"Trillions" of liquidity released: Can pre-IPO equity tokenization reshape PE/VC exit models? — The evolution from Perps to TaaS

Author: Owen Chen from Peking University Blockchain Association (X @xizhe_chan)

Summary

Pre-IPO Stock in private companies accounts for trillions of dollars in global asset allocation, but has long been constrained by two structural dilemmas: high entry barriers for participants and scarce liquidity exit options. As on-chain real-world assets (RWA) become a focus of financial innovation, “equity tokenization” is seen as a key mechanism to break the liquidity deadlock in private markets. This report focuses on the underlying equity tokenization of non-listed companies (especially unicorns), aiming to clarify the evolution from early speculation to compliant infrastructure by analyzing market status, implementation pathways, and key challenges. The core conclusions are as follows:

1. Market Status: Despite the valuation of global unicorns reaching trillions of dollars, the actual on-chain tokenization market size is only in the range of $10–20 million (excluding some non-free-float projects, the freely tradable amount is only in the tens of millions). The market shows a strong top-heavy effect, with assets highly concentrated in a few AI tech unicorns like OpenAI and SpaceX. This indicates the industry is still in the very early stage of transitioning from “narrative space” to “effective market,” with no large-scale asset supply and acceptance yet formed.

2. Path Differentiation: The industry has formed three distinct pathways, mainly differing in “degree of rights confirmation” and “company participation”:

- Synthetic Asset (Republic, Ventuals): Includes perpetuals and debt notes, without holding underlying equity, only providing valuation exposure. They use high leverage for speculative needs and mainly serve as traffic entry points.

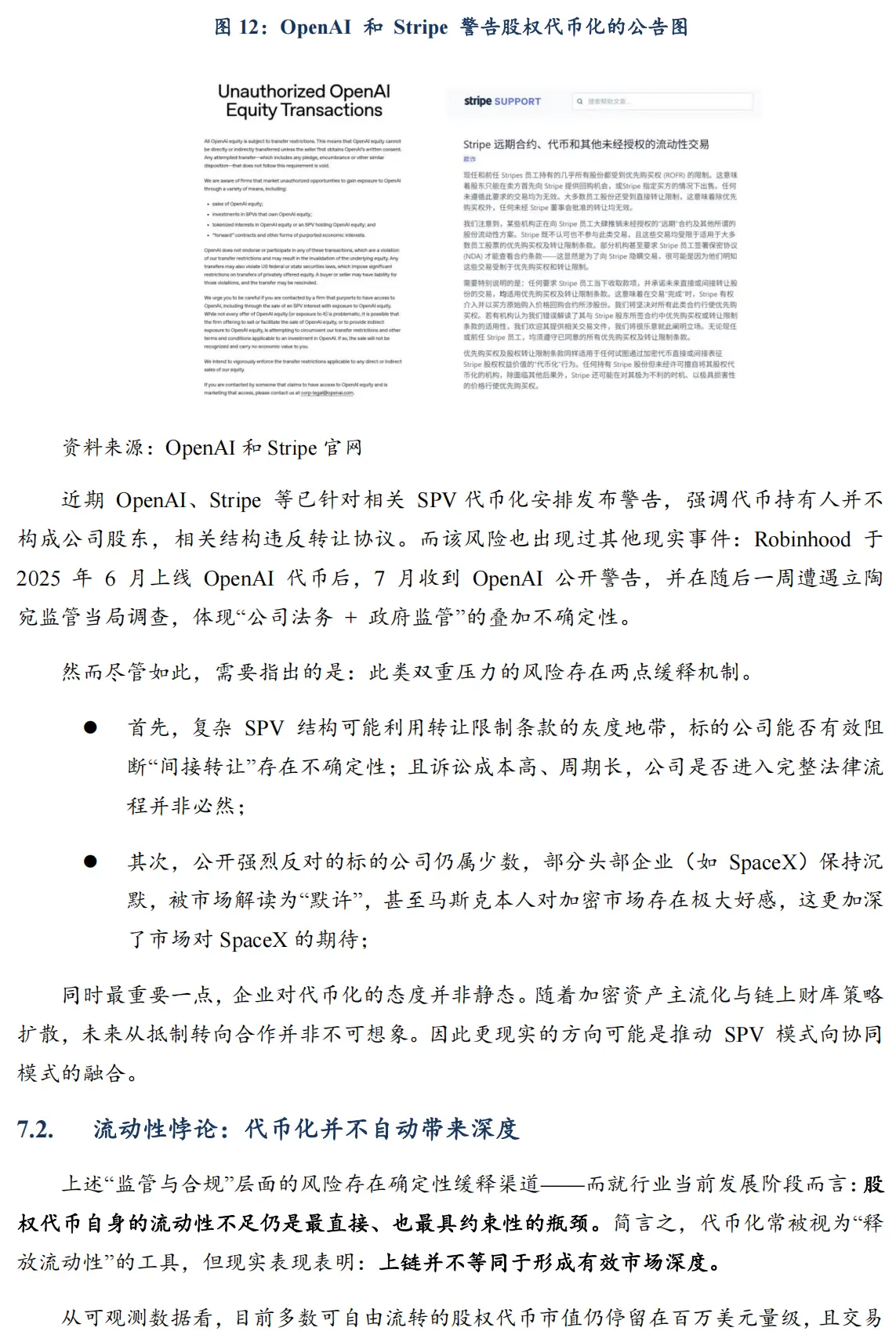

- Indirect Holding via SPV (Jarsy, PreStocks, Paimon): Uses offshore SPVs to hold shares and tokenize rights, representing the most mainstream on-ground form. However, they face dual compliance risks from target companies and regulators, with recent warnings from companies like OpenAI exposing legal vulnerabilities related to “transfer restrictions.”

- Native Collaboration (Securitize, Centrifuge): Essentially providing TaaS (Tokenization-as-a-Service) for target companies. Relying on transfer agent qualifications, they achieve legal mapping between on-chain tokens and shareholder registers, enabling true equity on-chain. Although slow to implement, they solve legal deadlock issues and provide compliant pathways for IPO transitions.

3. Trend Analysis: Tokenization does not automatically generate liquidity; the current market faces liquidity issues (thin markets, mispricing). The future breakthrough depends on collaboration with target companies:

- Compliance: Under regulatory and legal pressures, business models will shift toward compliance collaboration, with service providers offering TaaS infrastructure.

- Asset Side: Target assets will shift from top unicorns to private companies with more urgent exit needs.

- Infrastructure: Need to build native RWA trading facilities compatible with securities (e.g., compliant AMMs, on-chain order books) to address depth issues.

- Ecosystem: The market will evolve into a multi-layered symbiotic pattern rather than a winner-takes-all scenario. Synthetic assets serve as traffic entry and user cultivation; SPV-based indirect holding offers flexibility for early validation; native TaaS provides standardized paths for large-scale asset on-chain and institutional funding.

Keywords: Pre-IPO equity tokenization, RWA, SPV architecture, TaaS (Tokenization-as-a-Service), Transfer Agent

1. Scope and Key Definitions

Equity in private companies, especially high-growth unicorns, constitutes an important asset class in the global economy.[1] However, for a long time, access and value appreciation have been dominated by PE/VC and a few high-net-worth groups, making it difficult for ordinary investors to participate. As blockchain technology matures, “equity tokenization”—mapping equity shares to on-chain digital tokens within compliant boundaries—begins to be feasible, improving private asset circulation efficiency. Boston Consulting Group (BCG) projects that by 2030, the on-chain RWA market could reach $16 trillion.[2] This reflects high market interest: on one hand, due to the enormous value of top private companies; on the other, because tokenization technology is expected to lower traditional financial market barriers and transaction frictions.

Against this background, this paper systematically reviews the market background and current development of private equity tokenization, analyzes traditional market pain points and the advantages of tokenization mechanisms, and combines key platform cases, technology, regulation, and challenges to forecast future trends.

1.1. Research Focus

This report centers on the enterprise side—the tokenization of underlying rights of non-listed companies (especially unicorns)—specifically “target company equity” tokenization, rather than the tokenization of LP shares in private equity funds (PE Funds).

The reason is: discussions on “private equity fund tokenization” usually start from the investment side, using traditional financial frameworks, which often overlook the larger portion of equity structure in unicorns—such as founder holdings and employee stock ownership plans (ESOP). Omitting these can lead to underestimating the scope and real liquidity needs of “equity tokenization,” thus undervaluing the market’s potential and scalability.

1.2. Research Assumptions

Time Frame: The research is current as of December 27, 2025.

Data Basis: Since there is no unified official valuation for private equity, some market size and tokenization market cap figures are estimated from publicly available statistics and platform data.

Liquidity of Equity: Private equity inherently faces lock-up, transfer restrictions, and shareholder register management, making tokenization challenging. Therefore, the concepts of “theoretical full tokenization” and “traded (restricted) tokenization” are distinguished.

Currency and Exchange Rate: Multiple currencies are involved; all figures are presented in USD, with exchange rates approximated based on USD stablecoin assumptions, without scenario analysis for extreme de-pegging.

Special Products: Synthetic contracts on platforms like Bybit and Hyperliquid are measured by open interest (OI) and not included in “equity token market cap.”

2. Market Background: The “Trillion-Dollar Enclosure” of Private Equity

2.1. Asset Spectrum and Ownership Structure

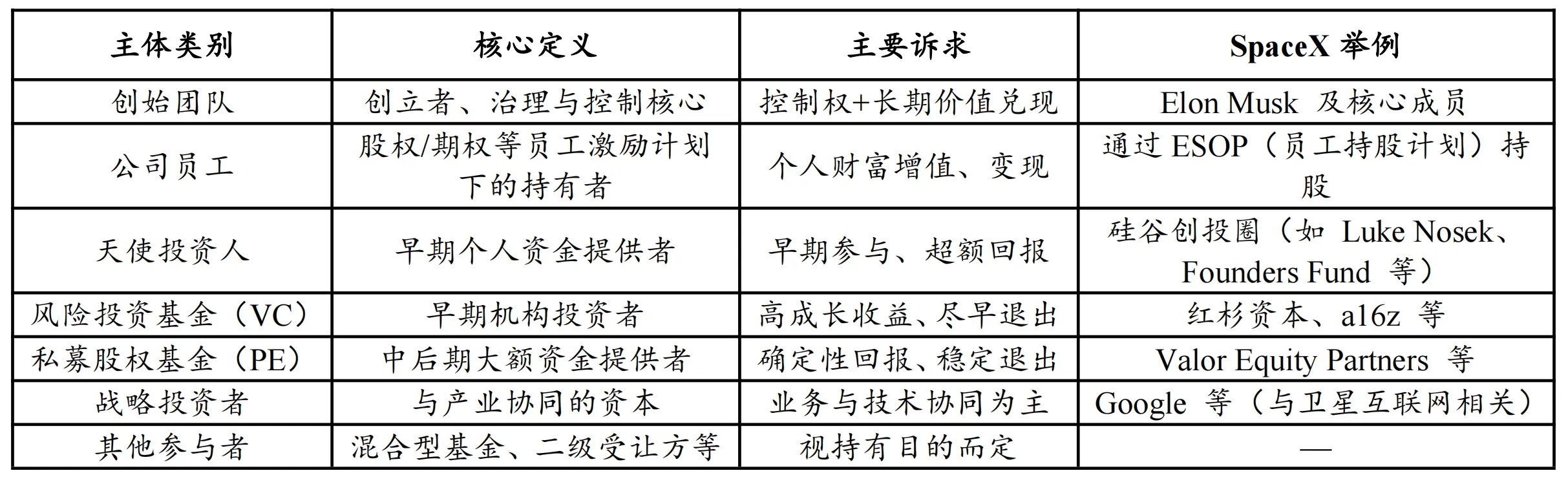

Broadly, private company equity includes all shares not listed on public exchanges, with highly diverse types—from early startups to mature private conglomerates. Holders are not limited to institutional funds but also include founders, employees (via equity or options), angel investors, VCs/PEs, strategic investors, and secondary market buyers.

Table 1: Common Ownership Structures in Private Equity

Source: PKUBA Research

Except for strategic investors and some founders, other equity holders often have varying exit demands: institutions emphasize exit efficiency; employees, upon departure or financial planning, need liquidity. Under traditional mechanisms, secondary market liquidity is low, making “exit difficulty” a persistent structural challenge.

2.2. Scale Illustration: Capital Allocation and Asset Valuation

It’s important to note that due to the lack of a unified official valuation for private equity, this section relies on mainstream institutional data, inferred from “capital allocation capacity” and “asset valuation scale.”

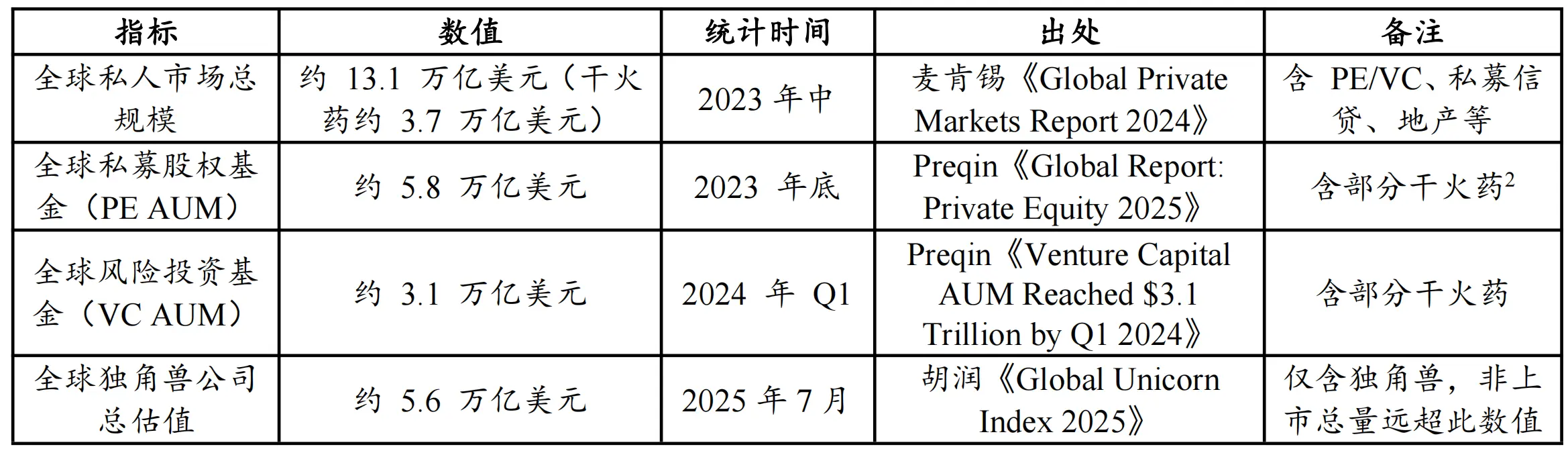

Table 2: Key Metrics of Global Private Markets and Unicorn Valuations

Sources: Hurun, McKinsey, Preqin

Data shows that “capital allocation capacity” (PE + VC assets under management) totals about $8.9 trillion (5.8T + 3.1T), forming a significant capital base for private equity assets;

Meanwhile, the valuation of unicorns alone reaches trillions. Hurun Research estimates that by mid-2025, unicorn valuations are about $5.6 trillion. CB Insights reports that as of July 2025, 1,289 unicorns worldwide are valued at over $4.8 trillion.[4]

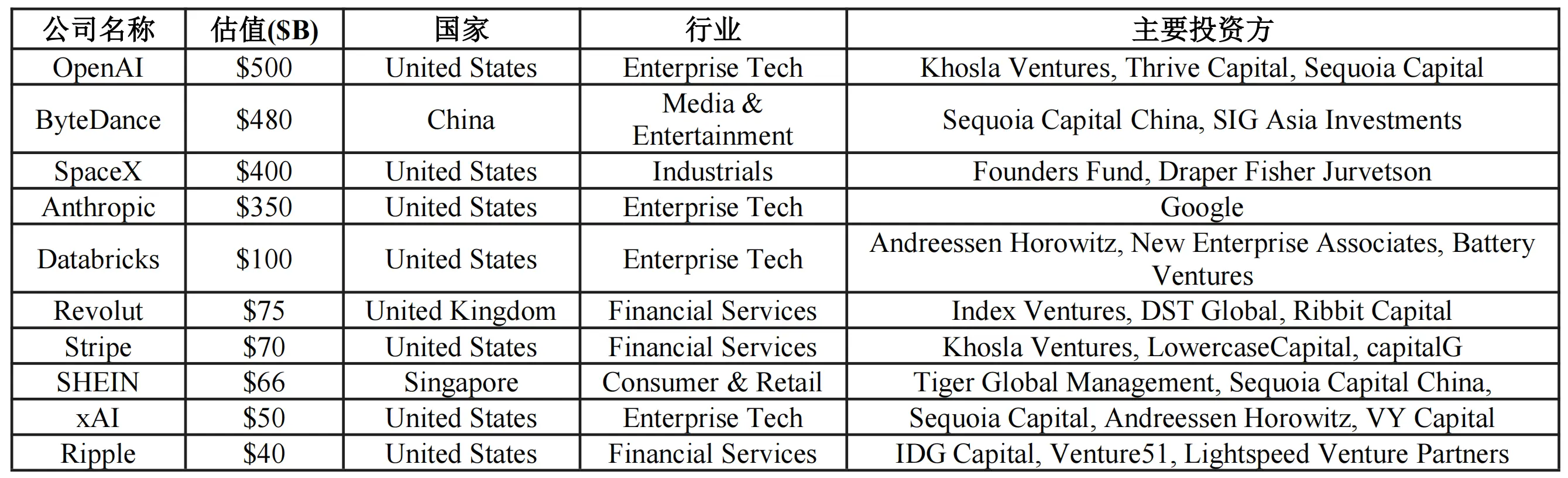

Table 3: Top 10 Global Unicorns by Valuation

Sources: CB Insights (as of December 2025)

It’s worth emphasizing that whether $4.8T or $5.6T, these figures only cover the top few thousand unicorns; the vast number of mature private and growth-stage companies below unicorn level are not included.

Overall, the total value of the global private equity market far exceeds several trillion dollars. This enormous, illiquid asset blue ocean offers promising application prospects for tokenization.

3. Core Contradictions and the Value Path of Tokenization

Private equity has long exhibited high valuation and low liquidity simultaneously, mainly due to dual constraints on participation and exit mechanisms. The potential value of equity tokenization lies in three aspects: transfer channels, price discovery, and financing.

3.1. Dual Bottlenecks: Participation Restrictions and Exit Difficulties

The structural feature of “high valuation—low liquidity” stems from dual constraints:

- Participation: High entry barriers restrict investor access—strict qualification rules, large minimum investments (hundreds of thousands to millions USD), and net worth/income requirements create institutional and capital barriers, leading to concentrated asset benefits and limited market supply.

- Exit: Reliance on IPOs or M&A for liquidity, but delayed listings of unicorns extend holding periods, making wealth realization slow. Private secondary transfers often involve offline negotiations, with issues like opacity, due diligence friction, high costs, and slow settlement, resulting in inefficient and unstable liquidity supply.

3.2. Three Gains: Transfer Channels, Price Discovery, and Financing

Compared to “public stock tokenization,” which mainly improves trading timing and channels, private equity tokenization is more about restructuring the private market:

- Transfer Channels: Tokenization can provide continuous secondary liquidity, building two-way channels for participation and exit.

- For participation: fractionalization lowers entry barriers, allowing more compliant investors to access growth assets.

- For exit: provides additional transfer options beyond IPO/M&A, expanding liquidity and potential buyers, improving exit flexibility without changing ultimate paths.

- Price Discovery: Introduces more continuous price signals, improving valuation accuracy and market cap management.

- Financing: Opens incremental financing channels, exploring STOs and “digital listings,” reducing IPO costs and cycle times, and offering new capital management options.

4. Market Status: From Narrative to Measurable Scale

4.1. Scale Status: Early Validation of “Tens of Millions”

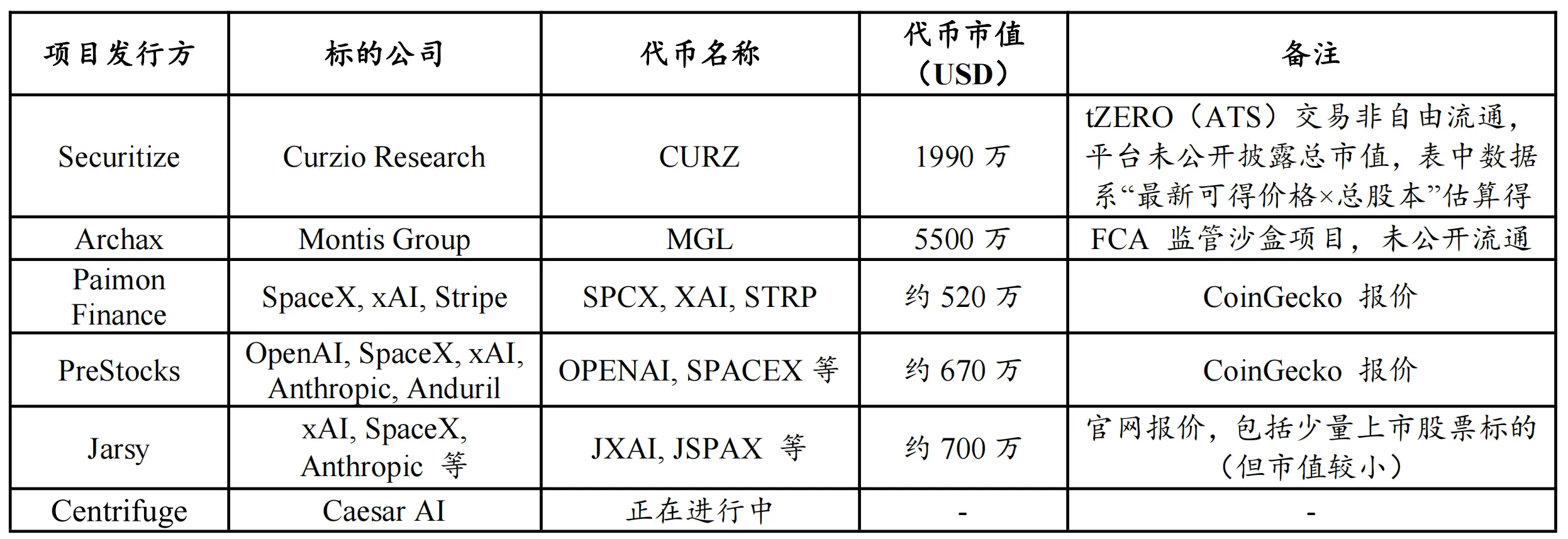

Due to some platforms not disclosing valuations and synthetic contracts measured by open interest, estimates are based on CoinGecko and project websites.

Table 4: Key Projects in Private Equity Tokenization (Incomplete)

Sources: CoinGecko, project websites, as of December 27, 2025

From these samples, it’s clear that the private equity tokenization market is still in early validation. Based on available data, the overall industry scale is roughly in the range of $10–20 million, excluding projects like Securitize (CURZ) and Archax (MGL) that are not freely tradable. The freely tradable market size is only in the low tens of millions USD.

This indicates that, despite the narrative potential, current secondary liquidity, trading depth, and participation breadth are limited, resembling a few samples completing market education and validation.

4.2. Target Preferences: Concentration in Top Tech Unicorns and AI Assets

Distribution of underlying assets shows high homogeneity and concentration in top US tech unicorns, especially AI-related assets like OpenAI, SpaceX, xAI, etc.

This preference is driven by early-stage projects prioritizing well-known, narrative-rich assets to lower education costs and attract trading volume, thus enabling product launch and market validation. Although some projects claim engagement with Chinese unicorns, no verified cases have emerged, indicating challenges in asset acquisition, compliance, and transaction structure.

5. Implementation Pathways: Structural Differences and Rights Boundaries

Practically, three main schemes have emerged for transforming private equity into tradable on-chain assets, differing mainly in: whether they hold actual shares, company participation, rights correspondence, and licensing.

Table 5: Comparison of Private Equity Tokenization Models

Sources: Pharos Research

5.1. Synthetic Asset: Value Mapping Without Underlying Rights

Synthetic assets typically do not involve target company permission or hold underlying shares. Instead, they issue contracts tracking valuation, providing economic exposure. Investors do not appear on shareholder registers or enjoy governance/dividends; returns depend on contract terms, making them akin to derivatives.

Advantages include fast deployment, flexible structure, and low dependence on asset acquisition; risks involve counterparty credit, tracking errors, settlement risks, and regulatory uncertainties across jurisdictions.

This path suits Web3-native traders and speculators but does not equate to true asset-on-chain equity. Examples include debt notes (Republic) and valuation perpetuals (Ventuals on Hyperliquid).

Figure 2: Ventuals White Paper on Equity Tokenization

Sources: Ventuals official documentation

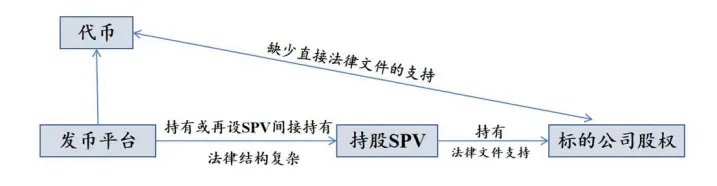

5.2. Indirect Holding via SPV: Mainstream Validation with Compliance Risks

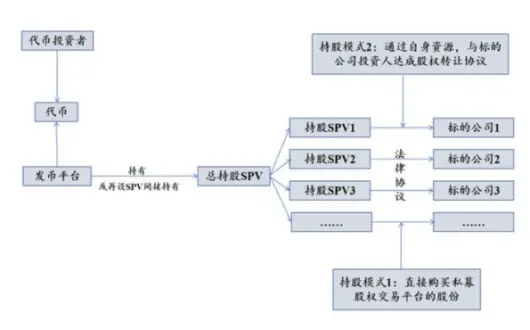

SPV structure: a platform establishes an offshore SPV holding real shares; the tokenized rights are claims on the SPV, not direct shares. Investors are usually not registered shareholders and lack direct governance rights.

Figure 3: SPV Indirect Holding Issuance Architecture

Sources: Pharos Research

Advantages include flexibility; risks include:

- Transparency challenges: offshore SPV complexity means investors can verify only “SPV holds shares,” not full operational/financial details.

- Company warning risks: if the target company considers the arrangement a violation of shareholder agreements or transfer restrictions, legal conflicts may arise.

5.3. Native Collaboration: Legal Equity on-Chain via Transfer Agent

This approach requires the target company’s deep participation, providing TaaS (Tokenization-as-a-Service). The key is having a qualified Transfer Agent (TA) to map on-chain tokens to offline shareholder registers, ensuring legal rights are preserved.

TA, often SEC-registered, manages shareholder records. Only when token transfers trigger legal register updates do tokens truly correspond to equity, enabling rights like voting, dividends, and information access. This makes the rights foundation clearer than SPV or synthetic paths.

However, this approach has higher implementation costs: regulatory scrutiny on transfer and custody, licensing requirements (Broker-Dealer, ATS), and compliance cycles. Current market progress:

- Opening Bell mainly works with listed companies; private company cooperation remains at the promotional stage.

- Securitize offers a strong compliance reference; further details follow.

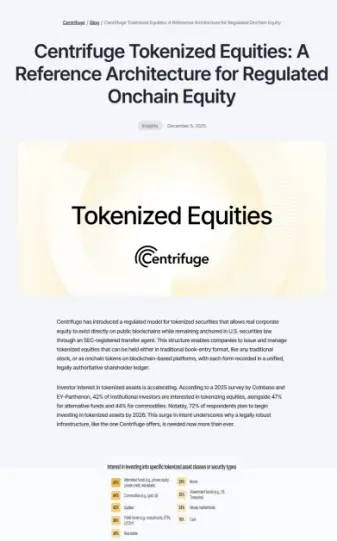

- Centrifuge, a leader in RWA, announced in November 2025 entry into private equity tokenization, shifting focus from private credit to private equity, with ongoing developments.

Figure 4: Centrifuge’s Entry into Private Equity Tokenization

Sources: Centrifuge official website

6. Case Studies: Typical Examples of Three Modes

Based on the pathways, compliance strategies and trading facilities differ significantly. This section dissects specific cases and compares their processes and effectiveness.

6.1. Synthetic Assets: Attracting Speculative Traffic

Synthetic assets do not hold underlying shares but split valuation into contracts, providing price exposure via on-chain matching. Practice mainly follows two paths:

- Perpetuals on DEX platforms (e.g., Hyperliquid-based Ventuals)

- Debt instruments in the form of tokenized notes (e.g., Republic’s Mirror Tokens)

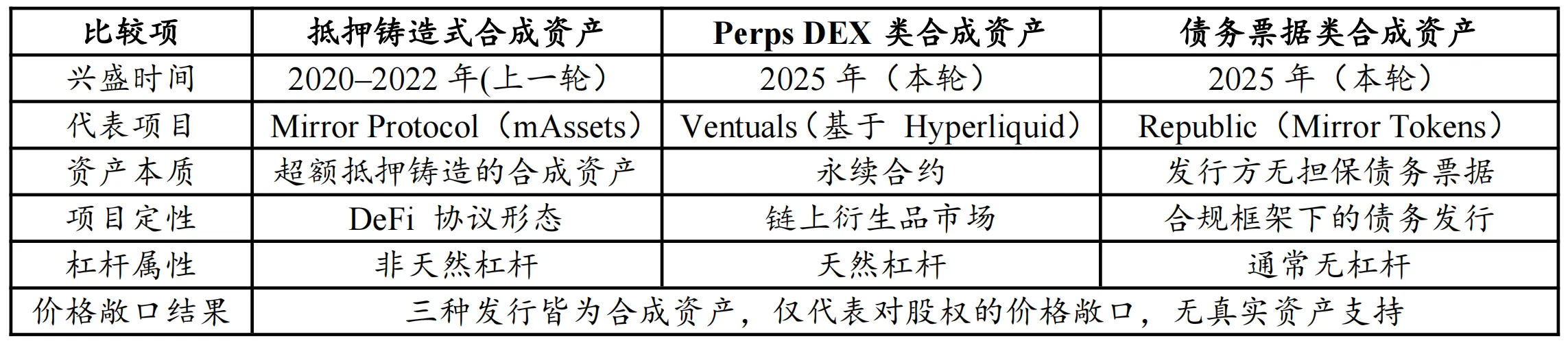

Both do not represent real shares or shareholder rights; differences lie in compliance boundaries, trading mechanisms, and capital attributes. They differ from previous collateral-backed synthetic narratives like Mirror Protocol.

Table 6: Comparison of Three Types of Equity Synthetic Assets

Sources: PKUBA Research

Market differentiation is clear:

- Republic’s approach aligns more with traditional finance, holding Broker-Dealer licenses and complying with US securities law.

- Perps DEX emphasizes native trading features, leveraging leverage, continuous liquidity, and low friction, with less emphasis on legal rights.

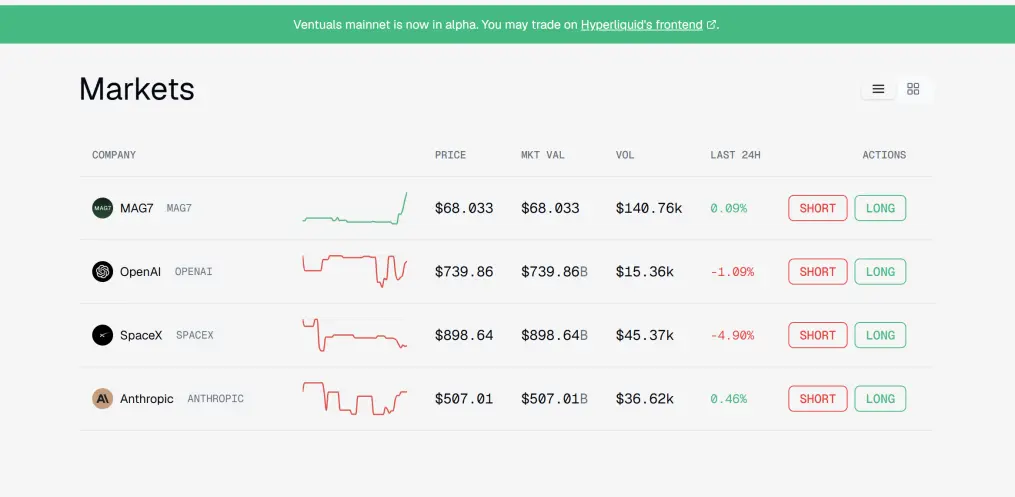

Figure 5: Ventuals Pre-IPO Contract Product Display

Sources: Ventuals official website

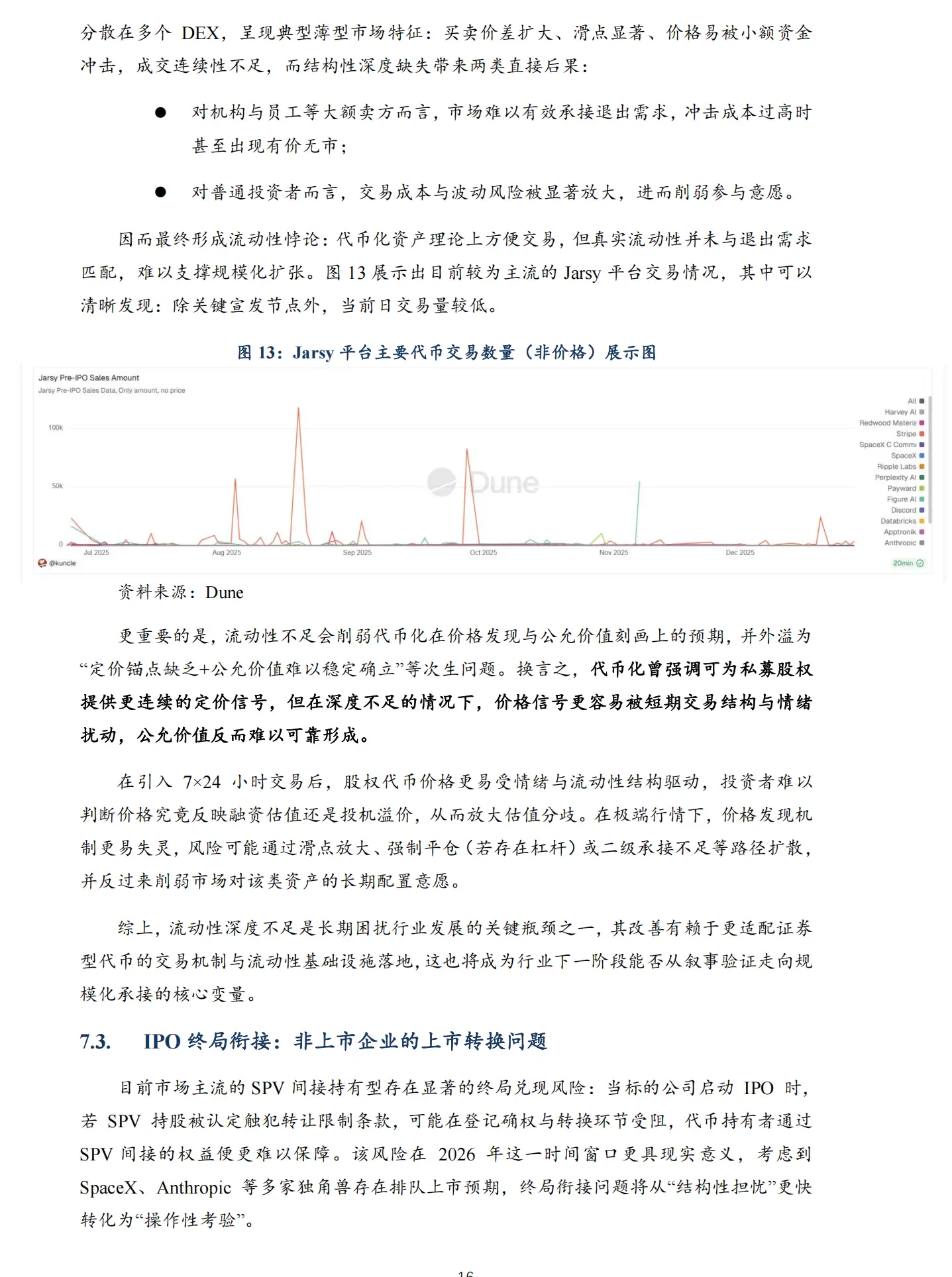

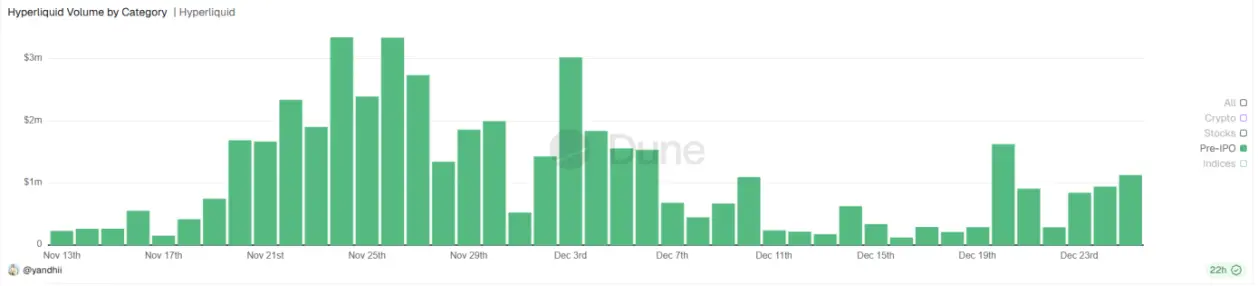

In liquidity, Hyperliquid’s perpetuals outperform. Dune data shows daily trading volume of Pre-IPO assets on Hyperliquid reaches millions USD, contrasting with SPV indirect holding’s secondary trading and depth (see later Figure 13). This is because synthetic assets, especially perpetuals, align with crypto market preferences: high-frequency, high-leverage trading attracts speculative traders, creating volume and educating users on non-listed equity exposure.

Figure 6: Hyperliquid Pre-IPO Asset Daily Trading Volume (USD)

Sources: Dune

Further analysis suggests synthetic assets are not necessarily substitutes for true equity on-chain but serve as demand builders and liquidity warm-up tools, attracting users and capital before transitioning to more compliant, rights-confirmed pathways.

6.2. SPV Indirect Holding: Low Barriers, High Compliance Risks

SPV structure: an offshore SPV holds target shares; the tokenized rights are claims on the SPV, not direct shares. Investors are typically not registered shareholders.

Figure 7: SPV Indirect Holding Token Issuance Architecture

Sources: Pharos Research

Advantages include lower barriers; risks involve:

- Transparency: complex offshore structures mean investors verify only “SPV holds shares,” not full operational details.

- Company warning risks: if the target considers the arrangement a breach of shareholder agreements or transfer restrictions, legal conflicts may occur.

6.3. Native TaaS: Regulatory-Approved On-Chain Rights

This approach requires the target company’s compliance, providing TaaS (Tokenization-as-a-Service). It involves a qualified Transfer Agent managing shareholder records and ensuring legal mapping between on-chain tokens and offline shares.

Centrifuge announced in December 2025 a reference architecture for regulated on-chain equity, emphasizing transparent, compliant transfer processes via licensed TA, aligning on-chain tokens with legal rights.

Figure 8: Securitize’s Compliance Architecture

Sources: Securitize official website

This approach is more costly but offers clearer legal rights and compliance. It is currently being tested mainly with listed companies; private company applications are still in early stages.

7. Challenges: Three Bottlenecks Limiting Industry Growth

Despite clear narrative and potential value, the sector faces rigid constraints that limit scalability:

- Regulatory Constraints: Higher complexity than listed stock tokenization, involving SEC oversight and company legal restrictions.

- Liquidity Depth: Thin markets and low trading volume hinder large-scale adoption.

- IPO Transition Uncertainty: Long and uncertain paths to IPO or exit, especially for unicorns delaying listing.

7.1. Regulatory Constraints: Dual Pressures

Compared to listed stock tokenization, private equity tokenization faces higher compliance hurdles:

- Regulatory: Product issuance and trading may trigger securities laws, requiring licenses and disclosures.

- Company legal: Share transfer restrictions (Transfer Restrictions) in shareholder agreements pose legal challenges. Structures like SPV or indirect transfer aim to bypass restrictions but risk violating agreements or triggering legal conflicts. Recent public statements from companies like OpenAI highlight external uncertainties.