Wall Street Races onto the Chain: Why Are Markets and Investors Playing Dead? Bitwise CIO: The Knowledge Gap Is the Biggest Alpha

Whenever Anthropic releases a new tool, related industry stocks plummet—fueling a market-wide panic that “AI will destroy the world.” But the well-known financial media The Kobeissi Letter offers a very different perspective: the process of AI lowering cognitive costs is not a sign of economic collapse but a necessary step toward an era of “bountiful GDP.” This article is based on a tweet from The Kobeissi Letter, edited and translated by Dongqu.

(Background recap: The end of antivirus software? Claude AI uncovers 500 zero-day vulnerabilities, frightening Wall Street; CrowdStrike plunges 18.)

(Additional context: How is AI filling the world with bubbles?)

Table of Contents

Toggle

- Anthropic’s “Massacre”: The Panic Is Real

- Commoditization of Cognition ≠ Economic Collapse

- Investors are selling the “Layoff Story,” but the real big news is service price compression

- “Ghost GDP” vs. “Abundant GDP”

- White-collar employment impact: Reasonable concern, but not inevitable

- The endgame of SaaS is not disappearance but transformation

- Agentic Commerce: Friction decreases, transaction volume increases

- Productivity data is already speaking

- The most underestimated scenario: AI abundance ends war

- Conclusion: Transformation ≠ Collapse

The stock market just wiped out $800 billion in market value because the idea that “AI will take over everything” has become a consensus view. But this perspective is overly “obvious”—and “obvious” trades never truly win.

This doomsday narrative is so popular because it hits a primal fear. It depicts AI as a macroeconomic destabilizer capable of triggering a chain reaction of negative domino effects: layoffs hurt consumption, shrinking demand forces companies to automate further, automation accelerates layoffs.

The undeniable fact is: AI is not just another software upgrade or efficiency tool. It’s a general capability disruption that touches every white-collar workflow. Unlike any previous technological revolution, AI is “simultaneously” becoming proficient at everything.

But what if this doomsday scenario is wrong? It rests on three assumptions: demand is fixed, productivity gains won’t expand the market, and the system’s adaptation speed can’t keep up with disruption.

Anthropic’s “Massacre”: The Panic Is Real

First, the conclusion: we cannot ignore what’s happening in the market. Anthropic’s impact through Claude is shaking the entire industry, causing hundreds of billions of dollars in market cap to evaporate.

This is a recurring scene in 2026: Anthropic releases a new AI tool, Claude makes substantial breakthroughs in programming and workflow automation, and within hours, affected sectors’ stocks crash.

Here are some examples:

Immediate stock reactions to Claude announcements

IBM ($IBM) suffered its worst decline since October 2000 after Anthropic announced Claude can simplify COBOL code. Adobe ($ADBE) has already fallen 30% this year, as generative AI compresses the value of creative workflows. The cybersecurity sector collapsed across the board after the release of “Claude Code Security.”

CrowdStrike ($CRWD) nearly lost $20 billion in market value within a minute of Claude launching “Claude Code Security.” On February 20, at 1 p.m. Eastern, Claude released an AI tool that automatically scans code for vulnerabilities, and just two trading days later, CrowdStrike’s market cap shrank by $20 billion.

These reactions are not irrational. The market is trying to price in the immediate profit compression. When AI can replicate a worker’s output, pricing power shifts from sellers to buyers. This is the first-order impact—and it’s real.

Commoditization of Cognition ≠ Economic Collapse

But commoditization does not equal collapse; it’s a way to lower costs and expand access. Personal computers commodified computation, the internet commodified distribution channels, cloud computing commodified infrastructure, and AI is commodifying “cognition.”

Undoubtedly, some traditional workflows will face profit compression. The key question is: will the decline in cognitive costs lead to economic collapse or to rapid economic expansion?

The pessimistic cycle constructs a simplified linear model: stronger AI → layoffs and wage cuts → reduced consumer spending → further automation by companies to maintain profits → repeat. This model assumes a static economy.

History shows otherwise. When the cost of producing something drops sharply, demand rarely stays the same—it expands. When computing costs fall, we don’t consume the same amount of power at lower prices; we consume orders of magnitude more and build entirely new industries on that basis.

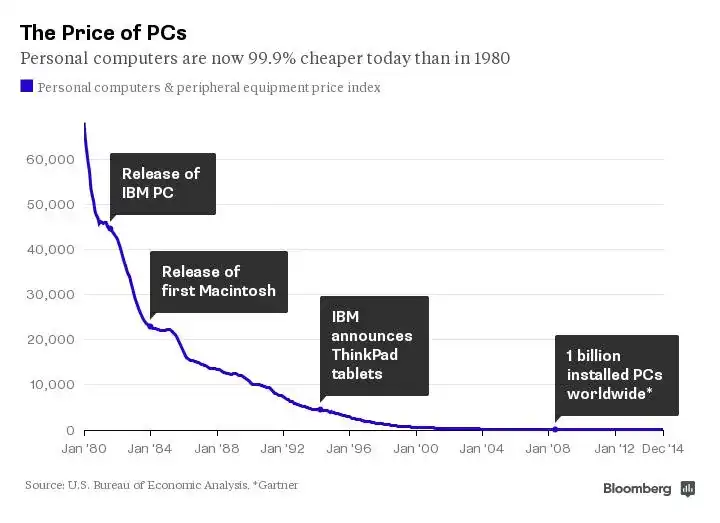

Today, personal computer prices are 99.9% cheaper than in 1980:

AI is lowering costs across industries. When service prices fall, regardless of wage growth, consumer purchasing power increases.

Only if AI replaces labor without genuinely expanding demand will the doomsday cycle hold. If cheap computing and productivity spur new consumption scenarios and economic activities, optimistic outcomes emerge.

Investors are selling the “Layoff Story,” but the real big news is service price compression

Investors tend to promote the “obvious” layoff narrative, but the bigger story is the compression of service prices. The reason knowledge-based work is expensive is because of its scarcity. Once knowledge supply becomes abundant, the price of knowledge work naturally declines.

Think about healthcare administration, legal documents, tax filing, compliance checks, marketing production, basic programming, customer service, and education. These services consume significant economic resources mainly because they require trained human attention. AI is lowering the marginal cost of this attention.

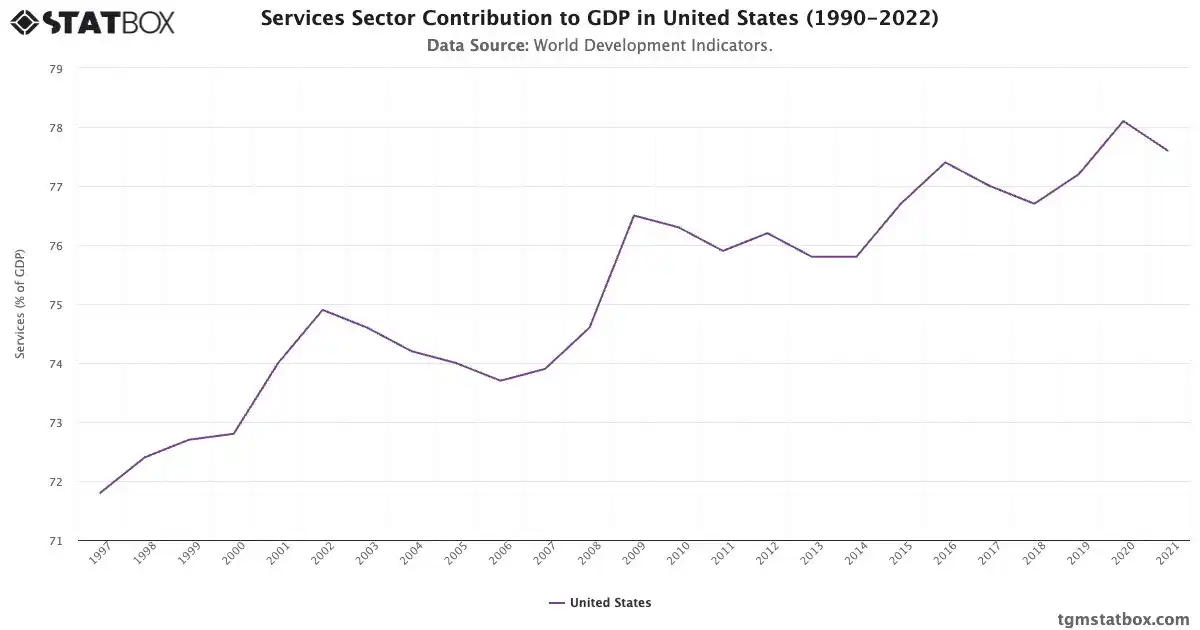

In fact, the US service sector contributes nearly 80% of GDP:

If operating costs decline, small businesses can survive more easily; if the cost of accessing services drops, more households can participate in the economy. To some extent, AI’s progress is akin to an “invisible tax cut.”

Businesses that rely on high-cost cognitive labor may suffer, but the broader economy will benefit from lower service inflation and higher real purchasing power.

“Ghost GDP” vs. “Abundant GDP”

Pessimists rely on “Ghost GDP”—appearing impressive on paper but not truly improving household living standards. Optimists prefer “Abundant GDP”—growth in output coupled with falling living costs.

Abundant GDP doesn’t require nominal income to soar; it depends on prices falling faster than incomes. If AI significantly lowers the costs of essential services, even if household wages slow, real income will still increase. Productivity gains are not disappearing—they’re transmitted through lower prices.

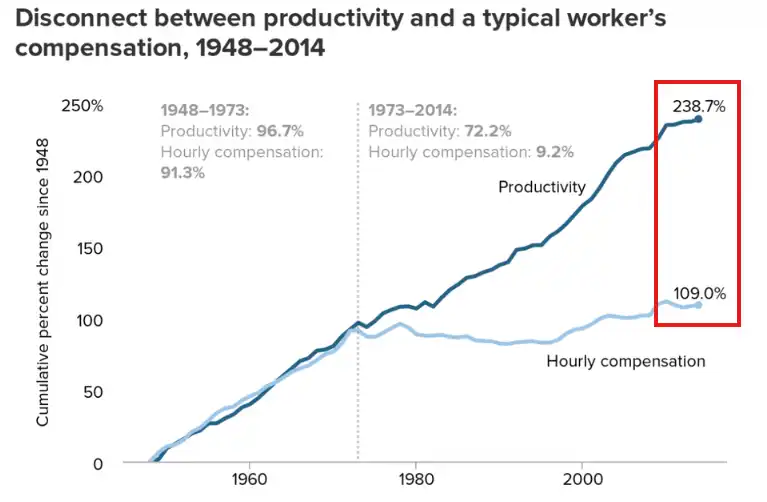

This may explain why productivity has consistently outpaced wage growth over the past 70+ years:

The internet, electricity, mass manufacturing, and antibiotics all provided new ways to expand output and lower costs, despite being disruptive and volatile. But in retrospect, these transformations permanently raised living standards.

A society that wastes less time navigating complex systems and paying for redundant services will be functionally wealthier.

White-collar employment impact: Reasonable concern, but not inevitable

A core worry is that AI will disproportionately impact white-collar jobs, which drive non-essential consumption and housing demand. This is a reasonable concern, especially given the stark wealth gap.

However, AI still has clear limitations in physical dexterity and in areas involving human identity and social roles. Skilled trades, hands-on healthcare, advanced manufacturing, and experience-driven industries still have structural demand. In many cases, AI acts as an assistant rather than a replacement.

More importantly, AI lowers the barriers to entrepreneurship. When individuals can automate accounting, marketing, customer service, and programming tasks, starting small businesses becomes much easier. Removing entry barriers with AI might be a solution to current income inequality.

The internet eliminated some jobs but created new ones. AI is likely to follow a similar trajectory—reducing some white-collar roles while expanding autonomous economic participation in other areas.

SaaS’s endgame is not disappearance but transformation

AI clearly pressures traditional SaaS (Software as a Service) business models. procurement teams’ bargaining power increases, and some long-tail software products face structural resistance. But SaaS is just a delivery mechanism, not the end of value creation.

Next-generation software will be adaptive, agent-driven, results-oriented, and deeply integrated. Winners won’t be static tool providers but those best able to adapt to change.

A certain degree of profit compression does not mean the entire digital economy is collapsing; it signals a transition.

Agentic Commerce: Friction decreases, transaction volume increases

Pessimists believe that agentic commerce will destroy middlemen and fee-based revenue. To some extent, that’s true—reduced friction makes fee extraction more difficult.

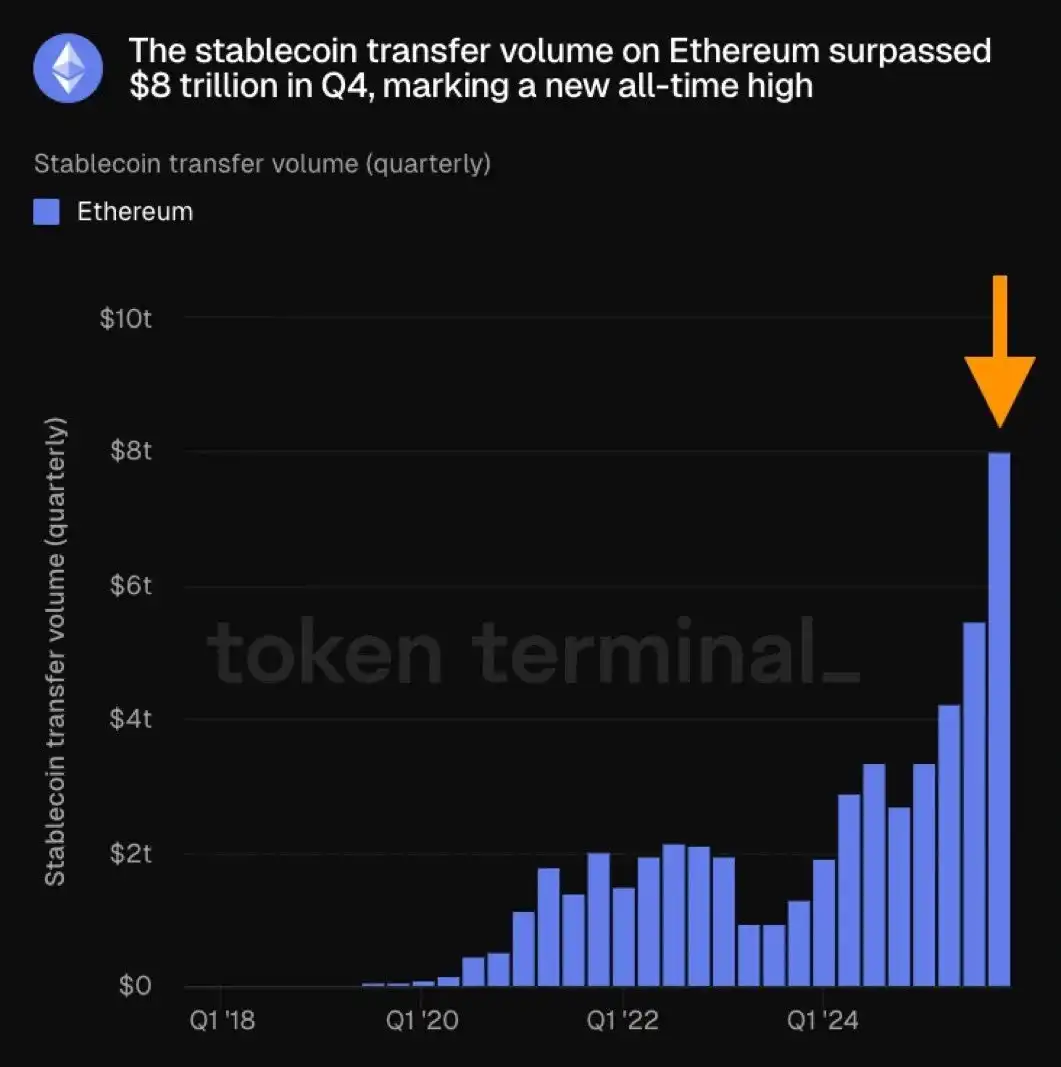

Even before AI looked like today, stablecoin trading volume had already surged. Why? Because markets always favor efficiency.

But lower systemic friction also amplifies total transaction volume. When prices improve and transaction costs fall, more economic activity occurs—this is a bullish signal.

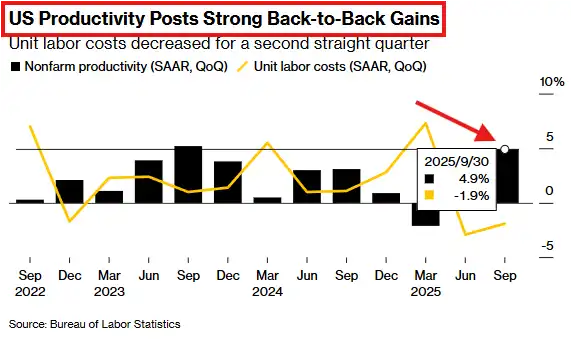

Productivity data is already speaking

The ultimate arbiter of optimism is productivity. If AI can sustain continuous productivity improvements in healthcare, government, logistics, manufacturing, and energy, the result will be widespread abundance and lower entry barriers.

Even just 1-2% incremental productivity growth over time, compounded over ten years, is remarkable.

In Q3 2025, US labor productivity accelerated to its strongest pace in two years:

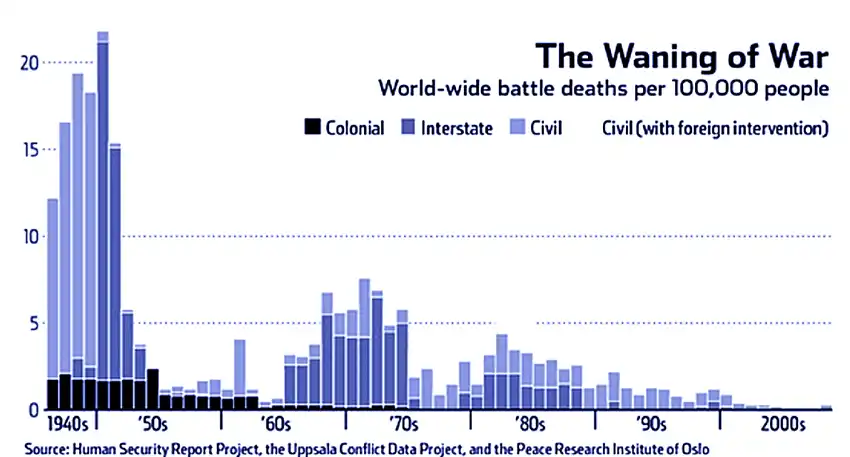

The most underestimated scenario: AI abundance ends war

One of the least discussed impacts of AI-driven abundance is geopolitics. Most wars in history have been fought over scarce resources: energy, food, trade routes, industrial capacity, labor, and technology. When resources are limited and growth feels zero-sum, conflicts arise.

But abundance changes everything. If AI significantly lowers the costs of energy, manufacturing, logistics, and services, the global economic pie expands. When productivity rises and marginal costs fall, reliance on resource conquest diminishes.

Tariffs are tools in resource-scarce worlds to protect domestic industries. But if AI causes production costs worldwide to plummet, protectionism becomes economically inefficient. History shows that periods of technological acceleration tend to reduce global conflict—post-WWII industrial expansion decreased the motivation for major powers to confront each other directly.

The most optimistic AI outcome isn’t just higher productivity or stock indices—it’s a world where economic growth is no longer a zero-sum game.

Conclusion: Transformation ≠ Collapse

AI amplifies outcomes. If institutions cannot adapt, it will magnify vulnerabilities; if productivity outpaces disruption, it will magnify prosperity.

The industry “massacre” triggered by Anthropic signals that workflows are being re-priced and cognitive labor is becoming cheaper—an unmistakable sign of transformation. But transformation does not mean collapse, just as every major technological revolution initially appears destabilizing.

The currently underestimated possibility isn’t utopia but “abundance.” AI may compress rents, reduce friction, and reorganize labor markets, but it could also bring the largest real productivity expansion in history.

The difference between a “global intelligence crisis” and “global intelligence prosperity” isn’t capability but adaptation. And this world always finds a way to adapt.