On April 15, the U.S. tax filing day, Nicholas Anthony, a researcher at the Cato Institute, published an analysis report stating that the current U.S. capital gains tax rules require reporting the acquisition date, the expenditure (spending) date, the original cost, and the profit or loss for each individual bitcoin transaction. The report calculates using the example of making small purchases with bitcoin on a daily basis, and the total filing documents at year-end exceed 100 pages.

IRS Filing Rules and the Burden of Bitcoin Transaction Documentation

According to the analysis report published by Nicholas Anthony at the Cato Institute, under current U.S. tax law, each bitcoin transaction is subject to a capital gains tax filing obligation, requiring records of the following four data points: acquisition date, expenditure date, cost basis (Cost Basis), and the amount of profit or loss, and filing through IRS Form 8949 and Form 1040 Schedule D.

The report directly quotes Nicholas Anthony’s statement: “The purpose of setting capital gains tax rates is to encourage long-term holding. Given that the long-term holding policy suppresses conduct that is typically viewed as currency use, this policy distortion is especially evident in the realm of money.”

Three Policy Solutions: Including Threshold Adjustments in the “Virtual Currency Tax Fairness Act”

(Source: Scott Bessent)

(Source: Scott Bessent)

According to Nicholas Anthony’s Cato Institute report, under the current tax system, the following policy options exist:

· Completely repeal the capital gains tax

· Establish a special exemption for capital gains from cryptocurrency and foreign currencies

· Advance the “Virtual Currency Tax Fairness Act”

The report notes that the “Virtual Currency Tax Fairness Act” currently intends to set a minimum exemption for收益(gains) below $200. In the report, Nicholas Anthony recommends raising this threshold to a level consistent with the average annual household spending in the United States (about $80k).

Current State of Bitcoin Payment Infrastructure

According to relevant reporting, Square has launched a no-fee bitcoin payment service at merchants’ point-of-sale terminals. Bull Bitcoin, Zeus, and Trezor have also rolled out self-hosted wallet products to optimize consumers’ bitcoin on-chain spending workflows.

Frequently Asked Questions

Which IRS tax forms must U.S. bitcoin users file?

According to Nicholas Anthony’s analysis report from the Cato Institute, each bitcoin transaction must be reported in IRS Form 8949 and Form 1040, Attachment D (Schedule D), including the acquisition date, expenditure date, cost basis, and profit or loss amount. The reporting requirements are the same as those for traditional capital assets such as stocks.

What is the current exemption threshold for the “Virtual Currency Tax Fairness Act,” and what does the Cato Institute recommend?

According to the report Nicholas Anthony published at the Cato Institute, the “Virtual Currency Tax Fairness Act” currently intends to set a minimum exemption for cryptocurrency transaction gains below $200. In the report, Nicholas Anthony recommends raising the threshold to about $80k to correspond to the average annual household spending level in the United States.

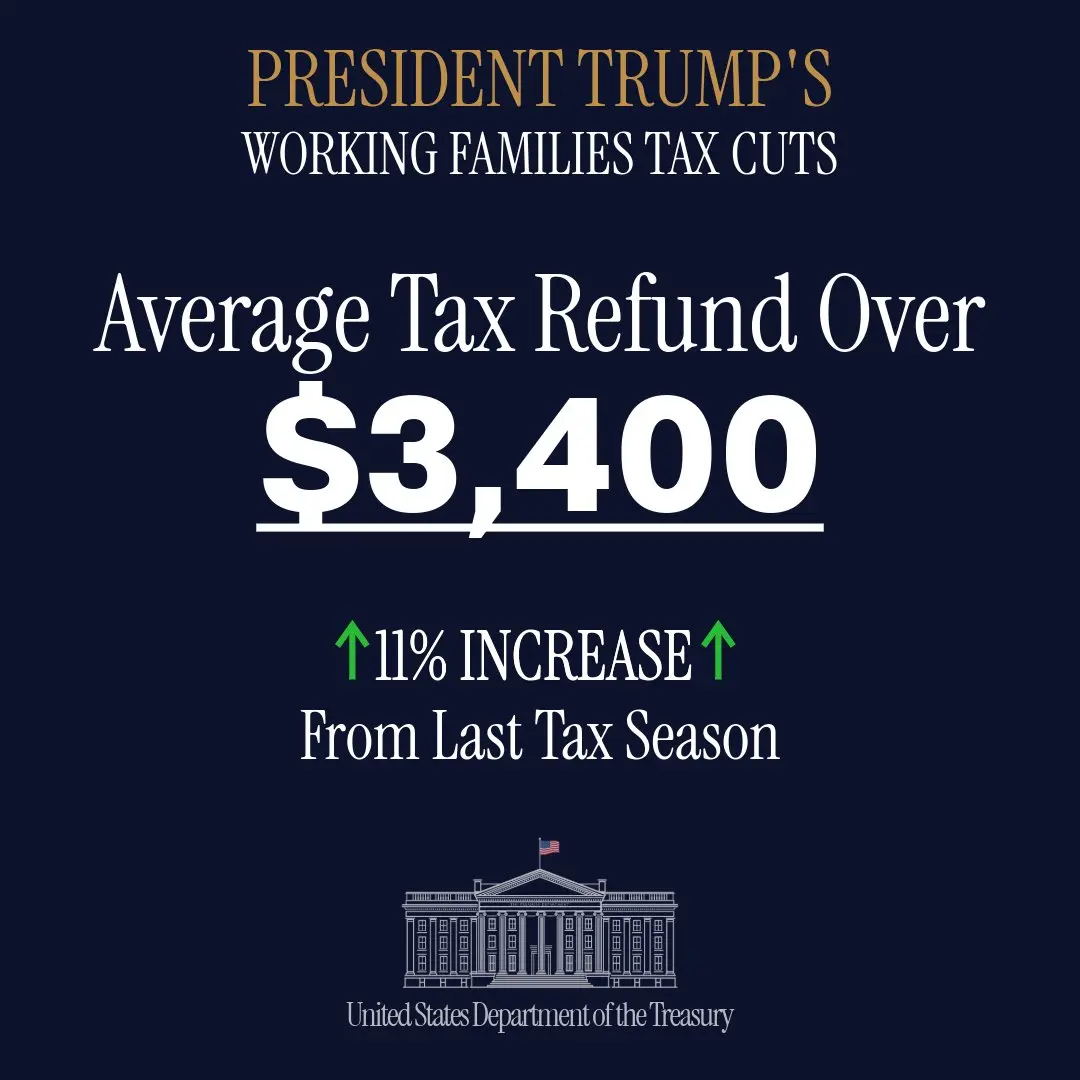

What areas does U.S. Treasury Secretary Scott Bessent’s statement on April 15, tax filing day cover?

According to relevant reporting, on April 15, Scott Bessent issued a statement regarding the “Working Families Tax Relief Act,” saying that tens of millions of U.S. working families have received more after-tax income. The statement does not address issues related to capital gains tax on bitcoin or cryptocurrency.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

South Korea's Legal Framework: Crypto Assets Accumulated During Marriage Are Divisible Property

Gate News message, April 25 — According to South Korea's Asia Economy Daily, a woman in her 40s discovered two years after her divorce that her ex-husband had secretly invested in cryptocurrency during their marriage and made substantial profits. Na-hee Kim, an attorney at Saeworld Law, stated that

GateNews46m ago

U.S. Sanctions Iran-Linked Crypto Wallets, Tether Freezes $344M USDT

U.S. Treasury Secretary Scott Bessent announced on Friday that the federal government is sanctioning multiple wallets linked to Iran as part of President Donald Trump's efforts to increase economic pressure on the country amid an ongoing ceasefire, according to CNN. The action follows Tether's

CryptoFrontier50m ago

CFTC Files Amicus Brief with Massachusetts Supreme Judicial Court, Defending Federal Authority Over Prediction Markets

Gate News message, April 25 — The U.S. Commodity Futures Trading Commission (CFTC) filed an amicus brief today with the Massachusetts Supreme Judicial Court, asserting its exclusive federal jurisdiction over commodity derivatives markets, including prediction markets. The case, Commonwealth of Massa

GateNews2h ago

Tennessee Becomes Second U.S. State to Ban Crypto ATMs, Imposing Class A Misdemeanor Penalties

Gate News message, April 24 — Tennessee has become the second U.S. state to outright ban cryptocurrency ATMs after Gov. Bill Lee signed House Bill 2505 into law on April 13. The legislation, which passed both chambers unanimously, was officially codified on Thursday and will take effect July 1.

GateNews4h ago

Italian Researcher Wins 1 BTC Bounty for 32,767-Bit Quantum Attack on Elliptic Curve Keys

Gate News message, April 24 — Giancarlo Lelli, an Italian researcher, has been awarded one Bitcoin after demonstrating the largest-scale quantum attack on elliptic curve cryptography to date. The breakthrough escalates concerns about quantum threats to Bitcoin, Ethereum, and other assets secured

GateNews5h ago

DeFi Stakeholders Petition SEC to Formalize Interface Guidance as Ethereum Proposes Native Privacy Layer

Gate News message, April 24 — The DeFi Education Fund (DEF) and 35 co-signatories, including a16z crypto, Aptos Labs, Uniswap, Chainlink, Paradigm, Solana Policy Institute, and Phantom, have petitioned the Securities and Exchange Commission (SEC) to convert its recent staff guidance on DeFi interfac

GateNews5h ago