Gold vs Bitcoin: 12 Years of Data Shows Who Is the True Winner

Author: Viee, Amelia | Biteye Content Team

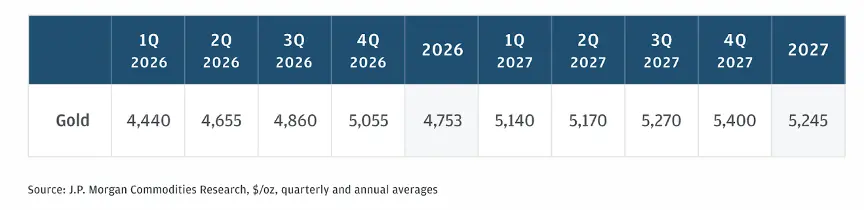

On January 29, 2026, gold experienced a single-day plunge of 3%, marking the largest drop in recent times. Just days earlier, gold broke through $5,600 per ounce to hit a new high, and silver also followed upward. The market had already far exceeded JPMorgan Chase’s mid-December expectations just at the start of 2026.

Data Source: JPMorgan Chase

In contrast, Bitcoin remains in a weak consolidation zone after a correction, and the market performance of traditional precious metals and Bitcoin continues to diverge. Despite being called “digital gold,” Bitcoin still seems unstable. During periods of inflation, war, and other traditional positive factors for gold and silver, Bitcoin instead behaves more like a risk asset, fluctuating with risk appetite. Why is this happening?

If we cannot understand Bitcoin’s actual role within the current market structure, we cannot make rational asset allocation decisions.

Therefore, this article attempts to answer from multiple angles:

- Why have precious metals recently surged?

- Why has Bitcoin performed so weakly over the past year?

- Looking back at history, how has Bitcoin performed when gold rises?

- For ordinary investors, how should they choose in this divided market environment?

1. Cross-Cycle Game: A Decade of Competition Between Gold, Silver, and Bitcoin

From a long-term perspective, Bitcoin remains one of the highest-return assets. But over the past year, Bitcoin’s performance has clearly lagged behind gold and silver. The market trend from 2025 to early 2026 shows a stark binary divergence: precious metals entered a “super cycle,” while Bitcoin showed slight weakness. Here are the key comparative data for three cycles:

Data Source: TradingView

Data Source: TradingView

This divergence in trend is not new. As early as the initial outbreak of the pandemic in early 2020, gold and silver surged due to risk aversion, while Bitcoin once plunged over 30%, before rebounding. In the 2017 bull market, Bitcoin soared 1359%, while gold only rose 7%. In the 2018 bear market, Bitcoin fell 63%, while gold declined just 5%. In the 2022 bear market, Bitcoin dropped 57%, with gold barely changing (+1%). This suggests that the correlation between Bitcoin and gold is unstable; Bitcoin is more like an asset at the intersection of traditional and new finance—possessing technological growth attributes, yet heavily influenced by liquidity and market sentiment, making it hard to equate with the centuries-old safe haven of gold.

Therefore, when we are surprised by “digital gold not rising while real gold explodes,” the real question should be: Is Bitcoin truly regarded as a safe haven by the market? Based on current trading structures and main capital behaviors, the answer may be negative. In the short term (1-2 years), gold and silver outperform Bitcoin, but over the long term (10+ years), Bitcoin’s returns are 65 times that of gold—over time, Bitcoin’s 213-fold gains prove that it may not be “digital gold,” but it is the greatest asymmetric investment opportunity of this era.

2. Analysis of Reasons: Why Have Gold and Silver Surged More Than BTC Recently?

Behind the frequent new highs of gold and silver and the lagging narrative of Bitcoin lies not only price divergence but also a deep disconnect in asset attributes, market perception, and macro logic. We can understand the watershed between “digital gold” and “traditional gold” from four perspectives.

2.1 Trust Crisis: Central Banks Lead Buying Gold

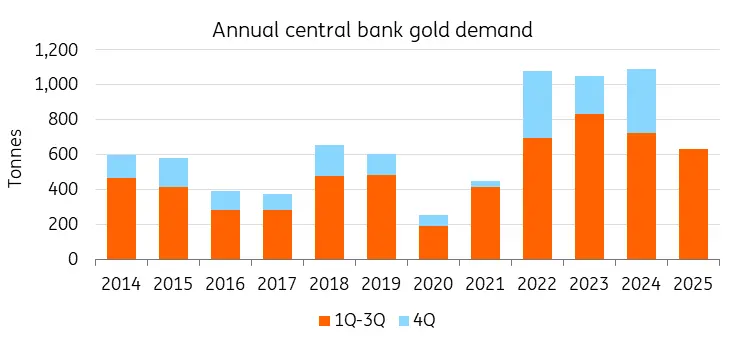

In an era of strong expectations of currency devaluation, who keeps buying determines the long-term trend of assets. From 2022 to 2024, central banks worldwide have consecutively increased gold holdings for three years, with an average net purchase of over 1,000 tons annually. Emerging markets like China and Poland, as well as resource-rich countries like Kazakhstan and Brazil, regard gold as a core reserve asset against dollar risk. The key point is: the higher the price, the more central banks buy—this “buy more as it gets more expensive” behavior reflects their firm belief in gold as the ultimate reserve asset. Bitcoin, however, struggles to gain recognition from central banks due to structural issues: gold has a 5,000-year consensus and does not rely on any national credit; Bitcoin requires electricity, network, and private keys, which central banks are reluctant to allocate on a large scale.

Data Source: World Gold Council, ING Research

2.2 Gold and Silver Return to “Physical Priority”

As global geopolitical conflicts escalate and financial sanctions become frequent, asset safety becomes a question of whether assets can be兑现 (fulfilled/realized). After the new US administration took office in 2025, policies such as high tariffs and export restrictions disrupted global markets, making gold the only ultimate asset that does not depend on other countries’信用 (credit). Meanwhile, silver’s industrial value began to be unleashed: expansion in new energy, AI data centers, photovoltaic manufacturing, etc., increased industrial demand for silver, driven by real supply-demand mismatches. In this context, silver’s speculative and fundamental resonance naturally led to a sharper rise than gold.

2.3 Structural Dilemma of Bitcoin: From “Safe Haven” to “Leveraged Tech Stock”

Previously, Bitcoin was seen as a tool to counteract central bank money printing, but with ETF approvals and institutional entry, the capital structure has fundamentally changed. Wall Street institutions include Bitcoin in portfolios mainly as a “high elasticity risk asset”—we see from data that in late 2025, Bitcoin’s correlation with US tech stocks reached 0.8, an unprecedented high, indicating Bitcoin is increasingly like a leveraged tech stock. When markets face risks, institutions prefer to sell Bitcoin first for cash, unlike gold, which is bought during risk-off periods.

Data Source: Bloomberg

More representative is the crash on October 10, 2025, where $19 billion of leveraged positions were liquidated in one go. Bitcoin did not show safe-haven traits; instead, its high leverage structure caused a collapse.

2.4 Why Is Bitcoin Still Falling?

Besides structural issues, there are three deeper reasons for Bitcoin’s recent sluggishness:

Crypto ecosystem dilemma: lagging behind in ecosystem development. While AI tracks attract massive capital, the crypto scene still plays Meme games. No killer app, no real demand—only speculation.

Shadow of quantum computing: the threat is not unfounded. Although true quantum cracking still takes years, this narrative has already deterred some institutions. Google’s Willow chip has demonstrated quantum advantage, and while Bitcoin’s community researches quantum-resistant signatures, upgrades require consensus, slowing progress but making the network more robust.

Early adopters selling off: many early Bitcoin holders are exiting. They feel Bitcoin has “gone astray”—from a decentralized idealistic currency to a Wall Street speculative tool. After ETF approval, Bitcoin’s core spirit seems lost. Institutions like MicroStrategy, BlackRock, Fidelity hold increasing positions, and Bitcoin’s price is no longer driven by retail but by institutional balance sheets. This is both positive (liquidity) and negative (loss of original purpose).

3. Deep Dive: The Historical Correlation Between Bitcoin and Gold

Reviewing the historical correlation between Bitcoin and gold reveals that their prices are often loosely related during major economic events, frequently diverging. Therefore, the “digital gold” label is often invoked not because Bitcoin truly resembles gold, but because markets need a familiar reference point.

First, Bitcoin’s correlation with gold has never been safe-haven resonance from the start. Early on, Bitcoin was in the geek community’s infancy, with minimal market cap and attention. In 2013, Cyprus’s banking crisis led to capital controls, and gold prices fell sharply (~15%), while Bitcoin soared past $1,000. Some interpret this as capital fleeing and safe-haven funds flowing into Bitcoin, but in hindsight, Bitcoin’s 2013 surge was mainly driven by speculation and early sentiment, not broad safe-haven recognition. During that year, gold plunged while Bitcoin soared, with a correlation coefficient of only 0.08—almost zero.

Second, periods of synchronization only occurred during liquidity floods. Post-2020 pandemic, unprecedented monetary easing by central banks and rising inflation expectations caused both gold and Bitcoin to rally. In August 2020, gold hit a new high (over $2,000), and Bitcoin broke $20,000 at year-end, accelerating to over $60,000 in 2021. Many see this as Bitcoin beginning to demonstrate “inflation hedge” qualities like digital gold, benefiting from loose monetary policies. But fundamentally, both benefited from the same environment—Bitcoin’s volatility was much higher (annualized volatility 72% vs. 16% for gold).

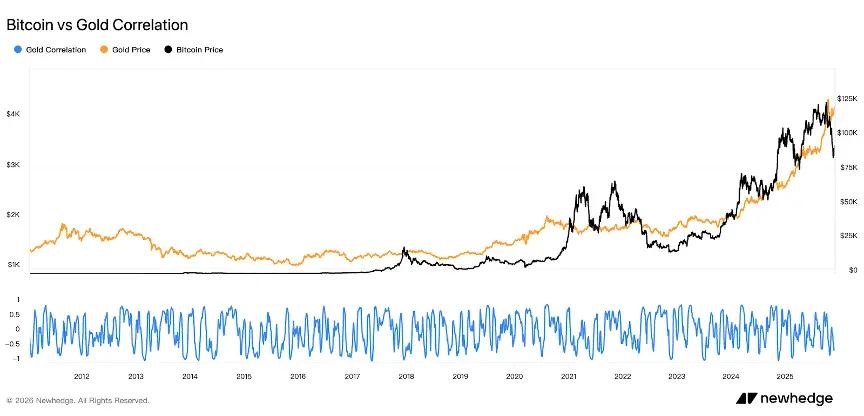

Third, the long-term correlation between Bitcoin and gold remains unstable, and the “digital gold” narrative still needs validation. Data shows that their correlation fluctuates over time, often negative, especially after 2020. This indicates Bitcoin has not stabilized as “digital gold,” with its movements more driven by independent market logic.

Data Source: Newhedge

In summary, gold has repeatedly proven to be a safe-haven asset, while Bitcoin resembles a non-traditional hedge tool that only fits certain narratives. When crises hit, markets still prefer certainty over speculation.

4. The Essence of Bitcoin: Not Digital Gold, But Digital Liquidity

Let’s look at it from another angle: what role should Bitcoin truly play? Is it really meant to be “digital gold”?

First, Bitcoin’s fundamental attributes make it inherently different from gold. Gold is physically scarce, does not rely on networks or systems, and is a true end-of-world asset. In geopolitical crises, gold can be physically delivered at any time, serving as the ultimate safe haven. Bitcoin, however, depends on electricity, networks, and computational power; ownership relies on private keys, and transactions depend on network connectivity.

Second, Bitcoin’s market performance increasingly resembles a high-elasticity tech asset. In periods of liquidity abundance and rising risk appetite, Bitcoin often leads gains. But in rising interest rates and risk-off environments, institutions tend to reduce holdings. Currently, the market still sees Bitcoin as a “high-risk, high-reward” speculative asset—possessing both high growth and volatility, as well as a hedge against uncertainty. This “risk-hedge” ambiguity may only be clarified after more cycles and crises. Until then, markets tend to treat Bitcoin as a high-risk, high-return speculative asset, correlated with tech stocks.

Perhaps only when Bitcoin demonstrates a stable store of value akin to gold can this perception change. But Bitcoin will not lose its long-term value; it still has scarcity, global transferability, and decentralization advantages. Its current market positioning is more complex: it is a pricing anchor, a trading asset, and a speculative tool simultaneously.

The overall stance: gold is an inflation-hedging safe haven; Bitcoin is a growth asset with higher return potential. Gold is suitable for preserving value during economic uncertainty—low volatility (16%), small maximum drawdown (-18%), acting as a “shock absorber.” Bitcoin is suitable for allocation in periods of abundant liquidity and rising risk appetite—annualized returns up to 60.6%, but with high volatility (72%) and maximum drawdown of -76%. This is not an either-or choice but a combination in asset allocation.

5. Opinions from Key Opinion Leaders (KOLs)

In this macro re-pricing cycle, gold and Bitcoin are playing different roles. Gold acts more like a “shield,” defending against war, inflation, and sovereign risks; while Bitcoin acts more like a “spear,” capturing value from technological change.

OKX CEO Xu Mingxing @star_okx emphasizes that gold is a product of old trust, while Bitcoin is a new trust foundation for the future. Choosing gold in 2026 is akin to betting on a failing system. Bitget CEO @GracyBitget states that despite inevitable market volatility, Bitcoin’s long-term fundamentals remain unchanged, and she remains optimistic about its future. KOL @KKaWSB cites Polymarket’s forecast data, predicting Bitcoin will outperform gold and the S&P 500 in 2026, believing in the eventual realization of value.

KOL @BeiDao_98 offers an interesting technical perspective: Bitcoin’s RSI relative to gold has dropped below 30 again, and historically, such signals often precede Bitcoin’s bull run. Well-known trader Vida @Vida_BWE suggests that after gold and silver led a surge, the market is eager to find the next “dollar substitute,” so some small positions in BTC have been bought, betting on capital rotation and FOMO over the coming weeks.

KOL @chengzi_95330 presents a broader narrative: first, traditional hard assets like gold and silver absorb the credit shocks from currency devaluation; only after they complete their roles does Bitcoin enter. This “traditional first, digital later” path may be the current story unfolding in the market.

6. Three Practical Recommendations for Retail Investors

Faced with the differing gains of Bitcoin and precious metals, common questions from retail investors are: “Which should I invest in?” There’s no one-size-fits-all answer, but here are four practical suggestions:

Understand the asset roles and clarify your investment goals. Gold and silver still have strong “hedging” attributes during macro uncertainty, suitable for defensive allocations; Bitcoin is more suitable when risk appetite rises and tech growth logic dominates, but don’t expect to get rich overnight with gold. For inflation hedging and safe haven—buy gold; for long-term high returns—buy Bitcoin (but be prepared for -70% drawdowns).

Don’t expect Bitcoin to always outperform everything. Its growth comes from technological narratives, capital consensus, and institutional breakthroughs, not a linear yield model. It won’t always outperform gold, Nasdaq, or oil annually, but its decentralized nature still holds value over the long term. Don’t dismiss it during short-term dips, nor go all-in during surges.

Build a diversified portfolio, accepting that different assets perform differently across cycles. If your perception of global liquidity is weak and risk tolerance limited, consider a mix of gold ETFs + small BTC holdings to hedge macro scenarios; if you have higher risk appetite, combine ETH, AI sectors, RWA, and other emerging assets for a more volatile portfolio.

4️⃣ Is it still advisable to buy gold and silver now? Be cautious about chasing highs; prioritize buying on dips. Long-term, gold remains favored by central banks, and silver’s industrial attributes add value during turbulent periods. But short-term, their gains are large, and technical corrections are likely. The 3% single-day drop in gold on January 29 is an example. Long-term investors can wait for dips—buy below $5,000 for gold, below $100 for silver, and gradually accumulate. Short-term traders should watch the rhythm and avoid chasing the hottest market moments. Although Bitcoin’s recent performance is weak, if liquidity expectations improve later, it might be a good low-position entry point. Focus on market rhythm, avoid chasing highs or panic selling—this is the core defensive strategy for ordinary investors.

Final Words: Understanding Asset Roles Is Key to Survival!

When gold rises, no one questions Bitcoin’s value; when Bitcoin falls, it doesn’t mean gold is the only answer. In this era of redefined value anchors, no single asset can meet all needs at once.

In 2024-2025, gold and silver lead the way. But over a 12-year horizon, Bitcoin’s 213-fold return proves it may not be “digital gold,” but it is the greatest asymmetric investment opportunity of this era. Last night’s gold plunge might be a short-term correction ending or the start of a larger retracement.

For ordinary traders, the most important thing is to understand the roles behind different assets and establish your own investment logic for survival across cycles.

Good luck to everyone!

Related Articles

Data: In the past 24 hours, the entire network has been liquidated by $341 million, mainly short positions.