Bank of America warns of narrowing P/E, Bitcoin faces structural pressure

The latest market outlook from Bank of America is not merely a short-term negative forecast but a structural warning: what will happen when the market stops paying high valuations, even if corporate profits continue to grow.

The bank believes that the S&P 500 is currently “statistically expensive” according to 18 out of 20 valuation metrics, with four indices approaching record highs. Although they forecast corporate earnings could rise sharply by about 14%, they still expect the P/E ratio to contract.

A scenario of rising profits but declining valuations creates a classic “risk-off” environment — which is unfavorable for Bitcoin. This asset is increasingly trading like high-volatility tech stocks, rather than serving as a diversification hedge as emphasized during the initial phase of institutional interest.

Narrowing P/E Despite Stable Profits

Notably, Bank of America does not forecast a collapse in profits. The year-end target for the S&P 500 at 7,100 points implies a significant valuation contraction, even with earnings at the high end of market consensus.

Valuation pressures stem from five main factors:

- Lower profit forecasts after price corrections

- A wave of new IPOs increasing stock supply

- Rising leverage and asset levels on corporate balance sheets

- Risks from private sector incidents affecting indices

- Market structure becoming more sensitive to liquidity shocks

The software sector is seen as the most pressured, down about 20% since the start of the year, with valuations near multi-year lows amid concerns over AI investment returns. According to Bank of America, this sector is unlikely to recover quickly.

Changing Correlation Between Bitcoin and Stocks

The relationship between crypto and traditional stocks has changed markedly since 2020. CME Group research shows Bitcoin’s correlation with Nasdaq reaching around 0.35–0.6 during 2025–early 2026. Crypto often amplifies stock volatility, especially during sharp declines.

The “digital gold” narrative is gradually giving way to reality: Bitcoin operates like a high-liquidity beta in a multi-asset portfolio — an extension of the high volatility of US tech stocks, which are often sold off before risk appetite diminishes.

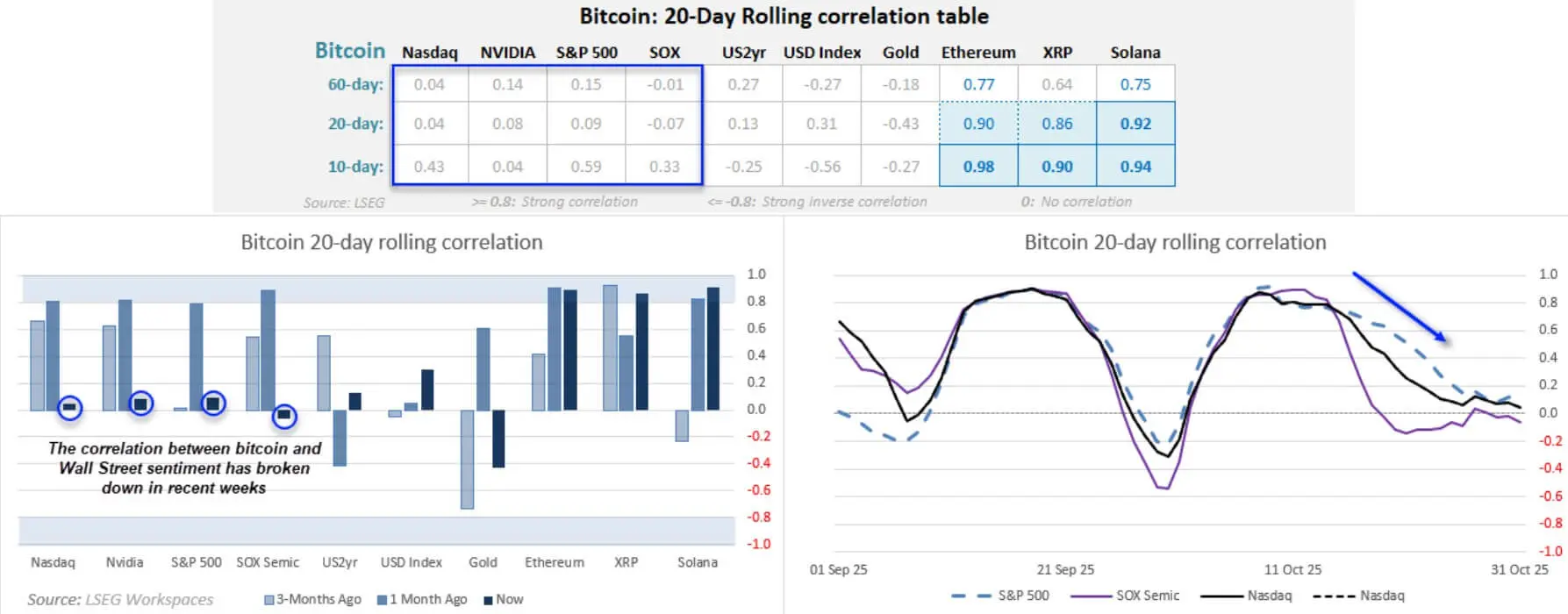

20-day correlation data shows Bitcoin sometimes has low correlation with the S&P 500 and Nasdaq, but maintains a very high positive correlation with major digital assets like Ethereum, XRP, and Solana.

As of late October 2025, the 20-day correlation of Bitcoin with major stock indices approaches zero with the S&P 500 and Nasdaq, while maintaining a strong positive correlation above 0.90 with Ethereum, XRP, and Solana.## Non-yielding assets under pressure as real yields rise

As of late October 2025, the 20-day correlation of Bitcoin with major stock indices approaches zero with the S&P 500 and Nasdaq, while maintaining a strong positive correlation above 0.90 with Ethereum, XRP, and Solana.## Non-yielding assets under pressure as real yields rise

When risk premiums increase or real yields go up, assets with “long duration” tend to be heavily adjusted. Bitcoin has no cash flows, no dividends, no terminal value — yet in practice, it reacts very sensitively to discount rates.

The transmission mechanism lies in the discount rate: if stocks with actual cash flows see their P/E ratios compressed because investors pay less for future growth, then expectation-dependent assets like Bitcoin often face greater pressure.

If the Fed signals a slowdown in rate cuts after inflation data, Bitcoin’s “implied duration” could be revalued similarly to growth stocks.

BlackRock also emphasizes that the crypto trajectory in 2026 largely depends on liquidity conditions and the pace of rate cuts, viewing monetary policy as the primary driver.

Reducing Multi-Asset Leverage and Liquidity Shocks

Periods of deleveraging in multi-asset portfolios show that crypto is vulnerable to broad sell-offs. In a stress session in early February, Bitcoin liquidations exceeded $1 billion, coinciding with tech stock corrections and weakening crypto ETF flows.

This is not a crypto-specific shock but reflects Bitcoin’s position in the “liquidity hierarchy”: when portfolio managers need to quickly reduce exposure, they sell assets that are both highly liquid and volatile — and Bitcoin fits both criteria.

IMF has noted increasing risk spillover between crypto and traditional financial assets, especially during volatile periods.

Analyses from Reuters also point to a wave of debt financing for AI investments boosting corporate leverage, making the system more fragile — conditions that can trigger widespread sell-offs, with Bitcoin at the intersection of maximum liquidity and volatility.

Spot ETFs Turn Sentiment into Daily Cash Flows

The advent of spot Bitcoin ETFs makes the risk-off transmission to prices more mechanical. What was once only reflected in “market sentiment” now directly manifests through daily fund inflows and outflows.

CoinShares reports weekly outflows reaching $1.7 billion in early February, with Bitcoin accounting for about $1.32 billion — enough to reverse the year-to-date inflow trend into outflows.

The ETF structure creates a tight feedback loop:

Weak stock performance → ETF outflows → downward pressure on Bitcoin → triggering stop-losses and leverage liquidations → further outflows.

This makes technical rebounds more suspect if prices rise but ETF flows remain negative or neutral — a sign of lacking institutional confirmation.

Spillover Risks from AI and Software Stocks

Bank of America’s identification of the software sector as the weakest area this year signals more than just stock analysis. Deep valuation declines reflect growing skepticism about AI spending efficiency and the sustainability of growth narratives.

As markets shift from “AI is transformative” to “AI spending may be overvalued,” the typical reaction is not selective selling but broad beta liquidation. Bitcoin is often lumped into this high-beta group despite lacking direct AI exposure.

Nvidia’s earnings report serves as a short-term test. If outlooks disappoint or raise doubts about AI investment returns, selling pressure could spread to tech stocks and drag Bitcoin down. Conversely, if market confidence is restored, crypto could temporarily “relieve pressure” — provided capital flows return.

Three Short-Term Scenarios and Catalytic Windows

Base case: orderly valuation correction. Mixed profits, stable inflation, cautious Fed stance. Stocks sideways or slightly down, P/E ratios contract gradually. Bitcoin remains volatile but leans toward downside, with rebounds vulnerable if ETF flows weaken.

Bad scenario: “AI black hole.” Nvidia’s outlook sparks fears, software stocks plunge further, stock volatility spikes. Bitcoin drops more than stocks due to high liquidity beta; ETF outflows and leverage liquidations accelerate.

Good scenario: macro data cools and AI outlook stabilizes. Inflation eases, Fed signals earlier easing, Nvidia reassures markets. Stocks recover, and Bitcoin could outperform thanks to risk-on flows and improved ETF demand — but only if multiple conditions align.

Structural Pressures on Bitcoin if Stock Valuations Contract

Upcoming key dates include Nvidia’s earnings, CPI data, and Fed meetings. These events will determine whether the valuation contraction thesis from Bank of America unfolds swiftly or is delayed.

If markets shift from “perfect valuation” to “pay less for risk,” Bitcoin is likely to be sold as a high-liquidity beta asset — through deleveraging, liquidity tightening, and ETF mechanisms — before any “decoupling” narrative can develop.

According to Bank of America, the chance of a rapid rebound is low. If this scenario materializes, Bitcoin will face structural headwinds, not from its intrinsic factors but from its position within the high-volatility risk asset ecosystem when markets cease paying high valuations.

Related Articles

Bitcoin On-Chain Activity Falls to Six-Month Low, Raising Red Flags for Traders