SEC issued a statement on Wednesday, clarifying that tokenized securities are subject to federal securities laws. They are divided into two categories: issuer-led (recorded on-chain) and third-party-led (which may introduce bankruptcy risks). The SEC warns that blockchain is merely a record-keeping technology and cannot change the legal nature. The SEC favors broker custody over crypto self-custody.

Breakdown of the SEC Framework: Issuer-led vs. Third-party Tokenization

(Source: RWA.xyz)

The U.S. Securities and Exchange Commission’s Division of Corporation Finance, Division of Investment Management, and Division of Trading and Markets issued a staff statement on Wednesday stating that as tokenization moves from pilot projects to actual products, they are working to provide clearer guidance for market participants. The statement defines tokenized securities as instruments that fall within the scope of securities laws, presented in the form of crypto assets, with all or part of the ownership recorded via encrypted networks.

The staff divides the tokenization landscape into two main categories: issuer-led tokenization and third-party-led tokenization. In the issuer-led model, the company or its agent links on-chain transfers to its official shareholder records, effectively replacing traditional databases with on-chain record systems, while still bearing the same legal obligations related to issuance, sales, and reporting.

The report also describes a structure where tokens themselves do not carry underlying rights but serve as mechanisms that trigger updates to off-chain official ownership records. In this architecture, blockchain layers can assist in coordinating fund transfers, but security and legal enforceability are still determined by the issuer’s off-chain ledger. This design reveals a key fact: tokenization changes the form of stocks or bonds, not their legal nature.

The Two Main Tokenization Models Defined by the SEC

Issuer-led Model: The company uses on-chain records as official shareholder records, with blockchain replacing traditional databases, but securities law obligations remain unchanged.

Third-party-led Model: A company unrelated to the issuer creates crypto assets linked to others’ securities, potentially introducing additional risks such as bankruptcy.

The more complex third-party tokenization involves a company unrelated to the issuer creating crypto assets linked to others’ securities. The SEC staff notes that these models differ significantly and may introduce additional risks, including those related to the third party’s financial condition (e.g., bankruptcy), while the direct holders of the underlying securities may not face the same risks.

Regulatory Traps in Custody and Synthetic Models

The statement notes that regulators observe two common third-party approaches. One is custody tokenization, where the underlying securities are held by a custodian, and tokens represent rights or indirect interests. This model seems simple but introduces credit risk of the custodian. If the custodian goes bankrupt or misappropriates assets, token holders could face losses, whereas direct holders of the securities would not.

The other is synthetic tokenization, where tokens represent a third party’s own instruments that track the underlying securities, such as related securities or securities-based swaps, which have their own securities law implications. Regarding securities swaps, staff points out that providing services to persons who do not meet the contractual participant qualifications may trigger additional requirements, including registration and exchange trading conditions.

Reiterating, packaging risk exposure into tokens does not exempt them from long-term market rules. This is the core warning in the SEC statement: no matter how advanced the technology or how complex the structure, as long as the underlying assets are securities, securities laws must be followed. This “piercing” principle has long been established in traditional finance and is now explicitly applied to tokenized securities.

As this guidance is issued, some well-known institutions are testing how tokenized securities operate within regulatory frameworks. Last week, F/m Investments submitted an application to the SEC seeking approval to record ownership of its treasury bond ETF’s tokenized shares on a permitted blockchain. Meanwhile, asset managers and exchanges are seeking faster settlement and 24/7 functionality without violating existing investor protection measures.

The SEC staff describes the statement as a compliance roadmap, not a green light, and encourages companies to communicate with the agency when preparing registration, proposals, or action requests. This cautious attitude shows that while the SEC recognizes the technological value of tokenization, it will not relax regulatory standards because of it.

Broker Custody Over Native Crypto Self-Custody

The SEC outlined in December how tokenized securities exist within the U.S. market’s safeguards and favors broker-led custody rather than native crypto self-custody. It also approved the transfer of some stocks, bonds, and U.S. Treasuries to the blockchain via the Depository Trust & Clearing Corporation (DTCC).

This regulatory preference reveals the SEC’s distrust of native crypto custody models. Traditional broker custody is heavily regulated, with comprehensive investor protections and insurance schemes. In contrast, native crypto self-custody offers decentralization advantages but introduces risks like private key loss, hacking, and lacks the traditional financial compensation mechanisms.

“A clear framework like this is key to responsibly expanding tokenization,” said Securitize, a tokenization platform, in a Wednesday post on X. “We welcome the SEC’s thoughtful statement on tokenized securities, which recognizes that native, issuer-supported tokenization and on-chain recordkeeping are modern extensions of securities infrastructure.”

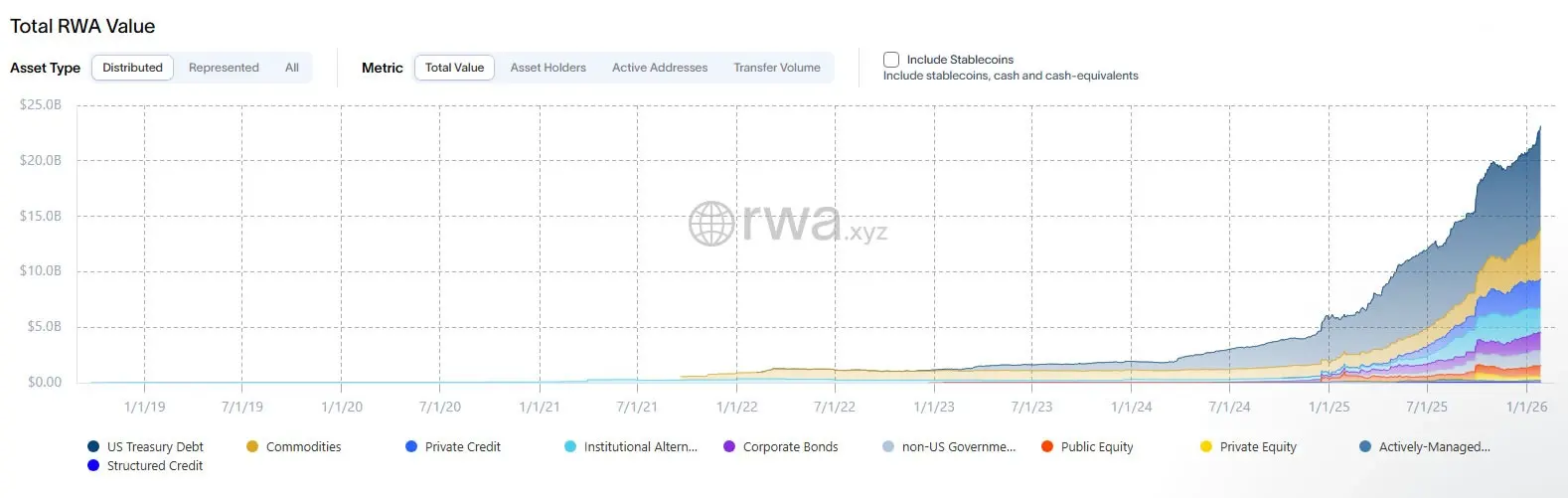

Over the past 12 months, the on-chain value of RWA tokenization has surged by 92%, indicating rapidly growing market demand for tokenized securities. However, this SEC statement sets clear regulatory boundaries for this fast-evolving field, ensuring that innovation does not come at the expense of investor protection.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.