Second Hong Kong IPO Attempt After Prior Filing Lapse

Wuhan Aimeison Life Sciences Co., Ltd., a Chinese early cancer screening company, has resubmitted its prospectus to the Hong Kong Stock Exchange for main board listing, with China Bohai Bank International and Shanghai Pudong Development Bank International as joint sponsors. This filing follows the lapse of the company’s initial submission on September 28, 2025. If successful, Aimeison would become Hong Kong’s first publicly listed company focused on methylation-based cancer early screening.

Aimeison was founded in January 2015 by Dr. Zhang Lianglu and specializes in early detection of high-incidence, high-mortality cancers using methylation-based technology. The company has developed two core marketed products: Aixingan for liver cancer detection and Aiguangle for urothelial cancer detection, along with four candidate products in development. Aixingan is the world’s first liver cancer detection reagent using methylation technology with real-time quantitative PCR (qPCR). Aiguangle requires only 1 milliliter of urine sample for non-invasive urothelial cancer detection. As of end-2025, the company’s R&D team comprises 40 people, with 65% holding bachelor’s degrees or higher, and holds 81 registered Chinese patents including 59 invention patents.

A Decade of Losses Despite Revenue Growth

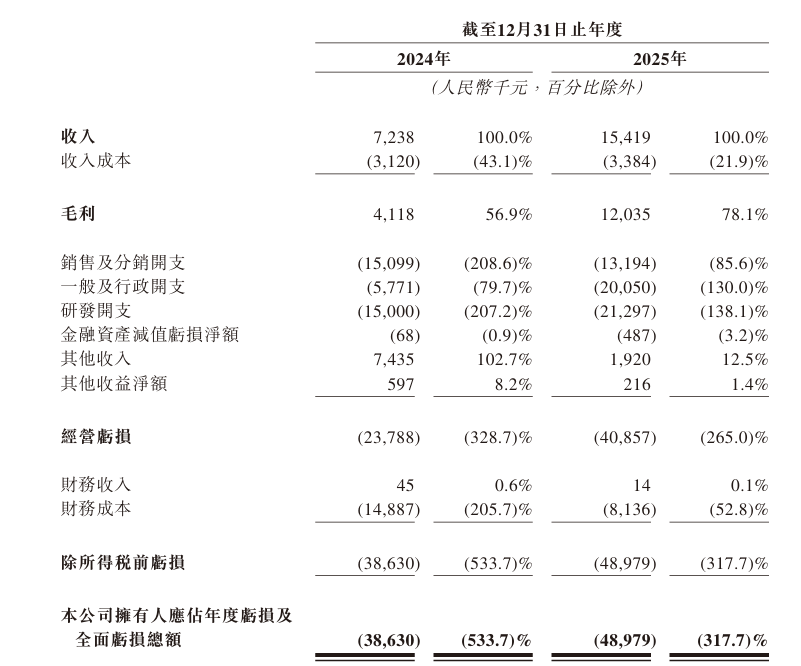

Despite product development efforts, Aimeison remains unprofitable. In the reporting periods of 2024 and 2025, the company generated revenue of approximately 7.238 million yuan and 15.419 million yuan respectively, representing 113% year-over-year growth. However, net losses reached 38.63 million yuan and 48.98 million yuan respectively, with cumulative losses of 87.61 million yuan over two years. Gross profit was 4.118 million yuan and 12.035 million yuan respectively.

The company attributes continued losses to its early-stage development phase, stating in the prospectus that operations have focused on business planning, fundraising, preclinical trials, and clinical trials since registration. While the company expects improved financial performance as it commercializes additional product pipelines, it has explicitly stated that it anticipates generating losses in 2026 despite higher expenses and stock-based compensation. Although net asset value turned positive to 26.945 million yuan by end-2025, the company’s cash flow remains highly dependent on external financing, indicating weak risk resistance.

R&D Spending Far Exceeds Revenue

As a technology-driven biotech company, Aimeison invests substantial resources in research and development. R&D spending as a percentage of revenue reached 207.2% in 2024 and 138.1% in 2025. The company’s future profitability is heavily tied to successful development, regulatory approval, and commercialization of candidate products.

In its prospectus risk disclosures, Aimeison emphasizes that most candidate products remain in design or clinical development stages, and the company has invested the majority of its time and financial resources into developing and commercializing these products. The company explicitly warns that it may be unable to complete clinical trials in a timely manner at acceptable costs or may be unable to complete them at all. Additionally, successful preclinical research and early clinical trials do not guarantee that subsequent clinical trials will produce similar results or ultimately obtain regulatory approval.

High Customer Concentration and Related-Party Dependency

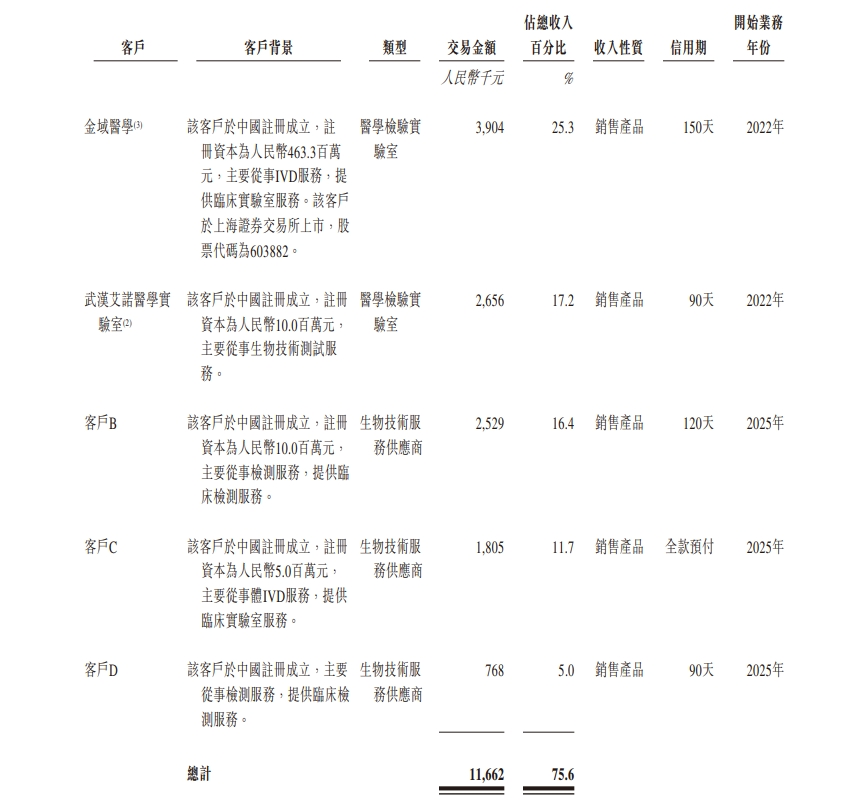

Customer concentration presents a significant challenge. In 2024 and 2025, the company’s top five customers generated combined revenue of 5.3 million yuan and 11.7 million yuan respectively, representing 73.2% and 75.6% of total revenue. The largest customer in each year contributed 3.8 million yuan and 3.9 million yuan, representing 52.1% and 25.3% of revenue respectively.

Notably, founder Zhang Lianglu’s wholly-owned Wuhan Aino Medical Laboratory was the company’s largest customer in 2024, contributing 52.1% of revenue. This means approximately half of 2024 revenue came from the controlling shareholder’s laboratory. Third-party medical testing leader Jinyu Medical ranked second with 674,000 yuan in sales (9.3% of revenue). Jinyu Medical’s major shareholder Liang Yaoming serves as the actual controller of Aimeison shareholder Suzhou Jinghe. Additionally, shareholder Guangdong Kepai Biotechnology ranked third with 375,000 yuan in sales (5.2% of revenue).

These two related parties combined contributed revenue representing 57.3% of the total, demonstrating significant related-party transaction dependency.

In 2025, the top five customer structure shifted. Wuhan Aino Medical Laboratory dropped to second place with revenue share declining to 17.2%, replaced by a non-related third-party institution in the top position. Shareholder Guangdong Kepai Biotechnology remained in the top five, alongside third-party medical testing and physical examination institutions. Despite structural improvements, combined top five customer revenue still exceeded 75%, indicating that high customer concentration issues remain unresolved.

Aimeison emphasizes in its prospectus that it will likely continue to depend on a limited number of customers for the majority of revenue in the foreseeable future, with single-customer revenue proportions potentially increasing in certain circumstances. Loss of one or more major customers or any major customer reducing purchase volumes would significantly reduce revenue.

Market Opportunity Amid Regulatory Challenges

According to Frost & Sullivan data cited in the prospectus, in 2024, liver cancer incidence ranked fourth among all cancers in China while cancer-related mortality ranked second. Urothelial cancer is characterized by high recurrence rates. Early detection of these cancers can significantly improve patient survival rates while reducing medical costs associated with late-stage treatment. China’s tumor molecular detection market remains in early stages but is developing rapidly, growing from 4.3 billion yuan in 2019 to 8.7 billion yuan in 2024, representing a compound annual growth rate of 15.2%. The market is projected to reach 38.8 billion yuan by 2033, with a compound annual growth rate of 18.1% from 2024 to 2033.

However, Aimeison faces multiple challenges: a decade of unprofitability with expected 2026 losses, R&D spending substantially exceeding revenue, and significant clinical and regulatory approval risks.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.