MicroStrategy's holdings surpass 700,000 BTC! The circular financing model hides credit disaster risks

MicroStrategy purchased 22,305 BTC, bringing the total holdings to 709,715 BTC (accounting for 3.55% of circulating supply), with an unrealized gain of $10.5 billion. The funds come from preferred stocks STRC (11%), STRK (8%), STRF (10%). BlackRock holds $470 million worth of MicroStrategy preferred stock. Experts warn of cycle dependency risks, but analysts see this as an innovative model.

MicroStrategy’s 70 Million BTC Milestone Behind the Financing Machine

Between January 12 and January 19, MicroStrategy made an additional purchase of 22,305 bitcoins at approximately $2.13 billion, continuing its aggressive accumulation, now absorbing 3.38% of the total supply of this top-tier cryptocurrency. This is equivalent to 3.55% of the circulating supply of 19.97 million coins. According to the 8-K filing submitted to the U.S. Securities and Exchange Commission (SEC) on January 20, the average purchase price was $95,284 per bitcoin.

This latest acquisition brings MicroStrategy’s total bitcoin holdings to 709,715, valued at about $64 billion. The company’s total cost basis for these bitcoins is approximately $53.92 billion, with an average cost of $75,979 per bitcoin. Based on current prices, the unrealized profit is about $10.5 billion. The funds for these recent purchases were raised from the company’s sale of Class A common stock (MSTR), perpetual deferred preferred stock (STRC), and Series A perpetual execution preferred stock (STRK).

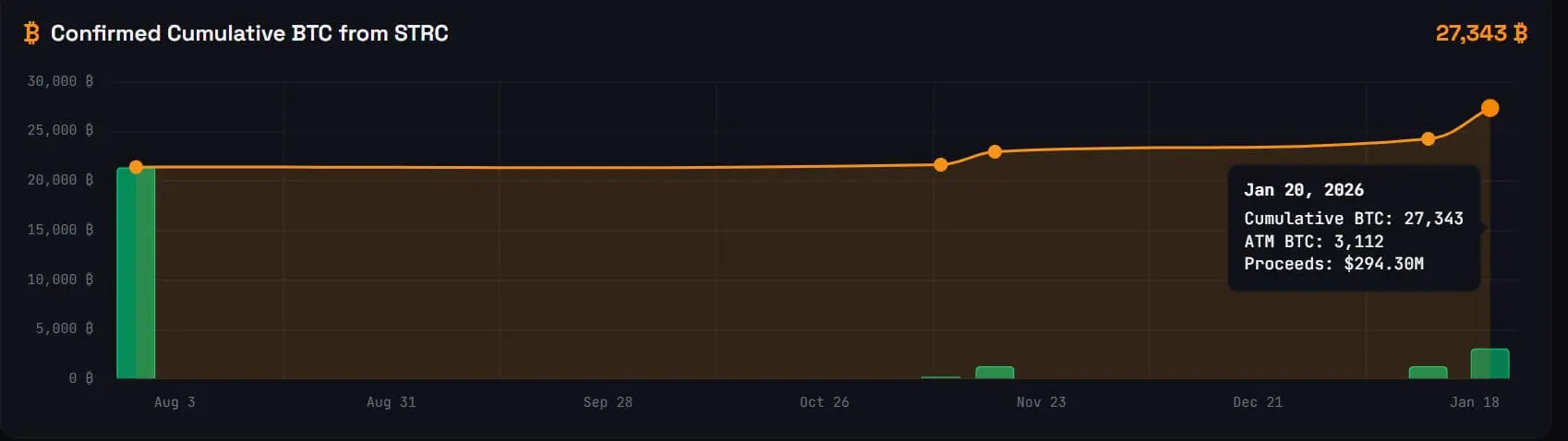

According to SEC filings, led by Michael Saylor, MicroStrategy sold 10,399,650 shares of MSTR stock last week, raising about $1.8 billion. The company still holds stocks worth approximately $8.4 billion, which can be used for future bitcoin purchases. However, activity in the preferred channels is increasing. The filings show that Strategy sold 2,945,371 shares of STRC, realizing a profit of about $294.3 million (remaining 36 million shares); sold 38,796 shares of STRK, with a profit of $3.4 million (remaining 2.03 billion shares).

This increased investment indicates that the company is attempting to transform its bitcoin treasury strategy into a reusable “yield SKU,” allowing it to quietly exist within brokerage accounts and income investment portfolios. This approach is attracting significant interest.

Four-Tier Preferred Stock Structure Creates a Bitcoin Yield Empire

This financial engineering has spawned four different tiers of bitcoin investment, traded on the NASDAQ. This means investors can participate without any specialized knowledge of bitcoin—they only need a regular brokerage account. The product line is divided according to risk tolerance, offering four different MicroStrategy trading options.

The highlight of this issuance is the floating-rate Series A perpetual deferred preferred stock (STRC). This security explicitly markets itself as “short-term high-yield credit,” currently paying an 11.00% annual dividend in cash. Unlike standard bonds whose yields are market-driven, STRC is a bond product managed by the issuer. The issuer retains the policy authority to adjust the dividend rate to ensure the stock trades close to its $100 face value. Data from STRC.live shows that the company has raised approximately 27,000 bitcoins through STRC funding activities.

MicroStrategy Preferred Stock Tiered Structure

STRC (Most Aggressive): 11% floating dividend, issuer can adjust rate, raised funds to buy 27,000 BTC

STRK (Hybrid): 8% dividend, convertible to stock, potential ~40% gains if MSTR rises

STRF (Conservative): 10% cumulative dividend, non-convertible but senior in capital structure, remaining capacity $1.6 billion

STRD (Highest Risk): 10% non-cumulative dividend, non-recourse, remaining capacity $1.4 billion

Additionally, MicroStrategy has even entered the European market. Last November, it launched Series A perpetual preferred stock (STRE), a euro-denominated security with a 10% annual dividend paid quarterly. The terms include strict penalties for unpaid dividends: dividends are cumulative, and missing a payment period increases the dividend by 100 basis points, up to a maximum of 18%.

BlackRock’s $470 Million Validation of Yield Strategy

The list of Strategy’s financial engineering products has successfully attracted a demographic usually dismissive of cryptocurrencies: income tourists. Data from filings by multiple institutions shows that high-yield and preferred stock funds dominate the STRC holder list, including Fidelity Capital Gains Fund (FAGIX), Fidelity Advisor Floating Rate High Income Fund (FFRAX), and Virtus InfraCap US Preferred Stock ETF (PFFA).

Meanwhile, the most notable validation comes from BlackRock. The BlackRock iShares Preferred Stock and Income Securities ETF (PFF) is a large fund with net assets of $14.25 billion. In its conservative investment portfolio, MicroStrategy’s bitcoin-linked bonds occupy a significant position. The ETF disclosed holdings of about $210 million in STRC, along with approximately $260 million in STRF, STRK, and STRD. BlackRock’s total holdings of MicroStrategy preferred stock through this ETF amount to about $470 million (3.3% of the fund’s total assets).

Valentin Kosanovic, Vice President at Capital B, sees this as a watershed moment for digital credit. “This is another clear, objective, irrefutable example demonstrating the realization of the institutionalized wave of traditional bitcoin-linked financial products.” BlackRock’s involvement, as a traditional financial giant, lends significant legitimacy to MicroStrategy’s model.

Controversies and Risks of the Cycle Financing Model

The mechanisms required to sustain these dividends introduce a series of unique risks. MicroStrategy does not pay these yields from operational profits but instead finances them through capital markets. The company’s offering documents for STRC indicate that cash dividends are expected to be primarily funded through additional fundraising, including issuing new stock on the market.

This creates a cycle dependency: MicroStrategy raises funds by selling securities to buy bitcoin, then pays dividends on these securities. RSM US partner Michael Fanelli emphasizes several risks inherent in this model, including sharp declines in bitcoin prices, lack of insurance coverage, and untested performance of such products during economic downturns. He also notes that perpetual products have no maturity date, meaning the company theoretically needs to pay dividends indefinitely unless it conducts buybacks or restructures.

However, bitcoin analyst Adam Levenstein counters that these products are almost “incomprehensible” to traditional analysts. He states: “STRC is quietly turning MicroStrategy into a private central bank serving a yield-hungry world.” He explains: “STRC is a yield-bearing ‘credit track’ that absorbs fixed-income demand, converts it at scale into bitcoin, and then uses the resulting equity premium for the next round of financing, making funding easier, cheaper, and faster. It’s a flywheel with an internal bidding mechanism.”

This controversy reflects the cognitive gap between traditional finance and crypto innovation. Traditional analysts see cycle dependency as fragile from a risk management perspective, while crypto supporters see it as an innovative flywheel breaking through traditional financing limits.

Related Articles

Strategy Raises STRC Dividend to 11.5% as MSTR Logs Eighth Straight Monthly Decline

Michael Saylor Signals New Bitcoin Buy Amid Market Weakness

Data: If BTC breaks through $69,504, the total liquidation strength of mainstream CEX short positions will reach $1.251 billion.