In-Depth Analysis of Hyperliquid: The King of On-Chain Contracts — Pushing DeFi into the "Exchange Era"

Author: Climber, CryptoPulse Labs

In recent years, DeFi has spawned countless trading products, but truly bringing professional trading on-chain is rare. The emergence of Hyperliquid has, to some extent, changed this landscape.

It’s not just deploying a contract-based DEX on Ethereum; it’s creating a Layer1 built specifically for trading. It aims to handle order books, matching, execution, and settlement as much as possible on-chain, while refining the user experience to be close to that of centralized exchanges. As a result, a huge market traditionally belonging to CEXs—perpetual contracts—is now being genuinely disrupted by on-chain forces.

Hyperliquid is regarded as the king of on-chain derivatives, but it’s also controversial due to its risk control, decentralization level, and systemic risks. Does it represent the next leap for DeFi, or is it a more complex risk experiment? This article will analyze Hyperliquid’s true nature through product logic, token value, and potential risks.

1. Hyperliquid: Making On-Chain Derivatives as User-Friendly as Exchanges

If we view the development of DeFi as a main storyline, a harsh truth emerges: most on-chain financial products fail not because of concept but because of user experience.

On-chain lending, DEX swaps, yield aggregators—these are naturally suited for slow, low-frequency operations. Users can accept slower confirmations, larger slippage, higher fees.

But perpetual contracts are entirely different. They are high-frequency financial products where traders demand millisecond response times, stable depth, smooth order cancellations and placements, and system stability even in extreme market conditions.

Hyperliquid’s core value lies here. It’s arguably the first platform that allows ordinary users to experience on-chain perpetual contracts with order book quality comparable to CEXs.

First-time users will have a strong impression: it doesn’t feel like DeFi, more like Binance or OKX. Its interface, order logic, market depth, and execution speed are approaching centralized exchange standards.

More importantly, this isn’t achieved by sacrificing transparency. Instead, it places key actions—order book, matching, execution, settlement—on-chain as much as possible, making the entire process verifiable. This is why Hyperliquid has suddenly emerged between 2024 and 2026.

The derivatives market is the largest cash flow entry point in crypto. CEXs earn most fees from contract trading, but DeFi has long lacked products capable of supporting this demand at scale.

Historically, on-chain perpetual contracts have mainly followed two paths: AMM models like GMX, which rely on liquidity pools for quoting, or order book models with off-chain matching, which often feel disjointed and reduce decentralization.

AMMs are unfriendly to professional traders—depth, quotes, and slippage become unsatisfactory at large sizes. Off-chain matching suffers from transparency issues, leaving users suspicious of hidden manipulations.

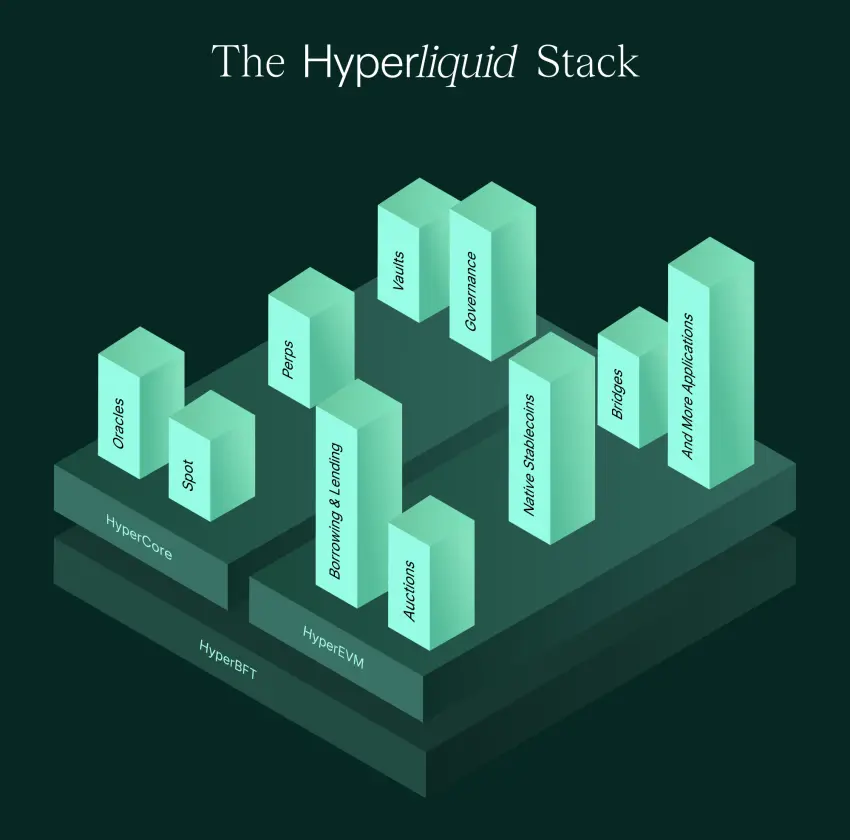

Hyperliquid chose the most aggressive route: since on-chain order book high-frequency trading is hard to sustain, it built a dedicated chain for trading.

It treats exchanges as a fundamental blockchain requirement, rather than shoehorning a trading app onto a general-purpose chain.

Beyond user experience, Hyperliquid also successfully solves the classic liquidity problem of order book DEXs.

Its HLP (Hyperliquid Liquidity Provider) mechanism essentially productizes market-making capability, allowing users to deposit funds into a liquidity pool, with the system executing market-making strategies and sharing trading fees and spread profits.

This makes the platform’s liquidity less dependent on external market makers, creating an endogenous cycle. Higher trading volume means more fees, stronger market-making profits, attracting more funds, improving depth, enhancing experience, and further increasing volume.

Thus, Hyperliquid’s rise isn’t mysterious. It’s fundamentally a product-driven project in DeFi, relying on real traders to generate volume.

2. The HYPE Boom—On-Chain Exchange Equity Narrative

Talking about Hyperliquid inevitably involves HYPE. Many see HYPE as just another platform token, but if viewed solely through the lens of a platform token, its valuation logic appears quite ordinary.

HYPE is more like a hybrid asset, embodying both the value capture potential of a trading platform and the network effects of a native blockchain asset, mainly backed by derivatives trading.

Derivatives are the engine of crypto markets. Spot trading is mainly buying and selling assets, while contracts are like a continuous fee-generating casino—higher trading frequency, more stable fees, and stronger user stickiness.

CEX dominance largely comes from derivatives. Hyperliquid’s significance is that it shows for the first time that contract trading doesn’t have to be exclusively provided by centralized exchanges. With a good enough experience, deep liquidity, and reliable liquidation, on-chain platforms can support large-scale perpetual contract trading.

This opens up a market imagination: if Hyperliquid captures more on-chain derivatives volume, it could become a “chain-based Binance,” with HYPE being akin to BNB.

But Hyperliquid isn’t content just to be a contract platform. It plans to expand into a broader on-chain financial ecosystem with the HyperEVM initiative in 2025–2026, transforming from a trading platform into a comprehensive DeFi ecosystem.

The significance of EVM compatibility is straightforward: it attracts Ethereum developers, enabling DeFi’s financial Lego components to grow on Hyperliquid’s chain.

Exchanges provide traffic and capital; ecosystems provide applications and stickiness. This has been the most successful path for CEXs over the past decade: use trading as an entry point, then expand the moat through ecosystem development. Hyperliquid is now bringing this model on-chain.

Additionally, Hyperliquid’s marketing approach is more like “crypto fundamentalism”: emphasizing product quality, traders, and community-driven growth. Its user base includes many professional traders and high-frequency players, not just retail users chasing airdrops.

This user structure signals that Hyperliquid isn’t a bubble built on subsidies but a genuine, sustainable trading venue. After experiencing many bubble projects, this authenticity is especially valuable.

3. Hyperliquid’s Dilemma: Decentralization Tensions, Systemic Risks, HLP Risks, and Regulation

Looking solely at Hyperliquid’s growth curve, many might think the on-chain derivatives king has arrived. But in reality, Hyperliquid faces intense controversy, mainly stemming from inherent contradictions in its business approach.

The biggest contradiction is decentralization. Many call Hyperliquid “on-chain Binance,” which is both praise and criticism. Praise for delivering top-tier experience; criticism because it behaves more like a centralized platform in areas like risk control, bans, and address restrictions.

Hyperliquid currently adopts a pragmatic, middle-ground approach: to ensure system stability and reduce attacks or abnormal fund flows, it may implement stronger risk controls.

But the more robust the risk controls, the more it resembles a CEX, which weakens its decentralization narrative. This contradiction will only intensify as it scales. Larger trading volume and influence mean greater risk management needs and increased external scrutiny.

The second systemic risk comes from the derivatives system itself. Perpetual contracts are complex financial products with inherent systemic risks—extreme market moves, cascade liquidations, underfunded insurance pools, bad debts, and failed forced liquidations—all can trigger trust crises if mishandled.

Hyperliquid’s challenge is to maintain transparency on-chain while ensuring reliable liquidations during extreme conditions.

CEXs can use off-chain measures—pausing trading, adjusting risk parameters, forced liquidations, or rule changes—to manage crises. On-chain systems lack such flexibility, requiring stronger mechanisms and resilience.

Has Hyperliquid truly undergone sufficient stress testing under extreme conditions? This is a critical question for cautious assessment.

The third risk involves HLP. Many new users see HLP and mistakenly think it’s a “stable yield pool,” but it’s more like a market-making fund.

Its returns come from fee sharing and spread profits, but risks stem from traders’ counterparty advantage and unilateral shocks during extreme markets. Market-making is never risk-free; it’s a specialized field. HLP’s core is funds entrusted to the system for market-making, but users bear the risk of being “harvested” by “whales.”

In a bull market with high volume and fees, HLP looks profitable. But in certain conditions, it can suffer significant drawdowns. For ordinary users, the biggest risk isn’t just losses but misunderstanding the risk—treating it as a low-risk investment.

Finally, regulatory and real-world risks loom. Derivatives are heavily regulated in traditional finance, and perpetual contracts are sensitive products in many jurisdictions.

As a on-chain platform, Hyperliquid may initially operate in a gray area. But once it scales and enters mainstream view, regulatory pressure will be almost inevitable.

Conclusion

Hyperliquid isn’t a myth; it marks the entry of DeFi into the “exchange era.”

Its importance isn’t just about a token pump but proves that on-chain derivatives can reach near-CEX experience and attract real traders to migrate.

From an investment perspective, the platform remains a high-risk derivatives system. It still faces decentralization debates, and as it scales, it must confront extreme market conditions and regulatory realities.

If the past DeFi era was about protocols, Hyperliquid signals DeFi’s move toward the market. It’s not the endpoint, but it could be a turning point.