When "stability" begins to fluctuate: A full review and structural analysis of the USD1 de-pegging event

Author: 137Labs

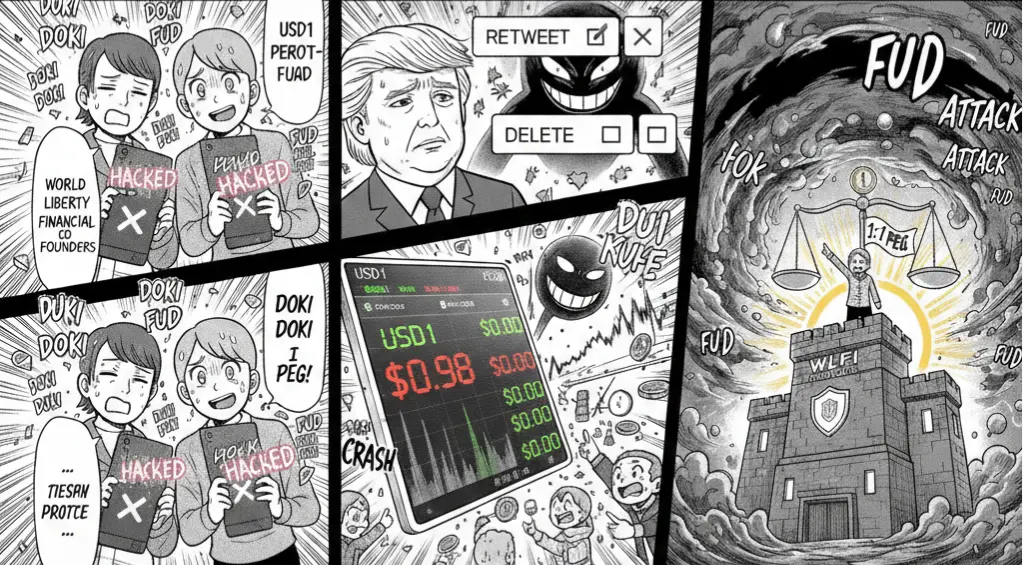

On February 23, a stablecoin called USD1 suddenly showed a significant discount in the secondary market.

On-chain quotes briefly dropped to around 0.98 USDT, and social media quickly heated up.

The project team, World Liberty Financial (WLFI), then publicly stated that this was a “coordinated attack,” and emphasized that reserves and redemption mechanisms were unaffected.

Prices then recovered.

But the problem has already emerged—

When a “stablecoin” starts to trade at a discount, is it just liquidity friction, or a sign of cracks in the credit structure?

1. Timeline: From peg to “attack theory”

Based on reports from CoinDesk, The Block, Decrypt, Wu Says Blockchain, PANews, Chain Catcher, and others, the event roughly unfolded as follows:

1️⃣ Abnormal secondary market fluctuations

- USD1 quickly fell to around 0.98 in some trading pairs

- The discount was short-lived

- Prices then rebounded

Unlike the brief de-pegging of USD Coin in 2023 due to banking risks, this event did not involve a systemic banking shock.

2️⃣ WLFI official response

WLFI publicly stated:

- This was an organized short-selling and coordinated attack

- Reserve assets showed no anomalies

- Redemption functions operated normally

- The 1:1 peg remained intact

This statement was later echoed by Chinese media outlets like Wu Says Blockchain and Chain Catcher.

3️⃣ Amplification on social media

The incident spread rapidly on X (Twitter).

Some related tweets were deleted, fueling further market speculation.

In the current highly emotional market environment, “deletion” often signals something rather than being an isolated action.

Thus, the question shifted from “Is the price de-pegged?” to:

- Are there reserve risks?

- Is there a concentrated run?

- Is there insufficient disclosure?

2. The essence of de-pegging: liquidity issue or solvency problem?

Judging whether a stablecoin has de-pegged hinges on distinguishing two entirely different risk structures.

The first is liquidity shock.

In this case, reserves are still sufficient, redemption mechanisms are intact, but due to shallow trading depth, market maker withdrawal, or concentrated selling pressure, the secondary market temporarily loses balance.

Arbitrage mechanisms usually restore the price quickly.

The second is a solvency crisis.

If the reserve assets are problematic, or if there is maturity mismatch or assets cannot be liquidated immediately, then de-pegging is no longer just a trading fluctuation but a revaluation of the balance sheet.

In this scenario, discounts tend to widen persistently, often accompanied by delayed redemptions or loss of trust.

Based on current disclosures, USD1 appears closer to the first scenario.

It is very different from the algorithmic death spiral of TerraUSD in 2022.

UST’s collapse was due to mechanism failure, whereas USD1’s peg deviation looks more like a short-term liquidity tilt.

Nevertheless, this event still holds significance.

Because the true anchor of a stablecoin is not just its reserves, but market trust.

Once trust is questioned, prices react before fundamentals do.

3. The credit structure of stablecoins: where do they “stay stable”?

Stablecoins are essentially the “base currency” of the crypto market.

Their credit support generally comes from three models:

- Algorithmic

- Collateralized

- Centralized reserve-backed

USD1 belongs to a more centralized reserve model.

The risks in this model are not from the algorithm but from:

- Reserve transparency

- Asset liquidity

- Maturity structure

- Market depth

If the market suspects reserve discounts or liquidity issues, prices often fall first.

This is very similar to “shadow banking runs” in traditional finance—once depositors start doubting, withdrawal behavior amplifies the risk.

4. Why is the market reaction this time particularly sensitive?

The panic index was already at an extremely low level that day.

In an environment with tight liquidity:

- Leverage declines

- Risk appetite weakens

- Market is highly sensitive to uncertainty

Stablecoins are not just trading tools; they are also the foundation of lending and liquidity.

Once discounts appear, chain reactions may include:

- Collateral ratios dropping

- Liquidations triggered

- Leverage further compressed

- Funds flowing out of the market

Therefore, even if prices recover quickly, the psychological impact remains.

5. Is the “attack theory” valid?

WLFI attributes the volatility to a “coordinated attack.”

In crypto markets, short-selling and rumor amplification are common.

When trading depth is shallow and market sentiment fragile, prices can be easily exaggerated.

But whether an attack can sustain depends on a key factor:

Does the market believe the reserves are real, redeemable, and sustainable?

If reserve transparency and redemption processes are clear and ongoing, attacks are hard to succeed long-term;

If disclosure is lacking, panic can reinforce itself.

6. The difference between USD1 and USDC, USDT, and the real meaning of this de-pegging

Historically, USDC briefly fell to $0.88 in 2023 due to bank risks, caused by exposure of the custodian bank and limited reserve liquidity.

Tether (USDT) has experienced minor de-pegging multiple times, usually during extreme panic or redemption pressure, but ultimately recovered as redemption mechanisms remained open and reserve liquidity was verified.

USD1 now seems to be undergoing a “trust stress test.”

This event is more like a liquidity shock rather than a solvency crisis.

The quick price recovery indicates no systemic run.

But what truly matters is not the $0.98 price, but whether the market is beginning to reassess the risk premium of “stability.”

Stablecoins are the monetary backbone of the crypto market.

When confidence in their safety wanes, the effects propagate along the credit chain:

- Leverage declines

- Lending contracts

- Assets are re-priced

- Funds flow back to mainstream assets or exit the market

Even if the event is just a short-term fluctuation, it raises future costs for financing and liquidity.

De-pegging is never just a price issue; it’s a credit pricing issue.

Prices can recover quickly,

but trust takes time to rebuild.

USD1’s de-pegging this time may not evolve into systemic risk,

but it reminds the market—

In a liquidity crunch,

credit always changes before prices do.

And once credit is re-evaluated,

the entire risk structure will also shift.

Related Articles

Peter Schiff warns that Trump's State of the Union address could trigger a "sell-off," increasing the risk of a short-term pullback after Bitcoin's rally.

Trump's State of the Union Address Triggers a Controlled Surge for Cryptocurrencies

Shiba Inu Price Forecast for February 2026: Massive Rally Ahead?

Bitunix Analyst: High Market Position in Central Bank Personnel, Japan's Interest Rate Path Adds New Uncertainty

Litecoin faces correction pressure, bears target the $45 mark

Dogecoin breaks through key resistance to turn it into support: DOGE price gains strength and may challenge the $0.096 level