Truth Unveiled: ETF Mechanism Suppresses Price Discovery, Jane Street Becomes the Scapegoat for Bitcoin's "10-Point Dump"

Author: Jae, PANews

Conspiracy theories often spread more easily than the truth, and this is true in the crypto world as well. Especially during periods of sideways price movement and market anxiety. When Bitcoin repeatedly struggles below $70,000, and every US stock trading day encounters strange selling pressure at 10 a.m., investors can’t help but suspect a mysterious hand manipulating the market.

As Jane Street becomes entangled in legal disputes with Terraform Labs and faces severe accusations in the crypto market, a fascinating phenomenon occurs: the precise “10 a.m. dump” scene, as accurate as a clock, mysteriously disappears. This New York-based quantitative trading giant, known for its low-profile approach and high-frequency algorithms, happens to be an authorized participant (AP) in top Bitcoin spot ETFs like BlackRock and Fidelity.

On social media, Jane Street has been identified as the culprit hiding behind algorithms, allegedly pressing the “sell button” every day on schedule. Through systematic analysis, PANews finds that Jane Street is not the true culprit behind Bitcoin’s price decline, but it has indeed become a projection target for market anxiety—a powerful, mysterious, and suitable scapegoat to play the “villain.”

Social media stokes the fire, accusing Jane Street of being the mastermind behind the “10 a.m. dump.”

The story begins with a very ordinary observation. Since November 2025, sharp traders have noticed that around 10 a.m. Eastern Time, shortly after US stock markets open, Bitcoin spot ETFs always face a wave of large sell-offs. This phenomenon is colloquially called the “10 a.m. dump strategy.”

However, this is not just a normal correction. The sell-offs usually flood in within half an hour after opening, quickly breaching the market’s liquidity depth, triggering a series of leveraged long liquidations. Prices panic to intraday lows, then gradually stabilize. This highly consistent “timestamp” hints at algorithmic involvement.

Milk Road points out that the underlying logic of this operation is exploiting the thin liquidity early in US stock market open to create a price crash, thereby reducing the cost of subsequent accumulation. In traditional finance, this behavior is called “quote stuffing” or “price manipulation,” aiming to profit from structural market fragility.

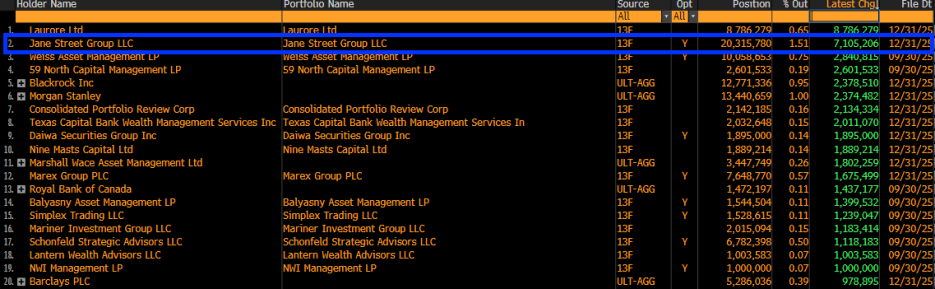

Fuel for conspiracy theories was further ignited in February 2026. Jane Street’s 13F filings showed a significant increase in holdings of BlackRock’s Bitcoin spot ETF (IBIT), adding over 7.1 million shares in Q4 2025, totaling 20.315 million shares worth about $790 million.

Once the data was released, social media exploded: since Jane Street is accumulating Bitcoin on a large scale, isn’t the 10 a.m. dump just to lower the cost of building positions? A logical chain emerges: motive (accumulation) + method (algorithm) = the culprit (Jane Street). However, Frontier Investments CEO Louis LaValle poured cold water: viewing the 13F disclosure as mere “long accumulation” is a fundamental misunderstanding of market-making business models.

As a primary market maker and AP for IBIT, Jane Street’s ETF holdings are more likely to be for balancing its options positions or executing hedging strategies, rather than a one-sided bet.

Disappearing strategies amid legal storms and regulatory spillovers: the impact of regulatory pressure on sell algorithms

If the 13F data only caused market misinterpretation, the subsequent phenomena add empirical weight to the debate. On February 24, Terraform Labs’ liquidator Todd Snyder filed a lawsuit accusing Jane Street of using a private communication channel with Terraform insiders (former intern Bryce Pratt) to precisely liquidate positions hours before the Terra ecosystem collapse in May 2022, allegedly involving insider trading and market manipulation.

Almost simultaneously, Jane Street faced allegations from India’s Securities and Exchange Board (SEBI) for manipulating the BANKNIFTY index, resulting in a $550 million fine. The spotlight of law suddenly shone brightly.

Remarkably, after the lawsuit became public, the regular morning 10 a.m. selling pressure significantly eased or even disappeared. This is hard to attribute to mere coincidence.

PANews believes that in financial engineering, when trading strategies are widely recognized or questioned by regulators, their profit margins (alpha) tend to diminish rapidly. Increased regulatory risk forces algorithms to self-restrain, shifting from “aggressive profit pursuit” to “compliance and risk avoidance,” which may directly lead to the breakdown of certain dump patterns.

The disappearance of the “10 a.m. dump” phenomenon confirms its existence and its close relationship with regulatory pressure. But does this prove it was Jane Street’s “exclusive strategy”? The answer remains ambiguous, but one thing is certain: when regulators scrutinize market makers’ internal operations, certain gray-area trading behaviors are forced to cease under compliance pressures.

The 10 a.m. dump contradicts market-making logic, making conspiracy theories less plausible

Although the community tends to blame price drops on a single malicious entity, conspiracy theories claiming Jane Street “deliberately suppresses Bitcoin prices” are considered untenable by opponents.

Keone Hon, former quant at Jump Trading, and Julio Moreno, head of research at CryptoQuant, provided strong technical rebuttals. Keone Hon pointed out that shorting IBIT alone cannot easily push Bitcoin prices down. While IBIT’s trading price is anchored to Bitcoin, it is fundamentally a secondary market stock. If IBIT trades at a significant discount, APs and arbitrageurs will quickly step in, buying low and redeeming Bitcoin in the primary market to arbitrage away the spread. This arbitrage mechanism prevents IBIT from decoupling from the spot price downward.

Julio Moreno believes that Jane Street’s operations are similar to any “delta-neutral” fund. “Real large market makers do not bet on direction,” said Xin Song, CEO of GSR Markets, a leading crypto market maker, in an interview with PANews.

Indeed, for market makers like Jane Street, taking directional risk is extremely dangerous. They pursue a “net risk exposure of zero” balance. When providing liquidity as an AP for IBIT, they face ongoing inventory risk. If clients buy large amounts of IBIT, Jane Street, as the seller, needs to hold a short position. To hedge this, they typically buy equivalent Bitcoin in spot or futures markets—this process is called “dynamic hedging.”

In this model, Jane Street’s profit does not come from price increases or decreases but from:

- Bid-ask spread: earning profit from buying slightly below and selling slightly above market prices;

- Funding rate arbitrage: buying ETF spot and simultaneously selling futures contracts on CME or other exchanges to lock in riskless basis gains (basis trade).

Although both strategies involve substantial selling, they are offset by equivalent buying, making the net market impact theoretically neutral.

Macro analyst Alex Krüger also presented data refuting this: since January 1, IBIT’s cumulative return from 10 a.m. to 10:30 a.m. Eastern Time has been 0.9%.

PANews believes that from a quantitative perspective, the “10 a.m. dump” is more likely triggered by the surge in hedging demand caused by opening volatility in the US stock market. Since IBIT’s liquidity is in a restructuring phase early in the market open, this hedging activity is amplified into price manipulation.

In reality, giants like Jane Street have enormous balance sheets. If Bitcoin prices collapse due to their manipulation, their own holdings of billions of dollars in related assets and derivatives would also face extreme liquidity and counterparty risks.

Structural issues in Bitcoin spot ETF price discovery

While technical skeptics dismiss conspiracy theories, Jeff Park, CIO of ProCap, argues that the root problem lies in the current AP mechanism of Bitcoin spot ETFs.

The key to AP’s significant influence on prices is its special legal status. Under SEC regulation, institutions like Jane Street enjoy privileges that ordinary traders do not:

- Exemption from short-selling restrictions: APs often are not bound by standard securities short-sale limits when performing market-making tasks. This means they can sell ETF shares without borrowing the underlying Bitcoin, using Bitcoin futures for hedging instead of buying spot Bitcoin;

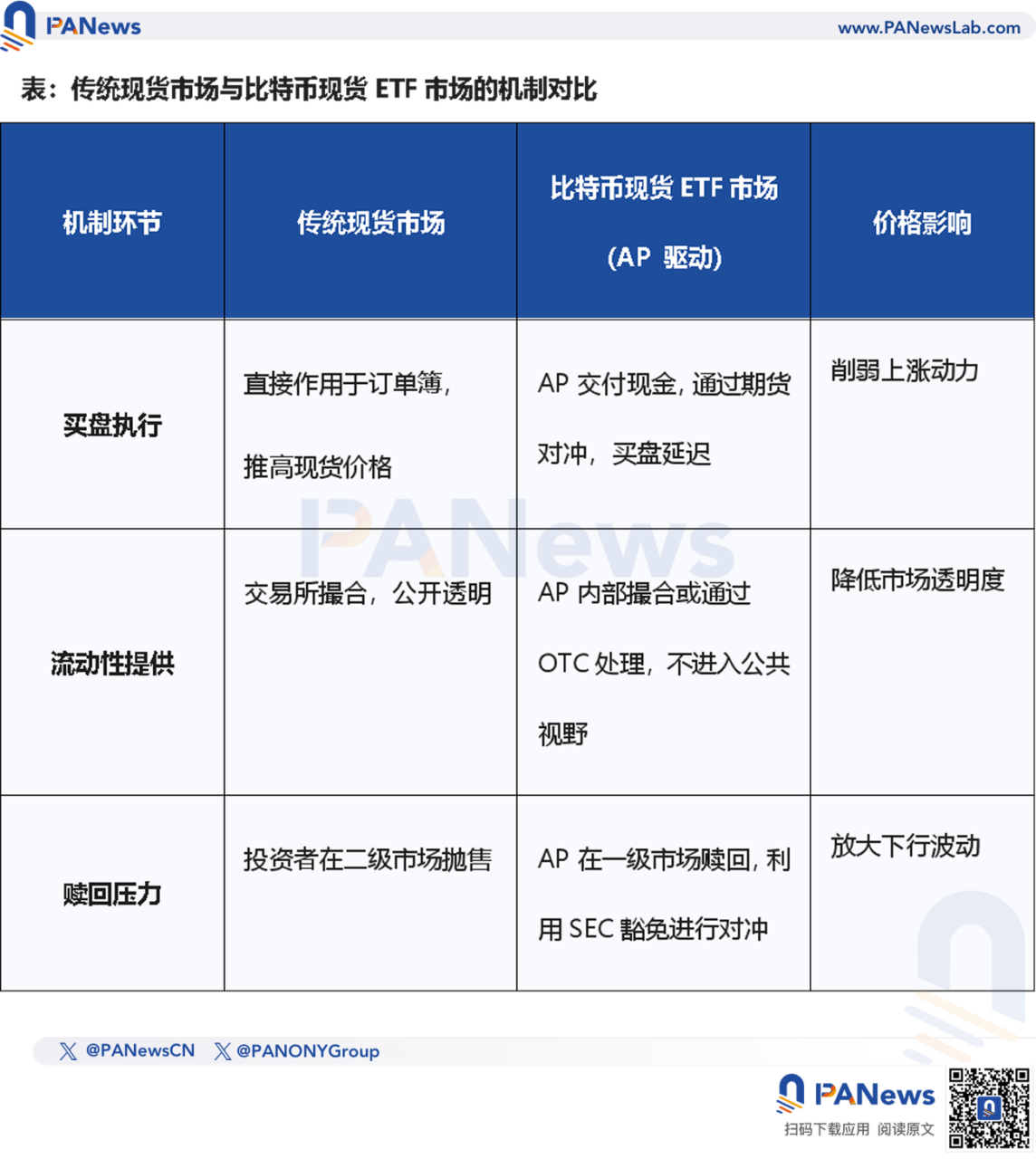

- Cash creation/redemption mode: Most Bitcoin spot ETFs currently adopt a “cash creation/redemption” process, quite different from traditional “physical” models (like gold ETFs).

Jeff Park further points out that the AP mechanism may be weakening Bitcoin’s price discovery function. The deeper issue is the “cash” mode itself. Bitcoin held by APs spends very little time in circulation; most of the time, it is “locked” in custodians’ cold wallets. PANews believes that this “lock-up” reduces circulating supply but also disconnects the ETF from the spot market.

Ideally, ETF demand should directly translate into spot market activity. But due to the presence of APs, this transmission is intermediated. APs often hedge risk through futures rather than direct spot purchases.

The result is that even if ETF inflows appear substantial, the actual buying in the spot market does not necessarily reflect this.

PANews believes that when APs like Jane Street use short-selling exemptions and hedge via futures, they are essentially creating a “synthetic” demand for Bitcoin. This can lead to ETF capital inflows that do not proportionally drive up the spot price, creating a “flexible suppression” effect on prices.

This structural mismatch results in a paradox: the larger the ETF, the more concentrated the Bitcoin price discovery power becomes among a few APs. Jane Street is one of the central nodes in this power structure.

Quantitative industry as a market ceiling?

“Quantitative never dies, and declines never stop.” The idea that “quantitative industry suppresses A-shares’ rise” is widespread on social media, even with hedge funds like Fantasia, behind DeepSeek, being accused of using advanced AI models to “glorify the country” while allegedly employing “dimensionality reduction” algorithms to harvest liquidity in secondary markets. But these claims are mostly emotional venting.

A profound question is posed: Is quantitative investing an “evolution of market civilization,” or an “invisible suppressor” of healthy stock market growth?

Today, algorithmic trading (including high-frequency trading, algorithm execution, and quantitative hedging) accounts for over 70% of US stock market volume. In contrast, the slightly less mature A-shares market has seen quantitative penetration grow from about 5% to 25–30% over the past decade.

Even more surprising are the results from top quant funds.

Contrary to common perception, even as quantitative trading share and top institutions’ returns increase year by year, the S&P 500 has gained about 260% over the past decade, while the Shanghai and Shenzhen 300 Index has only risen approximately 60%.

This shows that the growth of quant firms does not necessarily come at the expense of stock market health.

Rather than quant suppression of market rallies, it has profoundly changed the pace of wealth distribution. In the US, quant strategies have undergone industrialization; in A-shares, they may still be in a painful transition; and in crypto markets, quant giants are reconstructing pricing power through structural tools like ETF AP mechanisms.

The so-called “suppression feeling” is essentially a sense of powerlessness of traditional investment methods faced with high-frequency algorithms and complex financial engineering. Quantitative strategies will not disappear; they will become part of the market’s breathing.

For crypto players, instead of searching for a “villain,” it’s better to track the evolution of ETF mechanisms. Understanding how this “Wall Street-created money machine” operates is a must for every investor.

Conspiracy theories are always more viral than the truth because they are simple, direct, and emotionally appealing. But real markets are far more complex and often more boring.

Perhaps the real enemy is not a specific institution but our neglect of complex mechanisms and our craving for simple answers.