Federal Reserve 2026 dual rate cuts become consensus! Non-farm payrolls boost January rate cut probability to 31%

After the US non-farm payrolls data was released, US federal funds futures slightly increased the probability of a rate cut in January 2026 from 22% to 31%. US interest rate futures still project two rate cuts by the Federal Reserve in 2026, with an expected easing of 58 basis points next year. The market-implied probability of a rate cut in March has surged above 55%, reflecting growing market confidence that the Fed’s easing policy will resume soon.

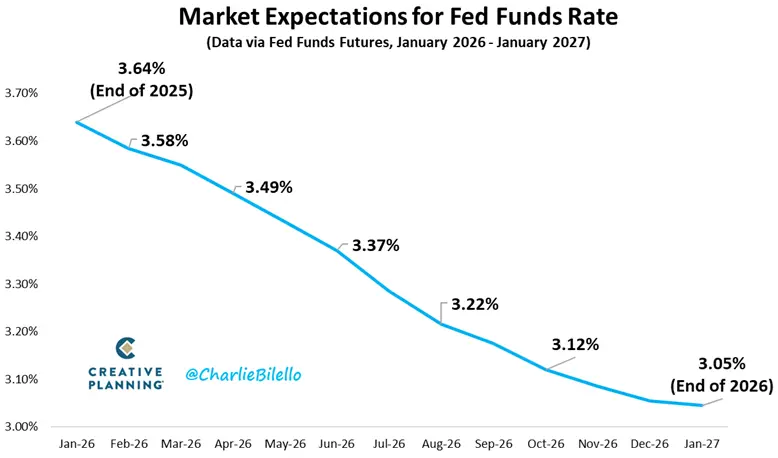

Employment Data Collapse Fuels Expectations of Fed Rate Cuts

(Source: Creative Planning)

The US dollar generally remained under pressure during early trading, as the delayed employment data confirmed that labor market growth momentum was weaker than expected. The sharp decline of 105,000 non-farm payrolls in October was the main shock, representing the third negative growth in six months, an almost unanticipated development. To make matters worse, the non-farm payroll data for August and September were revised downward, further fueling concerns that employment growth deterioration could last longer than previously thought.

Non-farm payrolls rebounded by 64,000 in November, slightly above expectations, but this modest growth is far from enough to offset previous losses. Overall, these data strongly support the Fed’s decision to cut rates again last week. The unemployment rate rose to 4.6% in November, higher than both expectations and September’s 4.4%. Meanwhile, average hourly earnings increased by only 0.1% month-over-month, well below the prior forecast of 0.3%, indicating that wage pressures are easing as labor demand cools.

Nevertheless, this release did not significantly alter expectations for a rate hike in January; a pause in rate increases remains the market’s baseline expectation. Fed officials have emphasized in recent public statements that more data is needed to assess the true state of the labor market. A key uncertainty is whether the November rebound signals a genuine turning point. Some of the improvement is attributed to reduced uncertainty after the US-China one-year tariff truce, but whether this easing will translate into sustained recruitment remains uncertain.

Three Pillars Supporting the Fed’s 2026 Double Rate Cut Path

Conversely, the repricing mainly focuses on the distant part of the yield curve. The market-implied probability of a rate cut in March has surged above 55%, reflecting increasing confidence that the Fed’s easing policy will soon resume. The Fed has planned to cut rates by another 25 basis points in 2026, so the debate centers on timing rather than direction. The risk is that if labor market weakness persists, markets might price in an earlier rate cut in early 2026.

Key Factors Supporting Fed Rate Cuts

Significant Cooling in the Labor Market: Consecutive negative non-farm payroll growth and an unemployment rate rising to 4.6% provide room for the Fed to cut rates

Easing Wage Inflation Pressures: Average hourly earnings growth slowing to 0.1% alleviates concerns about wage-driven inflation

Weak Retail Sales Growth: October retail sales were flat month-over-month, indicating insufficient consumer demand momentum

Additionally, October retail sales were flat compared to the previous month, below the expected 0.2% quarterly increase. Excluding auto sales, sales grew 0.4% from the previous quarter, slightly above the forecast of 0.3%. This consumer weakness further supports the Fed’s case for easing. The market expects a total of 58 basis points of rate cuts in 2026, equivalent to more than two cuts, reflecting investor concerns about economic slowdown.

Fed Chair Candidate and Policy Uncertainty

Furthermore, speculation about the next Fed chair has intensified, adding extra uncertainty to future monetary policy. The betting market has shifted significantly in favor of former Fed Governor Kevin W. with odds rising to about 46%, surpassing Kevin H. Hasset. Just a week ago, Hasset was the clear favorite at 77%. This shift is reportedly driven by opposition from senior advisors close to the President, who believe Hasset’s close ties to Trump are problematic.

The Fed chair’s identity is crucial for the future direction of monetary policy. W. is viewed as a more hawkish candidate, having expressed concerns about overly loose monetary policy during his tenure. If W. is ultimately appointed, it could influence the Fed’s rate cut trajectory, and the market’s projected 58 basis points of cuts may need to be reassessed. Regardless of who is appointed, they will face the reality of a weakening labor market and slowing economic growth.

In the forex market this week, the Japanese yen performed the strongest, followed by the British pound and Swiss franc. The Australian dollar and US dollar lagged, reflecting market reactions to the Fed’s easing expectations and the resulting dollar weakness. The US 10-year Treasury yield fell after the employment data, indicating a re-pricing of the Fed’s future policy path.

Global Central Bank Coordination and Fed Policy Spillovers

The Fed’s policy shift has also triggered a chain reaction among other central banks worldwide. The European Central Bank faces economic growth slowdown pressures, with December PMI data indicating a slowdown in eurozone economic activity. While the Bank of Japan maintains an accommodative stance, the yen has been the strongest this week, partly reflecting market expectations that Fed rate cuts will weaken the dollar. The Bank of England faces similar policy dilemmas; despite improved PMI data, a cooling labor market leaves room for further rate cuts.

As the world’s most influential central bank, the Fed’s policy adjustments have profound impacts on global financial markets and capital flows. If the Fed indeed implements two rate cuts in 2026, it will provide more policy space for other central banks, potentially sparking a global easing wave. This could support risk asset prices but also risk asset bubbles and financial stability concerns.

Related Articles

Non-farm payrolls may unexpectedly increase by only 70,000! White House: It's not an employment recession, but a productivity revolution

Kevin Wash's Federal Reserve New Policy! Using AI to tame inflation, refusing to be a big buyer of U.S. bonds

Charlie Munger: How do I respond when assets drop by 50%?

Wosh is about to succeed as Federal Reserve Chair! The probability of a rate cut in June skyrocketed to 46%, boosting risk assets.

Trump to Announce Federal Reserve Chair! Bitcoin-Friendly Kevin Wash's win rate soars to 95%

Gate Daily (January 30): Trump declares a national emergency and Cuban tariffs; The United States will announce a new chairman of the Federal Reserve next week