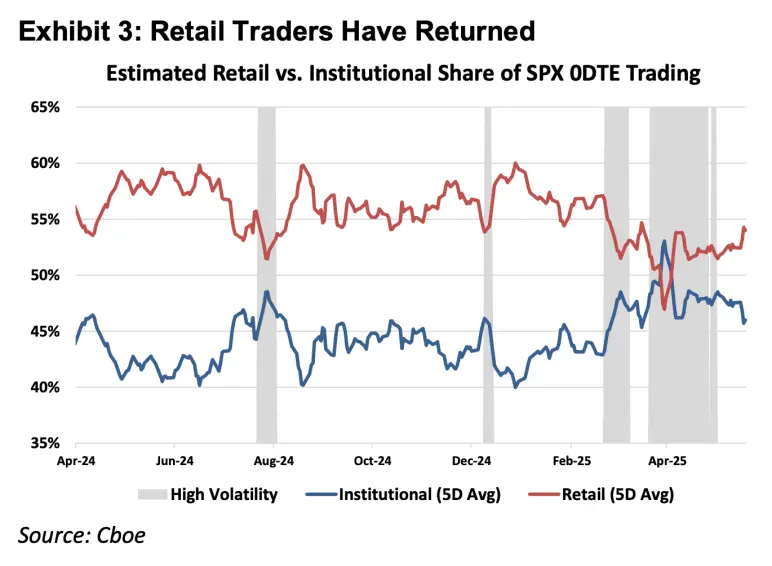

Figure: The above chart shows retail traders are the dominant force in the 0DTE market.

From the first principles of financial instruments, derivatives can be divided into Delta One products and nonlinear products. Traditional Delta One tools like stocks and futures have symmetric risk exposure: gains when the underlying price rises and losses when it falls, proportional and linear. Conversely, options are designed to manage asymmetric risks.

For example, a fund manager holding a large position in Apple stock, optimistic about the company’s long-term fundamentals but worried about short-term earnings volatility causing a sharp decline, can buy put options as insurance. In this structure, his upside potential remains intact as the stock rises (symmetric upside), but his downside is capped at the premium paid (asymmetric downside risk).

This “separation of rights and obligations” for insurance purposes means that options’ cost structure must reflect not only the intrinsic value (Delta) but also the potential volatility (Gamma) and time decay (Theta).

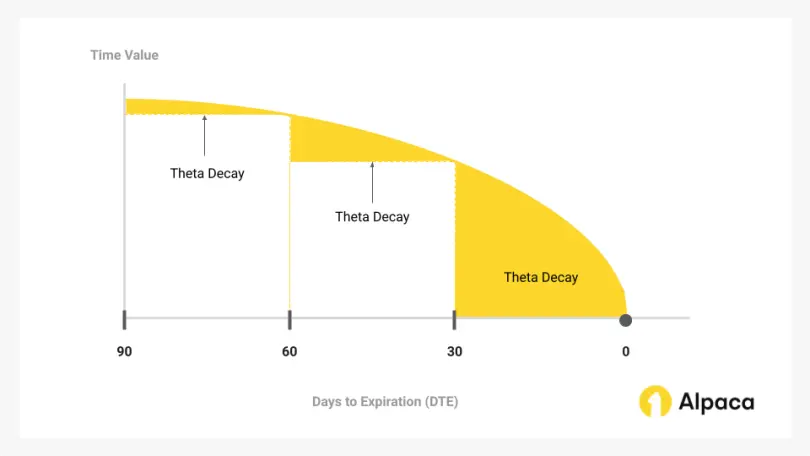

The recent growth of the 0DTE market reveals a paradox: many traders are not using options to hedge asymmetric risks or trade volatility, but rather as a sole means to access intraday leveraged directional bets. As a result, traders are forced to pay high costs for “insurance” they don’t need—time decay (Theta). As long as the underlying’s upward speed doesn’t outpace the decay of Theta, even correct directional bets can result in losses.

Figure: Time value, which shrinks as time passes, is the core of 0DTE options trading.

Therefore, as a Delta One product, perpetual contracts strip away extraneous time and volatility costs, offering a purely linear leverage exposure that mathematically can more precisely match the speculative needs of this capital segment than 0DTE options.

1.2 Entry Point 2: Non-US CFD Markets

Outside the US, retail leverage demand is mainly met by CFDs, with a projected monthly trading volume of $30 trillion in 2025.

While CFDs provide a linear Delta One payoff structure, their operation relies on broker models, which have significant transparency issues. Most CFD brokers operate on a B-Book (internal market-making) basis, meaning the broker acts as the counterparty to clients’ trades (some reputable brokers hedge their profitable clients to avoid risk, but the top 20% of the market is dominated by many small brokers relying on client losses). In this zero-sum, opaque environment, brokers have the technical and economic ability to modify quotes, slippage, and execution speed.

Compared to CFDs, RWA Perps can be viewed as a “transparent CFD based on smart contracts.” By bringing on-chain liquidation logic, funding rate calculations, and oracle prices, DeFi protocols eliminate the possibility of centralized broker intervention. Additionally, atomic settlement with stablecoins enhances capital efficiency to seconds, enabling true self-custody and real-time clearing.

2. Challenges in Building RWA Perps Products

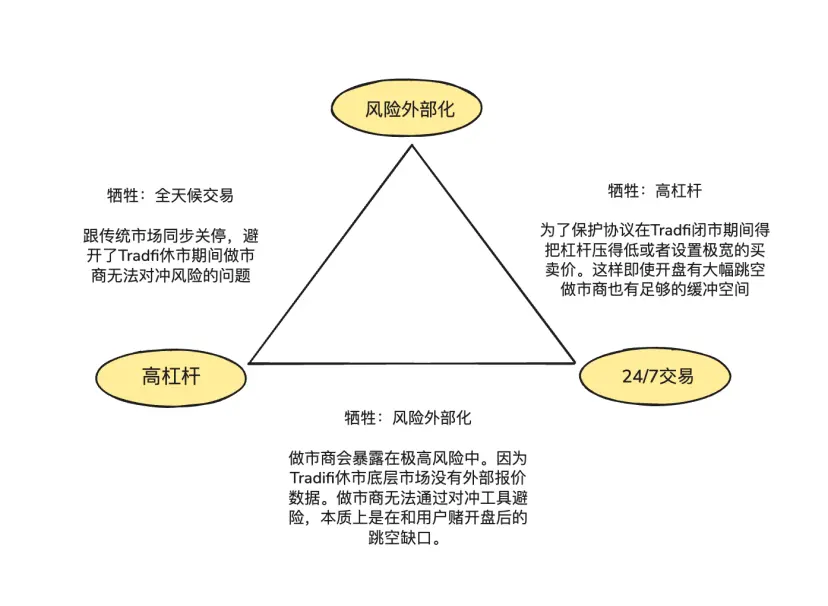

RWA Perps are not just simple replicas of crypto-native perpetuals. While crypto assets trade 24/7 with real-time pricing and T+0 on-chain settlement, traditional assets are constrained by physical world legal frameworks, holidays, and outdated banking clearing protocols.

This asynchronous nature creates an “impossible triangle” in product design:

- High Leverage: To meet retail traders’ demand for high multiples.

- 24/7 Availability: To maintain DeFi’s core value of anytime, anywhere trading.

- Risk Externalization: To ensure the protocol and market makers do not bear directional risk, enabling long-term system sustainability.

2.1 How is the on-chain price anchored when US markets are closed?

Perps are essentially “price discovery mirrors,” requiring continuous external spot price feeds. When Nasdaq or CME are closed on weekends or at night, oracle data sources break.

This creates two core risks during US market closures:

Risk 1: Lack of hedging channels for market makers during weekends

Market makers provide tight spreads and deep liquidity by taking neutral positions rather than directional bets. They hedge their risk by immediately buying or selling equivalent assets in traditional spot or futures markets when selling contracts to traders.

When traditional markets are closed, hedging channels are unavailable. Market makers can only cancel orders or add large risk premiums to quotes, leading to widened spreads—sometimes expanding 10-20x—causing liquidity to dry up.

Risk 2: Gap risk at Monday open

Crypto assets trade 24/7, with continuous price curves and sufficient time for liquidation engines to close positions during downturns. In RWA Perps, however, accumulated price pressures during market closure can cause sudden gaps at Monday open. Large jumps can create “price vacuum” zones where liquidation engines cannot find counterparties before positions are wiped out.

Current solutions include:

- Internal simulated pricing (e.g., TradeXYZ / Hyperliquid): Using EMA algorithms to gradually drift prices during oracle disconnection, maintaining 24/7 coverage but still susceptible to manipulation.

- Forced risk reduction (e.g., Ostium): Introducing 0DTE-like features—requiring high-leverage positions to be automatically closed or reduced before market close. Only low-leverage positions with sufficient margin buffers are allowed overnight. This sacrifices some “perpetual” nature but ensures safety against Monday gaps, preventing systemic bad debt.

2.2 How to provide TradFi-level trading depth on-chain at low cost?

Liquidity provision and order execution mechanisms are key to capital efficiency, risk distribution, and user experience. The two main approaches are: CLOB (Central Limit Order Book) and Oracle-based Pools.

Hyperliquid demonstrated success with order book models for crypto-native assets, leveraging zero-friction risk hedging via stablecoins transferred across platforms in milliseconds. Market makers can hedge risk on centralized exchanges instantly, keeping spreads tight and attracting volume.

In RWA, cross-border hedging friction is significant: on-chain USDC (T+0) and traditional fiat settlement are mismatched in time, forcing market makers to hold large dollar reserves in traditional accounts. Additionally, bank holidays and weekends prevent timely hedging during market stress.

This is why Ostium’s founder Kaledora advocates for a pool-based model rather than an order book—believing that native crypto assets’ frictionless hedging is hard to realize in RWA Perps. When a market maker receives an NVDA order in RWA Perps, they cannot hedge instantly via stablecoins across traditional channels due to banking constraints.

2.3 How does the system prevent bankruptcy when traders profit continuously in one-sided trends?

The third challenge involves how protocols hedge externally to ensure long-term solvency. GMX’s pool model persists because it acts as a “passive market maker,” statistically absorbing high-leverage positions’ losses and liquidations during volatile periods. This works well in crypto markets with frequent reversals.

However, RWA assets often experience prolonged bullish or bearish trends lasting years (e.g., S&P 500). Without risk externalization (hedging), continuous trader profits would drain the liquidity pool, leading to systemic insolvency.

3. Project Archetypes and Mechanism Battles: Oracle Pricing + Pool vs. Order Book

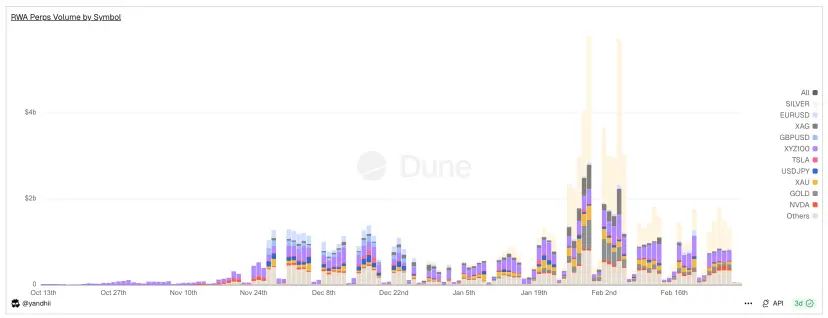

Figure: Daily trading volume of RWA Perps Dex shows significant volume drop during weekends.

The core contradiction in RWA Perps revolves around the “time gap”: despite over $200 billion traded in 30 days across platforms, weekend volumes plummet 70-90%. This indicates that liquidity still heavily depends on traditional market hours.

Two divergent architecture paradigms have emerged:

- Ostium’s Active Hedge Pool (AHP) model

- Hyperliquid’s internal pricing order book (Trade.xyz)

3.1 Early RWA Perps Projects: Synthetix and Gains Network

Before Ostium and Hyperliquid’s complex hedging or order book reconstructions, DeFi had experimented with “synthetic assets.” Synthetix and Gains Network validated the concept of on-chain RWA Perps, demonstrating strong demand but also exposing the limitations of first-generation mechanisms.

Synthetix: Global Debt Pool Model

Synthetix was among the earliest to attempt bringing real-world asset prices on-chain. Between 2020-2021, it launched synthetic stocks like sAAPL, sTSLA, trying to mirror US equities.

As a “pool counterparty” model (where all SNX stakers are counterparties), Synthetix created a no-order-book, infinitely liquid exchange: all synthetic assets are exchanged at oracle prices, eliminating the need for matching counterparties. This addressed early liquidity cold-start issues, especially with liquidity mining incentives.

By 2021, Synthetix removed most RWA assets due to lack of active hedging—when US market assets like sTSLA are closed, prices can’t be updated, risking attacks.

Overall, Synthetix pioneered the derivative collateral pool model for on-chain RWA assets, with no order book and oracle prices. Its influence persists, but by around 2022, it largely exited the RWA Perps market.

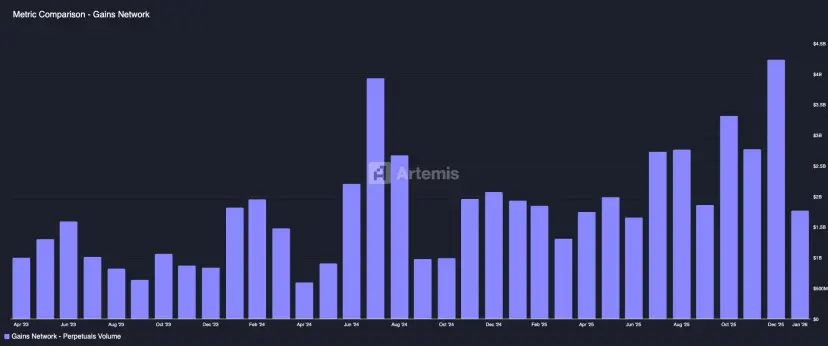

Gains Network (gTrade): Oracle-driven Market Maker Pool

Gains is another early project exploring on-chain synthetic leverage trading for crypto, forex, and US stocks. It uses independent asset pools as counterparties: users deposit USDC, DAI, ETH to open leveraged positions, with profits and losses managed by the gToken Vault.

- Liquidity Model & Market Making Dynamics:

- Single-sided vault: Gains’ liquidity pools mainly hold stablecoins like USDC/DAI.

- GNS token: acts as risk buffer and incentive. To prevent extreme losses, the protocol introduces GNS as a last line of defense—when pools are profitable, it buys back and burns GNS to reduce inflation; when pools are in deficit, it mints GNS and sells off-chain to top up liquidity.

Pricing relies on Chainlink feeds with fixed spreads, with fee sharing among LPs and GNS stakers. Risk controls include price impact fees (extra charges for large orders), and position limits to enforce stop-loss or forced liquidation.

Gains offers high leverage and multi-market coverage, serving as a decentralized alternative to centralized exchanges. It demonstrates that “oracle + liquidity pool” models can support large-scale trading under proper risk controls, but also reveal challenges like concentrated risk and lack of hedging mechanisms, informing future innovations.

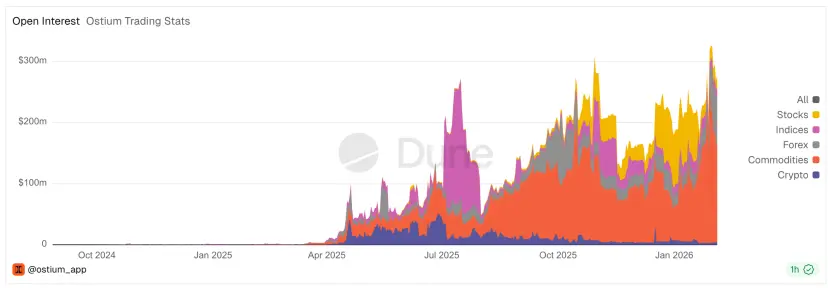

3.2 Ostium: Breaking Pool Model Limits, Building On-Chain CFD Brokerage

Ostium, a rising RWA Perp DEX, launched on Arbitrum in August 2025. It still adopts a pool-based core but incorporates insights from GMX, Gains, and others to address the “trader profit = LP loss” zero-sum dilemma, which limits market growth.

They design a hybrid A-Book (hedging) and B-Book (internal risk absorption) system on-chain to mitigate this conflict.

Liquidity & Market Making Architecture

- Two-layer liquidity model:

- Level 1: Liquidity Buffer—the protocol’s “moat,” accumulated from revenues, covering trader profits and losses. Similar to Gains’ market maker cushion.

- Level 2: Market Maker Vault (OLP Vault)—funded by LPs, only engaged when the buffer is exhausted.

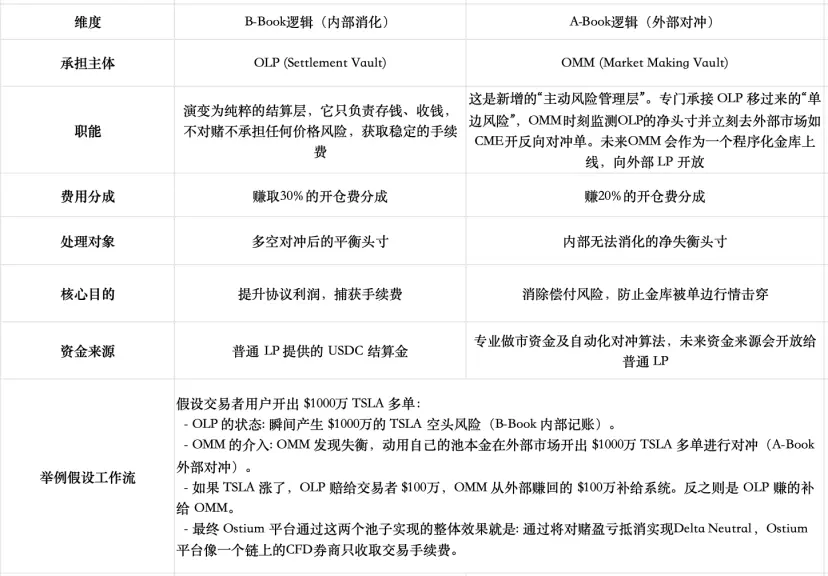

Key innovation: Separating “settlement” from “market making”

Ostium recognizes that simple two-layer buffers can’t handle long-term directional imbalances (data shows buffers are quickly depleted). To address this, they separate the functions:

- Settlement (closing positions, risk management)

- Market making (providing liquidity)

This involves integrating on-chain hedge vaults similar to traditional broker models, aiming for a system where high trading volume can be supported without LP long-term risk exposure.

@E14@

The hedge vaults are not yet live, but when scaled, they require professional market-making with millisecond cross-market hedging, real-time delta monitoring, and dynamic risk controls—challenging but essential.

Market close risk controls

Ostium aligns closely with US stock trading hours, using oracle timestamps to execute only during market hours, avoiding price vacuum risks. Before market close, the system forcibly closes high-leverage positions exceeding thresholds, reducing maximum leverage from 100x to safer levels.

Why doesn’t GMX adopt similar designs?

GMX maintains a pool model without separation, believing that the trade-offs are too high and that internal mechanisms (adaptive funding, price impact, long/short pools) balance risks sufficiently. Introducing external hedge vaults would sacrifice yield and increase centralization. Also, GMX’s pools cover all traders’ combined exposure, which statistically tends toward negative expectation in volatile crypto markets, whereas Ostium targets traditional, less volatile RWA markets.

Why choose pool models over order books?

Kaledora, Ostium’s founder, argues that the traditional pool model’s limitations—LP bearing unidirectional risk and size constraints—are addressed by her hybrid approach. She advocates for integrating A-Book and B-Book risk transfer to unlock unlimited trading volume, similar to top CFD brokers.

She also believes that order books, while effective for crypto-native assets, are resource-wasteful in RWA markets where prices are already efficiently discovered on top exchanges like Nasdaq and CME. Rebuilding on-chain order books would force competition with trillion-dollar giants, making it less attractive than leveraging global price references.

In summary:

- The core contradiction in RWA Perps is the “time gap” caused by market closures.

- Architectures include active hedge pools and internal order books.

- Early projects like Synthetix and Gains validated on-chain RWA exposure but faced efficiency and risk limits.

- Ostium aims to overcome these by hybrid models, integrating traditional broker-like risk management on-chain.

- The future of RWA Perps depends on balancing liquidity, risk, and market hours, with innovative architectures that can support large-scale, long-term trading.