SEC and CFTC compete for prediction market jurisdiction! Atkins: Still not classified as securities

SEC Chair Paul Atkins described prediction markets as a “huge issue” during a Senate Banking Committee hearing, citing “potential jurisdictional overlaps” currently primarily under CFTC authority but with both agencies working collaboratively. When asked whether clear rules are being developed, he responded “still watching” and stated “securities are securities, and the delineation of prediction markets and their products depends on specific language.”

“Huge Issue” Clarification: SEC Chair’s Regulatory Warning

(Source: The Block)

On Thursday, U.S. Securities and Exchange Commission Chair Paul Atkins told lawmakers that prediction markets are a “huge issue” of concern for regulators. During a Senate Banking Committee hearing, when asked about this rapidly evolving industry, Atkins said it is something he and CFTC Chair Michael Selig are both very focused on. “Prediction markets are precisely one of the areas where jurisdictional overlaps may exist,” Atkins said.

The phrase “huge issue” carries significant weight. In regulatory language, “issue” typically indicates an area requiring close attention and possibly enforcement action. “Huge” emphasizes the scale and urgency of the concern. Atkins’s choice of this strong wording sends a clear signal to the prediction market industry: do not assume a regulatory vacuum will last forever; strict regulation is imminent.

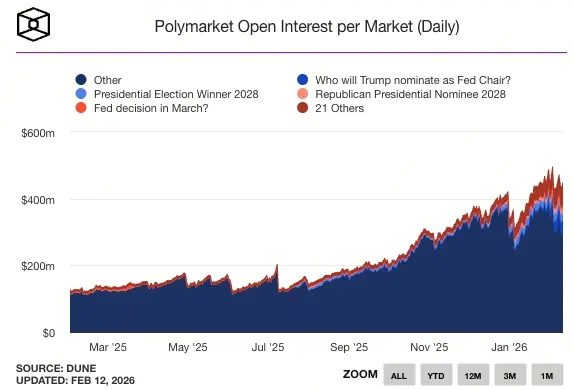

Over the past year, prediction markets including Kalshi and Polymarket have experienced explosive growth, especially after the 2024 U.S. election cycle. As CertiK reports, prediction markets grew from $15.8 billion in 2024 to $63.5 billion in 2025—quadrupling—transforming from fringe products into mainstream fintech. This rapid expansion naturally draws regulatory attention, as larger scale increases systemic risks and consumer protection issues.

How to regulate these markets, previously tightly restricted by the CFTC, has become a point of contention between state and federal authorities. Jurisdiction over prediction markets has become a key dispute between federal and state governments. Industry players argue that under the Commodity Exchange Act, all event contracts should fall under CFTC jurisdiction; some states, however, believe platforms involved in sports betting and other activities violate local gambling laws.

Atkins pointed out that most prediction markets tend to fall under CFTC jurisdiction, but both agencies will cooperate. When asked about the timeline for final rules, Atkins said “we’ll see.” This cautious response indicates that SEC and CFTC are still assessing how to divide jurisdiction and have not reached a final consensus. He added, “I believe we have sufficient authority. Securities are securities, regardless of their nature, and some nuances in defining prediction markets and products depend on wording.”

Three Core Issues in SEC vs CFTC Jurisdiction Dispute

Securities Definition: If prediction contracts meet the Howey Test (investment contract test), they may be considered securities under SEC jurisdiction.

Commodity Definition: The outcome of events (elections, sports) can be viewed as commodities, falling under CFTC regulation per the Commodity Exchange Act.

Gambling Definition: The distinction between skill and luck; if purely luck-based, platforms may be considered illegal gambling under state laws.

The statement “securities are securities, and the delineation of prediction markets and their products depends on specific language” reveals the complexity of regulation. For example, if a prediction contract is designed as “investment returns dependent on the organizer’s efforts,” it may be classified as a security. If it’s structured as a “derivative on commodity prices or event outcomes,” it could fall under CFTC. If it involves pure luck, it might be considered gambling. This legal reliance on precise wording creates significant uncertainty for prediction markets.

CFTC’s Defensive Stance: Developing Rules to Prevent Industry Outsourcing

CFTC Chair Selig stated on Bloomberg’s “Odd Lots” podcast Thursday that prediction markets are valuable and regulation is important. “We will certainly take on this task to ensure these markets don’t stagnate or move offshore, but rather that we develop the right rules and regulations to provide the best protections and ensure these markets thrive in the U.S.,” Selig said.

Selig’s tone is more friendly and proactive than Atkins. “Prediction markets are valuable” is a clear endorsement, indicating CFTC recognizes the industry’s significance. “Not pushing them offshore” reveals regulatory concerns: overly strict rules could drive platforms like Kalshi and Polymarket to offshore jurisdictions, causing the U.S. to lose control and tax revenue.

“Developing the right rules and regulations to provide the best protections” reflects CFTC’s regulatory philosophy. Unlike SEC’s tendency toward “enforce first, regulate later,” CFTC emphasizes guiding industry development through clear rules. This difference likely stems from their respective histories and cultures: SEC mainly regulates securities markets with a focus on investor protection and fraud prevention; CFTC oversees commodities and derivatives markets, emphasizing market efficiency and innovation.

However, Selig also stressed the importance of regulation. “Best protections” imply consumer rights, anti-money laundering, and manipulation prevention are essential. Prediction markets cannot be left in a regulatory vacuum; a balance must be struck between innovation and protection. Future CFTC rules may include platform licensing, minimum capital requirements, AML and KYC standards, market manipulation monitoring, and dispute resolution procedures.

Prediction markets are also under scrutiny due to insider trading reports and legislation aimed at restricting politically related betting. In traditional finance, insider trading is a serious crime, but in prediction markets, definitions are more complex. For example, if campaign staff bet on election outcome markets, does that constitute insider trading? These individuals have access to non-public polling data and campaign strategies, giving them an advantage over ordinary bettors.

From Confrontation to Cooperation: The Shift in SEC and CFTC’s Project Crypto

Recently, SEC and CFTC jointly launched “Project Crypto,” aiming to modernize cryptocurrency regulation. Just over a year ago, the two agencies were seen as engaged in a “territorial dispute” over digital assets. Former CFTC Chair Rostin Behnam believed most cryptocurrencies fell under CFTC’s commodity jurisdiction, while former SEC Chair Gary Gensler insisted that most tokens, except Bitcoin, are securities.

Atkins said Thursday that the agencies meet weekly. This regular communication marks a major shift. During Gensler and Behnam’s tenures, the agencies rarely coordinated, issuing conflicting guidance that left crypto firms in confusion. Now, weekly meetings suggest they are trying to establish a unified regulatory approach under the Biden administration.

Looking at the composition of commissioners, there is a serious partisan imbalance. Selig is the sole CFTC commissioner, while SEC has three Republican commissioners—Atkins, Hester Peirce, and Mark Uyeda—without Democratic appointees. This imbalance has sparked strong dissatisfaction among Democratic lawmakers. Maryland Senator Chris Van Hollen asked Atkins whether he would contact the White House and recommend appointing Democratic commissioners to fill SEC vacancies. Atkins responded, “Whether in public or private, I’ve always supported full commission membership. I believe it helps with debate and everything else.”

This partisan imbalance risks policy becoming overly skewed. SEC and CFTC were designed for bipartisan governance to ensure balanced and consistent policies. When all commissioners are from the same party, policies may become too aggressive or too lax, lacking checks and balances. For prediction markets, if both agencies are led by Republicans, they might implement very lenient regulation; if Democrats regain control, a regulatory swing could occur, tightening rules sharply.

Related Articles

The probability that Bitcoin will fall back to $60,000 in February on Polymarket is 31%.

The predicted weekly trading volume in the market exceeds 38 million transactions, setting a new record high

On Polymarket, the probability that ROBO's FDV exceeds $200 million on its second day of trading is 69%

The negative probability of "Court orders Trump to refund tariffs" on Polymarket surpasses 80%

Polymarket Builders' weekly trading volume has exceeded $100 million for three consecutive weeks.