Why does the market still "doze off" after NVIDIA's earnings report?

The “Super Bowl” of earnings season has just concluded. NVIDIA (NVDA) delivered a results report in line with expectations, but its stock price after hours seemed stuck at the key psychological level of $200, unable to break above or below. Meanwhile, the VIX index (also known as the “fear index”), which measures market panic sentiment, showed a much lower one-day volatility (VIX 1-day) increase after the earnings release than many traders anticipated, and it then plummeted sharply to around 9 at the open. It felt like a highly anticipated concert where the lead singer performed steadily, but the audience was unusually quiet, even yawning.

Behind this calm, there may be an important shift in market structure brewing. Once the most significant “boot” drops, the focus of the market is shifting from extreme individual stock performance to a more macro, and perhaps more boring, theme: “Dispersion Unwind.”

The “Buy the expectations, sell the facts” options dilemma

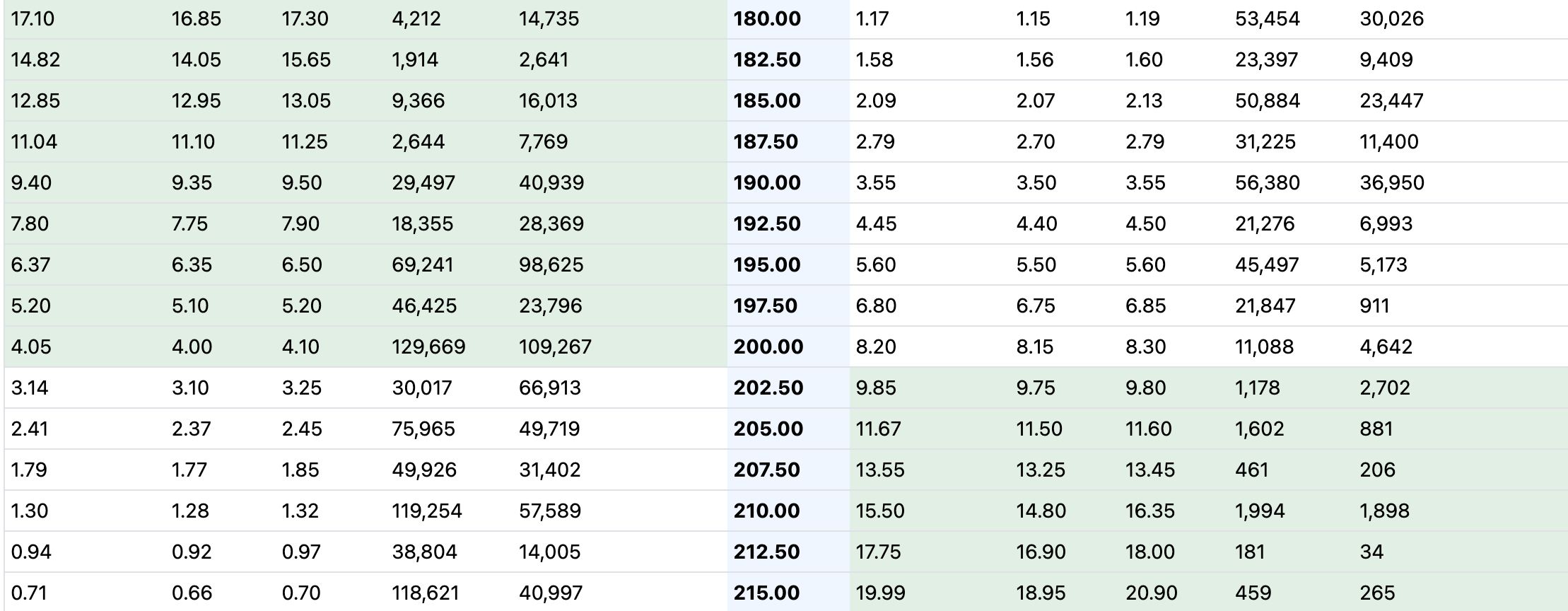

First, let’s look at NVIDIA itself. Before the earnings, market sentiment was extremely bullish, with the options market especially active. Large sums of money were betting that the stock would break through the $200–$205 range after the report. However, the reality was sobering. After earnings, the stock hovered around $200, causing the value of many out-of-the-money options (especially $200 and $195 call options) to rapidly evaporate.

I recall during a tech earnings season in 2023, a similar scenario occurred. A star company beat expectations but its stock opened high and then declined, due to the opposite effect of gamma squeeze—when the stock failed to break key strike prices, market makers hedging their positions sold aggressively, further pushing the stock down. The options chain for NVIDIA this time resembles that situation. When the most optimistic expectations are not met, the options market shifts from a “catalyst” to a “speed bump.”

The market’s “intermission” after the “big show”: Dispersion Unwind takes the stage

Why does the market seem somewhat “boring” after NVIDIA’s earnings? This may be because the main driver of the market in recent times—extreme divergence among individual stocks—is approaching a turning point.

Dispersion, simply put, is the difference between individual stock volatility and the overall market volatility. During the AI frenzy, we saw a few giants like NVIDIA and AMD soaring ahead with high volatility, while many other stocks performed modestly. This high dispersion environment is a playground for active stock pickers and quantitative hedge funds. However, such a state cannot last forever.

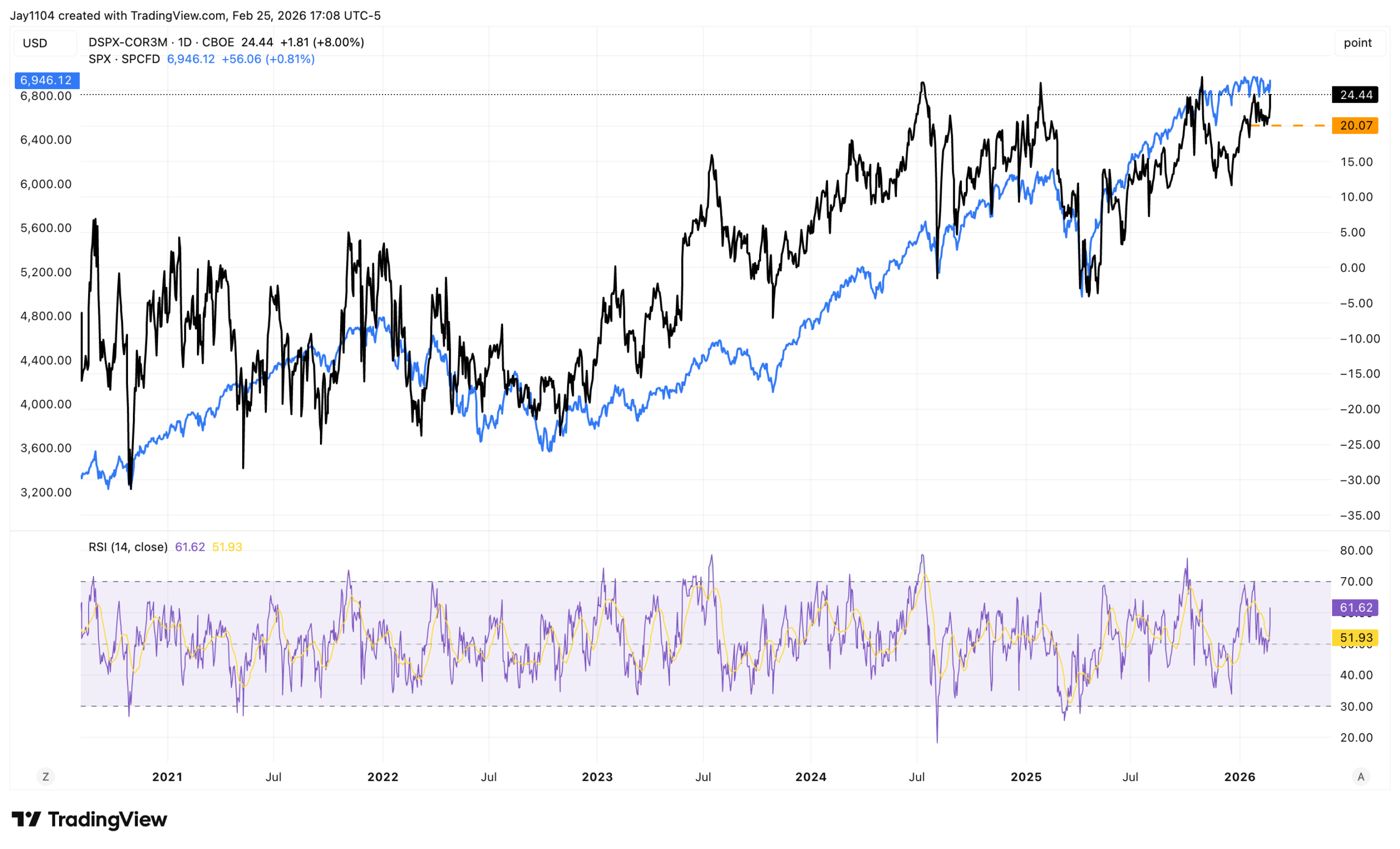

A key indicator to watch now is the three-month dispersion and the correlation spread (DSPX-COR3M). When this spread is high, it indicates significant stock divergence (high dispersion) and low correlation among stocks. Historical experience suggests this state tends to revert to the mean. In other words, implied volatilities of individual stocks will gradually align with the market index’s volatility, leading to a decrease in dispersion and an increase in correlation among stocks.

To put it plainly: “Star solo acts” may need to pause temporarily, making way for a “collective chorus.” If dispersion begins to converge, then the trading strategies that profited from long positions in strong AI stocks and short positions in weak stocks over the past few months could face deteriorating conditions. Capital might reassess sector rotations or shift back toward macro beta (overall market movement) trading.

The subtle “background noise”: Massive US Treasury settlements

While the market contemplates a style shift, a technical factor is quietly humming in the background—settlements of large US Treasury holdings.

According to the scheduled settlement dates, about $137 billion in Treasuries will settle in the coming trading days (including $22 billion on the earnings day, $37 billion the next day, etc.). Although these large fund transfers do not directly mean money flowing out of stocks, they can impact short-term liquidity in the financial system and potentially increase short-term volatility. It’s like a swimming pool where water is simultaneously being drained and refilled—calm on the surface, but turbulent underneath.

I recall during last year’s quarter-end “rebalancing week,” similar liquidity disturbances occurred. Even without negative fundamentals, the market experienced several days of quiet sell-offs at the close, largely due to institutional rebalancing and bond settlements. For short-term traders, these dates are calendar risks worth paying extra attention to.

What’s next for the market?

Overall, NVIDIA’s earnings may mark a temporary pause in a micro-driven momentum. The market needs a new catalyst. Potential sources include:

- Further clarity on macro policies: The monetary policy paths of major global central banks, especially the Federal Reserve, will become focal points. Any hints about the timing and pace of rate cuts could trigger a re-pricing of market styles.

- Earnings broadening validation: The AI narrative cannot rely solely on NVIDIA. The market needs more companies—whether tech giants or traditional industries—to demonstrate tangible AI capital expenditures and revenue contributions during earnings calls, confirming the breadth and depth of this wave.

- Self-fulfilling dispersion convergence: As more investors anticipate and trade “dispersion convergence,” the process may accelerate. Funds could withdraw from crowded AI stocks to seek other valuation opportunities, prompting a healthy sector rotation.

For investors, current strategies may need adjustment. Chasing high-priced, options-crowded star stocks carries changing risk-reward dynamics. Instead, focus on two areas: first, sectors that could benefit from dispersion convergence (e.g., cyclicals or financials that are more sensitive to macro trends and have lagged); second, monitor overall market volatility. If the VIX remains low, it might be a good time to buy some “insurance” (like index puts) for your portfolio.

Markets never stay euphoric forever. The current “calm period” is an opportunity to observe capital flows and adjust positions. After all, when the choir starts tuning, the next song isn’t far behind. Of course, all judgments should be made in real-time, staying flexible amid liquidity shifts and style rotations.